PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044147

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044147

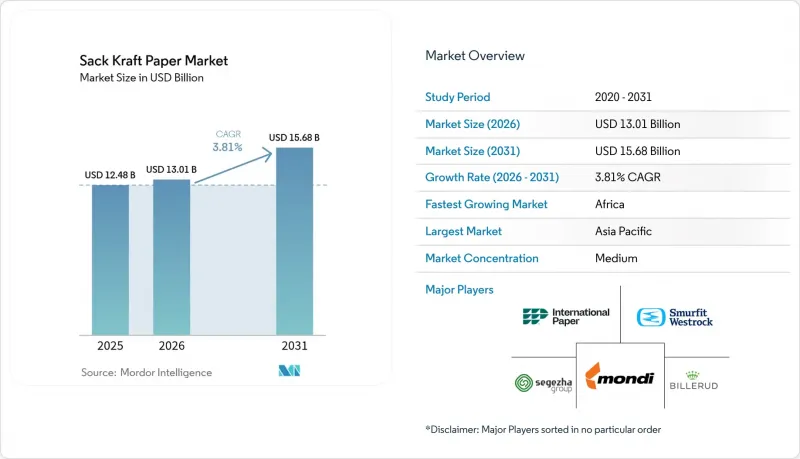

Sack Kraft Paper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The sack kraft paper market size was valued at USD 12.48 billion in 2025 and estimated to grow from USD 13.01 billion in 2026 to reach USD 15.68 billion by 2031, at a CAGR of 3.81% during 2026-2031.

The steady headline figure hides a structural transformation as plastic-ban legislation, carbon border adjustment mechanisms and digitized supply chains accelerate substitution of woven polypropylene bulk bags with recyclable multiwall paper sacks across cement, food ingredients and minerals handling. Integrated producers are upgrading mills with barrier coating and RFID-ready converting lines to secure premium contracts, while converters race to install form-fill-seal (FFS) equipment that doubles bagging speeds and cuts labor outlays by one-third. Raw-material volatility in virgin pulp and old corrugated containers continues to squeeze margins, but vertical integration and long-term fiber contracts are mitigating price swings. Lightweight single-ply extensible papers, supported by the need to curb freight emissions, are becoming the format of choice for 25-50 kilogram cement and fertilizer applications. Automation-ready, curbside-recyclable designs underpin future demand, positioning the sack kraft paper market as a strategic beneficiary of circular-economy policies worldwide.

Global Sack Kraft Paper Market Trends and Insights

Plastic-Ban Legislation Accelerating Paper Substitution

Single-use plastic prohibitions are compressing the replacement cycle for woven polypropylene across bulk packaging. Legislative momentum against single-use plastics is compressing the substitution timeline for woven polypropylene sacks across bulk packaging applications. The European Union's Packaging and Packaging Waste Regulation, finalized in 2024, mandates that 65% of packaging materials be recyclable by 2030 and bans oxo-degradable plastics outright, forcing cement and fertilizer distributors to transition to multiwall kraft sacks that qualify for municipal paper recycling streams. In the United Kingdom, the Extended Producer Responsibility scheme imposed a GBP 200 per tonne levy on non-recyclable packaging in 2025, raising the landed cost of polypropylene FIBCs by 18-22% and tilting procurement toward paper alternatives that avoid the surcharge. This driver exerts the largest positive swing on the sack kraft paper market because compliance is mandatory and immediate.

Cement-Sector Decarbonization Favoring Recyclable Sacks

Global cement producers are embedding Scope 3 packaging emissions into net-zero roadmaps. A 2025 life-cycle assessment verified that kraft sacks deliver 60% lower CO2 than polypropylene equivalents when end-of-life recycling is counted. Flagship projects include Mondi and Cemex's SolmixBag, a dissolvable single-ply kraft sack already commercial in Spain, and UltraTech Cement's pledge to shift 30% of its Indian retail portfolio to recycled kraft by 2027. European circular-construction pilots are trialing deposit-return schemes for reusable kraft sacks, rewarding contractors for recovering empty bags. Because cement represented more than two-fifths of 2025 demand, decarbonization choices by this sector meaningfully recalibrate the sack kraft paper market trajectory over the medium term.

Penetration of Woven-PP FIBCs in Bulk Packaging

Conductive and antistatic flexible intermediate bulk containers fill safety and reusability needs that kraft cannot match in chemicals and flammable powders. Type C FIBCs cost USD 8-12 each against USD 15-20 for equivalent multiwall kraft with antistatic liners, a gap widened by their ability to complete 5-10 shipping cycles. Closed-loop supply chains in plastics resins, mineral concentrates and automotive parts therefore continue to specify polypropylene, placing a -0.6% drag on the sack kraft paper market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Adoption of Curbside-Recyclable Heavy-Duty Mailers

- Food-Grade Bulk Ingredients Shifting to Certified Paper Sacks

- Volatile Virgin-Fiber and OCC Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Form-fill-seal sacks accounted for a meaningful proportion of the sack kraft paper market size and post a 4.78% CAGR because automated lines fill up to 1,800 units per hour, twice the speed of valve systems. Cement and chemical producers adopt FFS to cut stitching labor by 30-40% and boost bagging accuracy, while FFS-ready papers with controlled coefficient of friction maintain seal integrity. Valve sacks, holding 41.32% share in 2025, remain indispensable where dust control and legacy pneumatic filling dominate. Open-mouth and pinch-bottom formats fill niches in food and seed applications that require metal detection or upright retail display. Asia-Pacific drives FFS investments as rising wages narrow the cost gap versus automation, and North America leads on RFID-embedded FFS sacks that integrate with warehouse management software. Overall, the continuous shift toward high-speed automated packaging plants underpins sustained demand across all packaging types within the sack kraft paper market.

Second-generation FFS designs now integrate inline RFID tag insertion, variable data printing and palletizing robotics. Converters market turnkey lines that promise inventory accuracy above 99%, a value proposition that outweighs the upfront capital. Meanwhile, European mills calibrate paper formation to accommodate ultrasonic sealing demanded by recycled kraft substrates. Although valve sacks dominate in dusty cement environments, FFS systems are infiltrating fertilizer, pet food and pigment facilities due to superior filling hygiene. The competitive battle therefore centers on material specifications and machine compatibility, cementing packaging type as a decisive growth vector for the sack kraft paper market.

Coated and barrier kraft held 37.21% of sack kraft paper market share in 2025 and post the fastest 4.69% CAGR, reflecting customer migration from plastic-lined sacks to fully recyclable papers with moisture and oxygen barriers. Bio-based coatings achieve water-vapor transmission below 10 g/m2/24 h, opening applications in bulk coffee, flour and sugar without compromising recyclability. Standard kraft remains the workhorse for cement and minerals because tensile strength and printability trump barrier performance, though its growth is more subdued. Semi-extensible and extensible grades serve abrasives and jagged fertilizers, with 6-8% elongation at break preventing rupture during handling. Nanofiber pre-coatings and inline dispersion barriers now enable thinner gauges to pass 50-kilogram drop tests, supporting lightweighting targets mandated by carbon assessment protocols.

Investment in single-step barrier coating lines lowers conversion costs by up to 18% versus offline lamination, bringing premium performance within reach of mid-volume users. European coffee roasters and Asian spice traders increasingly specify mineral-based oxygen barriers that avoid PFAS chemistry. Specialty sub-grades such as creped or wet-strength kraft fill cushioning and outdoor storage requirements, rounding out a diverse product spectrum. This breadth ensures that each performance tier finds a stable customer base, reinforcing grade-level depth in the sack kraft paper market.

The Sack Kraft Paper Market Report is Segmented by Packaging Type (Valve Sacks, Open Mouth Sacks, Pinch-Bottom Sacks, Form-Fill-Seal Sacks, and More), Grade (Kraft, Semi-Extensible, Extensible, Coated/Barrier Kraft, and More), Ply/Layer Count (1-Ply, 2-Ply, and More), End-User Industry (Building Materials and Cement, Food and Beverage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 32.54% of 2025 global revenue behind China's cement consumption and India's agricultural packaging needs. Yet infrastructure moderation and patchy plastic-ban enforcement temper near-term growth. Rising labor costs push converters toward FFS automation, boosting demand for high-performance extensible grades. Capacity additions in Vietnam and Indonesia reflect mill owners' strategy to serve Southeast Asian growth corridors and hedge against Chinese import restrictions. Currency volatility and imported pulp dependence, however, keep cost structures exposed.

Africa is the fastest-growing region at a 4.77% CAGR, propelled by Nigeria's packaging market, which rises from USD 2 billion in 2024 to USD 3.5 billion by 2032. Plastic bans in Nigeria and South Africa, paired with 20% annual e-commerce growth, create demand for cement sacks and mailers. Supply constraints persist because fewer than 40% of regional mills run on renewable energy, limiting FSC certification and EU market access. The African Continental Free Trade Area eases intra-regional shipments, encouraging localized converting investments and regional specialization.

Europe and North America account for mature but stable demand shaped by infrastructure refurbishment and sustainability regulations. Carbon border adjustment tariffs effective in 2026 incentivize domestic low-emission paper and penalize imports from coal-fired mills. South America's outlook is tied to agricultural exports; Brazilian pulp expansions add regional fiber availability, while Andean construction projects use more paper sacks as governments phase out plastic. Collectively, these geographic nuances create a mosaic of opportunities and risks, sustaining global expansion for the sack kraft paper market.

- Mondi plc

- Smurfit Kappa Group plc

- WestRock Company

- Billerud AB

- International Paper Company

- Segezha Group PJSC

- Stora Enso Oyj

- Gascogne Groupe SA

- Nordic Paper AS

- Natron-Hayat d.o.o.

- Horizon Pulp and Paper Ltd.

- Canfor Corporation

- Klabin S.A.

- SCG Packaging Public Company Limited

- Oji Holdings Corporation

- Nine Dragons Paper Holdings Ltd.

- Sappi Limited

- Heinzel Holding GmbH

- Georgia-Pacific LLC

- Rengo Co., Ltd.

- Daio Paper Corporation

- Ahlstrom Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value / Supply-Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Market Drivers

- 4.5.1 Plastic-ban Legislation Accelerating Paper Substitution

- 4.5.2 Cement-sector Decarbonization Favoring Recyclable Sacks

- 4.5.3 E-commerce Adoption of Curbside-recyclable Heavy-duty Mailers

- 4.5.4 Food-grade Bulk Ingredients Shifting to Certified Paper Sacks

- 4.5.5 Radio-frequency-identifiable Sack Papers Simplifying Warehouse Automation

- 4.5.6 Carbon Border Adjustment Mechanisms Boosting EU Demand for Low-Emission Sack Papers

- 4.6 Market Restraints

- 4.6.1 Penetration of Woven-PP FIBCs in Bulk Packaging

- 4.6.2 Volatile Virgin-fiber and OCC Prices

- 4.6.3 Emergence of Soluble Fiber-based Bulk Packaging Films Eroding Niche Applications

- 4.6.4 Regional Shortfall of Renewable Energy Access Limiting Mill Green Certifications

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

5 MARKET SIZE AND GROWTH FORECASTS, VALUE

- 5.1 By Packaging Type

- 5.1.1 Valve Sacks

- 5.1.2 Open Mouth Sacks

- 5.1.3 Pinch-Bottom Sacks

- 5.1.4 Form-Fill-Seal Sacks

- 5.1.5 Rest of Packaging Type

- 5.2 By Grade

- 5.2.1 Kraft

- 5.2.2 Semi-Extensible

- 5.2.3 Extensible

- 5.2.4 Coated / Barrier Kraft

- 5.2.5 Rest of Grade

- 5.3 By Ply / Layer Count

- 5.3.1 1-Ply

- 5.3.2 2-Ply

- 5.3.3 3-Ply

- 5.3.4 More than 3-Ply

- 5.4 By End-User Industry

- 5.4.1 Building Materials and Cement

- 5.4.2 Food and Beverage Ingredients

- 5.4.3 Chemicals and Fertilizers

- 5.4.4 Agriculture and Animal Feed

- 5.4.5 Minerals and Pigments

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mondi plc

- 6.4.2 Smurfit Kappa Group plc

- 6.4.3 WestRock Company

- 6.4.4 Billerud AB

- 6.4.5 International Paper Company

- 6.4.6 Segezha Group PJSC

- 6.4.7 Stora Enso Oyj

- 6.4.8 Gascogne Groupe SA

- 6.4.9 Nordic Paper AS

- 6.4.10 Natron-Hayat d.o.o.

- 6.4.11 Horizon Pulp and Paper Ltd.

- 6.4.12 Canfor Corporation

- 6.4.13 Klabin S.A.

- 6.4.14 SCG Packaging Public Company Limited

- 6.4.15 Oji Holdings Corporation

- 6.4.16 Nine Dragons Paper Holdings Ltd.

- 6.4.17 Sappi Limited

- 6.4.18 Heinzel Holding GmbH

- 6.4.19 Georgia-Pacific LLC

- 6.4.20 Rengo Co., Ltd.

- 6.4.21 Daio Paper Corporation

- 6.4.22 Ahlstrom Oyj

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment