PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044134

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044134

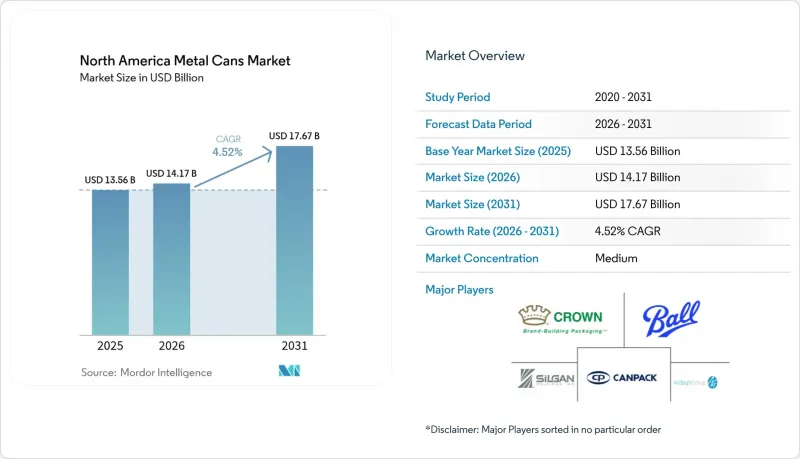

North America Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The North America metal cans market size is projected to expand from USD 13.56 billion in 2025 and USD 14.17 billion in 2026 to USD 17.67 billion by 2031, registering a CAGR of 4.52% between 2026 to 2031.

Rising extended-producer-responsibility fees on virgin plastics, tariff-driven import costs for tinplate, and brand owners' premiumization strategies continue to redirect packaging demand toward infinitely recyclable aluminum cans. Converter margins improved after lightweighting trimmed 355-milliliter beverage-can weights to 12.2 grams, while nearshored capacity in Mexico shortened order-to-delivery cycles by 40%. High-purity can-sheet expansions in Alabama and the southeastern United States reduce freight outlays by USD 40-50 per tonne and cushion the market against London Metal Exchange price swings. Personal-care brands embracing monobloc aerosols and ready-to-drink alcohol producers shifting to sleek 355-milliliter profiles create incremental high-margin volume that offsets soft beverages and shelf-stable food declines.

North America Metal Cans Market Trends and Insights

Growing Beverage Industry in the Region

North American fillers consumed nearly 120 billion aluminum cans in 2025 as energy drinks, hard seltzers, and craft beer offset a 1.2% slide in carbonated soft drinks. Mexico's beer output rose 4.3% in 2024 after a USD 1.2 billion expansion lifted annual capacity by 25 million hectoliters and shifted 36% of domestic packaging into cans. Ready-to-drink cocktails in the United States posted 18% retail-sales growth in 2024, with aluminum capturing 82% of volume at premium price points. Canada diverged, with beverage manufacturing sales contracting 1.7% in 2024 amid refillable-glass incentives. Cross-border supply realignment saw Mexican can exports to the United States climb 12%, while domestic U.S. capacity utilization hovered near 88%.

Shift Toward Infinitely Recyclable Aluminum Packaging

Seventy-five percent of all aluminum ever produced remains in use, underpinning a closed-loop advantage as California's Senate Bill 54 mandates 65% recycled content by 2032. Oregon's expanded deposit-return system is projected to lift redemption rates to 82% by 2026, compressing the virgin-to-recycled price spread by 38%. PepsiCo and Molson Coors pledged 100% recycled-content cans for select lines by 2027, redirecting 180,000 tonnes of annual scrap demand. These mandates elevate aluminum against polyethylene terephthalate's 9% recycling rate and against flexible pouches that lack commercial reclamation streams.

Proliferation of PET and Flexible Pouches in Food and Drink

Polyethylene terephthalate bottles and flexible pouches held 22% of North American juice and dairy packaging in 2024, eroding metal-can share in shelf-stable meals where transparency and resealability resonate. Ocean Spray and Tropicana each shifted up to 20% of their aseptic volume from steel cans to PET, citing unit costs up to 30% lower. Flexible pouches captured 18% of ready-to-eat meal volume in 2024 after brands leveraged 40-50% lighter weights and 60% smaller cube sizes compared to rigid cans. Mexican juice segments show even higher displacement, as cartons and PET hold a combined 68% share. Converters answer with lightweighting and digital printing, yet these actions address cost rather than core format preference.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization of Canned Wines and Cocktails (RTDs)

- Expansion of High-Purity Can-Sheet Mills in the United States

- Volatile Aluminum and Steel Coil Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminum captured 79.76% of North America's metal can market share in 2025, outpacing steel as extended producer responsibility rules reward closed-loop recyclability. The North America metal cans market for aluminum applications is forecast to expand at a 4.93% CAGR, whereas the steel market grows at only 3.12%. Tariff hikes that doubled Section 232 duties in 2025 inflated imported tinplate costs by USD 150-200 per tonne, squeezing steel-can margins and reinforcing aluminum's cost edge.

Novelis's and Ball's combined 900,000-tonne can-sheet additions fortify domestic supply and further lower freight outlays. Steel remains indispensable for retort-sterilized foods, paints, and industrial chemicals, but its 20.24% share in 2025 is expected to slip as flexible pouches chip away at three-piece formats. Material preferences also diverge geographically: Mexico's 28% steel-can share reflects local tinplate availability, while the United States' share contracted to 18%.

Two-piece drawn-and-ironed cans delivered a 61.32% share in 2025, serving high-volume beverages that demand seamless walls and low unit weights. Monobloc aerosols, however, exhibit the fastest 5.07% CAGR, offering tamper evidence, premium aesthetics, and 15% lighter weight than three-piece counterparts. Three-piece steel cans persist in paint and chunky soups, yet flexible pouches erode their growth to 3.21%.

Impact-extrusion presses enable monobloc geometry without side seams, but USD 8-12 million tooling bills curb smaller entrants. Retrofitting older three-piece lines with drawn-and-ironed tooling is an interim step for converters chasing beverage economics. As personal-care brands heighten demand for design flexibility, monobloc share is set to climb above 12% by 2031.

The North American Metal Cans Market Report is Segmented by Material Type (Aluminium, and Steel), Can Structure (Two-Piece, Three-Piece, and Monobloc Aerosol), Capacity/Size (Less Than 50ML, 250-500 Ml, and More), Manufacturing Process (Drawn and Ironed, Drawn and Redrawn, and Impact Extrusion), and End-User Industry (Food, Beverage, Personal Care and Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ball Corporation

- Crown Holdings, Inc.

- Silgan Holdings Inc.

- Ardagh Group S.A.

- CAN-PACK S.A.

- Mauser Packaging Solutions Holding Company

- Envases Universales de Mexico, S.A. de C.V.

- Trivium Packaging B.V.

- Tecnocap S.p.A.

- DS Containers Inc.

- CCL Industries Inc.

- Independent Can Company

- Allstate Can Corporation

- Sonoco Products Company

- BWAY Corporation

- Trinity Packaging Supply, LLC

- O.Berk Company, LLC

- Peerless Beverage Packaging LLC

- Consolidated Container Company LLC

- Pacific Coast Producers Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Beverage Industry in the Region

- 4.2.2 Shift Toward Infinitely-Recyclable Aluminium Packaging

- 4.2.3 Premiumisation of Canned Wines and Cocktails (RTDs)

- 4.2.4 Expansion of High-Purity Can-Sheet Mills in the United States

- 4.2.5 On-Premise Restrictions Accelerating Take-Home Multi-Packs

- 4.2.6 Blockchain-Enabled Traceability Demands From Brand Owners

- 4.3 Market Restraints

- 4.3.1 Proliferation of PET and Flexible Pouches in Food and Drink

- 4.3.2 Volatile Aluminium and Steel Coil Prices

- 4.3.3 Rising Refill-and-Reuse Legislation Challenging Single-Use Cans

- 4.3.4 Supply Bottlenecks in Body-Maker and D and I Line Equipment

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Aluminium

- 5.1.2 Steel

- 5.2 By Can Structure

- 5.2.1 Two-Piece

- 5.2.2 Three-Piece

- 5.2.3 Monobloc Aerosol

- 5.3 By Capacity / Size

- 5.3.1 Less than 50 ml

- 5.3.2 250-500 ml

- 5.3.3 500-1,000 ml

- 5.3.4 More than 1,000 ml

- 5.4 By Manufacturing Process

- 5.4.1 Drawn and Ironed (D and I)

- 5.4.2 Drawn and Redrawn (DRD)

- 5.4.3 Impact Extrusion

- 5.5 By End-User Industry

- 5.5.1 Food

- 5.5.2 Beverage

- 5.5.3 Personal Care and Cosmetics

- 5.5.4 Pharmaceuticals

- 5.5.5 Paints and Industrial Chemicals

- 5.5.6 Automotive Fluids and Lubricants

- 5.5.7 Other End-User Industries

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ball Corporation

- 6.4.2 Crown Holdings, Inc.

- 6.4.3 Silgan Holdings Inc.

- 6.4.4 Ardagh Group S.A.

- 6.4.5 CAN-PACK S.A.

- 6.4.6 Mauser Packaging Solutions Holding Company

- 6.4.7 Envases Universales de Mexico, S.A. de C.V.

- 6.4.8 Trivium Packaging B.V.

- 6.4.9 Tecnocap S.p.A.

- 6.4.10 DS Containers Inc.

- 6.4.11 CCL Industries Inc.

- 6.4.12 Independent Can Company

- 6.4.13 Allstate Can Corporation

- 6.4.14 Sonoco Products Company

- 6.4.15 BWAY Corporation

- 6.4.16 Trinity Packaging Supply, LLC

- 6.4.17 O.Berk Company, LLC

- 6.4.18 Peerless Beverage Packaging LLC

- 6.4.19 Consolidated Container Company LLC

- 6.4.20 Pacific Coast Producers Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment