PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044181

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044181

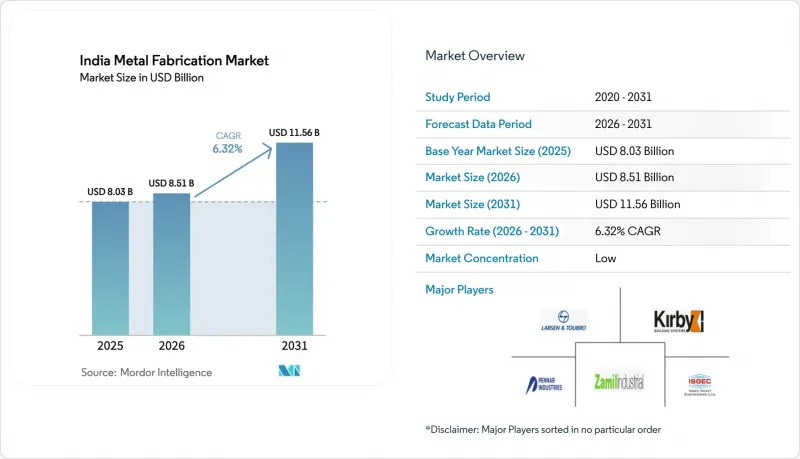

India Metal Fabrication - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The India Metal Fabrication Market size is expected to increase from USD 8.03 billion in 2025 to USD 8.51 billion in 2026 and reach USD 11.56 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

Growth reflects stronger public capital formation and a broad rebound in steel capacity, as domestic crude steel reached 235 million tonnes by November 2025, while policy targets still point to 300 million tonnes by 2030. Large public programs are sustaining multi-year demand for structural steel, rail systems, and station infrastructure, and defence indigenization has lifted domestic output and shifted orders toward certified suppliers with tighter traceability. Rising data center deployments and energy transition projects are pulling orders for modular racks, mounting structures, and pressure vessels, which is prompting investment in welding quality and corrosion-resistant coatings. Export-facing producers are preparing for the EU's Carbon Border Adjustment Mechanism from January 1, 2026, which raises the need for lower-emission routes and higher documentation standards on embedded emissions.

India Metal Fabrication Market Trends and Insights

Renewable-Energy OEM Localization For Wind Towers And Solar MMS

Defense against supply chain risk and policy incentives are bringing component manufacturing onshore across modules, towers, and mounting systems. Solar module manufacturing capacity nearly doubled from 38 GW in March 2024 to 74 GW by March 2025 as the Approved List of Models and Manufacturers and Basic Customs Duty supported domestic build-out, translating to steady orders for MMS, trackers, and galvanized structures. Wind turbine component capacity stands near 18 GW, and localization is reinforced by new lists that raise the bar on welding standards and certification for tower makers that serve coastal and high-wind sites. The National Green Hydrogen Mission has earmarked INR 14.66 billion for electrolyzer integration, which pulls precision frames and high-pressure vessels into the workload of certified shops, equal to USD 176.7 million in parentheses next to the original value (INR 14.66 billion, USD 176.7 million). Long-life solar and wind assets are shifting buyers toward pre-galvanized or hot-dip galvanized steel and higher-grade fasteners to extend structure life in saline and humid zones, increasing unit value while reducing field failures. From September 2026, BIS Scheme-X will demand domestic certification on specified heavy electrical and mounting equipment, which will push lagging small shops to upgrade in-house testing or exit sensitive supply chains.

Infrastructure Super-Cycle with Gati Shakti And NIP

Public investment has sustained momentum into FY 2025-26 with INR 11.21 lakh crore in capital expenditure and a 50-year interest-free loan of INR 1.5 lakh crore to states for infrastructure, which together support steel-intensive highways, rail, and urban transit programs, equal to USD 135.1 billion and USD 18.1 billion respectively at the prevailing exchange rate in parentheses next to the original values (INR 11.21 lakh crore, USD 135.1 billion) and (INR 1.5 lakh crore, USD 18.1 billion). The Ministry of Road Transport and Highways allocated INR 2.87 lakh crore for FY26 to expand the national highway network, equal to USD 34.6 billion in parentheses next to the original value (INR 2.87 lakh crore, USD 34.6 billion). Indian Railways' record capex of INR 2,65,200 crore for FY26 prioritizes rolling stock, station moder nization, and corridor capacity additions that intensify demand for certified structural fabrication, equal to USD 31.9 billion in parentheses next to the original value (INR 2,65,200 crore, USD 31.9 billion). Metro rail packages are anchoring complex steelwork orders that require higher welding standards and stronger documentation, including an underground stretch in Indore awarded to a large consortium during 2025 at an order value of INR 2,189 crore, equal to USD 263.7 million in parentheses next to the original value (INR 2,189 crore, USD 263.7 million). These commitments keep the India metal fabrication market aligned with multi-year pipelines, which support capacity utilization and encourage investment in advanced cutting, forming, and inspection systems.

CBAM-Linked Carbon-Compliance Cost on Aluminum and Steel Exports

The EU's Carbon Border Adjustment Mechanism enters full financial enforcement on January 1, 2026, which means EU importers will purchase CBAM certificates linked to embedded emissions in covered goods. Indian crude steel emission intensity near 2.55 tonnes CO2 per tonne implies a sizable price wedge if producers do not reduce emissions intensity toward European benchmarks, which puts pressure on blast furnace routes. India's steel and aluminium shipments to the EU already fell from USD 7.71 billion in FY24 to USD 5.82 billion in FY25, signaling exposure for export-oriented mills and downstream suppliers. Analytical estimates put annual CBAM liability for India near USD 1-2.5 billion, with iron and steel accounting for most covered exports, which strengthens the case for scrap-based EAFs and renewable captive power. Planning for measurement, reporting, and verification is a new requirement for many exporters, which increases the value of documented, lower-emission inputs across the India metal fabrication market.

Other drivers and restraints analyzed in the detailed report include:

- Defence Offsets and Indigenization Lifting Precision Fabrication

- Data-Center Build-Out Driving Heavy Modular Fabrication

- MSME Power-Supply Bottlenecks and Cost Pressures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Machining held 34.28% of the 2025 service-type revenue and continues to anchor high-precision workload in power, oil and gas, and defence, where dimensional tolerance and surface finish targets dictate process choice in the India metal fabrication market. Buyers frequently require inspection traceability and formal process control, which sustains demand for advanced machining centers with in-line metrology, and encourages integration with digital quality systems. Organized suppliers align capacity around long-cycle capital orders that prioritize uptime and adherence to PQR and WPS protocols, which stabilizes throughput. Service providers with sustained investments in automation and maintenance tend to report higher machine utilization and consistent delivery performance, which maintains their position in the India metal fabrication market. Certification regimes like ISO 3834-2 and EN 1090 support this profile by embedding welding quality and structural component compliance into the sourcing checklist for tier-1 buyers.

Welding is projected to expand at a 7.34% CAGR through 2031 as tower sections, tracker frames, and defense structures introduce higher welding-quality expectations, which raises the process value within the India metal fabrication market. Predictable demand from wind and solar assembly runs favors submerged arc and robotic MIG cells, while defense and rail packages pull in certified TIG and specialized consumables for thicker sections. Integrated suppliers use offline fixtures, weld-positioners, and end-of-line inspection records to support serial production and to maintain consistent bead quality across batches. Shops that record interpass temperature, heat input, and post-weld treatment provide stronger documentation and face fewer NCRs in audits, which shortens cycle time and reduces rework on large modules. Over the forecast period, service-type specialization will remain visible as machining concentrates on high-precision workloads and welding absorbs a larger share of renewable and rolling-stock assemblies within the India metal fabrication market.

The India Metal Fabrication Market is Segmented by Service Type (Cutting, and Others), by Material (Carbon Steel, and Others), by End-User Industry (Construction & Infrastructure, and Others), and by Region (Western India, Southern India, Northern India, Eastern India, and Central India). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Larsen & Toubro Ltd

- Kirby Building Systems India

- Zamil Industrial Investment Co.

- ISGEC Heavy Engineering Ltd

- Pennar Industries Ltd

- Salasar Techno Engineering Ltd

- JSW Severfield Structures Ltd

- Godrej Process Equipment

- Diamond Engineering (India) Pvt Ltd

- TEMA India Ltd

- Novatech Projects (India) Pvt Ltd

- Karamtara Engineering Pvt Ltd

- Bharat Heavy Electricals Ltd (Fabrication Div.)

- Tata Projects Ltd

- Welspun Corp Ltd

- Hindustan Dorr-Oliver Ltd

- Jindal Stainless - Fabrication Unit

- Bharat Forge Ltd (Fabrication Business)

- Essar Heavy Engineering Services

- Techno-Fab Engineering Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure super-cycle (Gati Shakti, NIP) unleashing structural-steel demand

- 4.2.2 Renewable-energy OEM localisation (wind towers, solar MMS)

- 4.2.3 Defence offsets accelerating precision fabrication

- 4.2.4 Data-center boom driving heavy modular fabrication

- 4.2.5 EV & battery-pack light-weighting creating aluminium sub-assembly demand

- 4.2.6 Green-steel procurement mandates (public tenders from FY-26)

- 4.3 Market Restraints

- 4.3.1 Imported coking-coal cost volatility

- 4.3.2 MSME power-supply bottlenecks

- 4.3.3 Fragmented quality-assurance ecosystem limits export readiness

- 4.3.4 CBAM-linked carbon-compliance cost for aluminium/steel exports

- 4.4 Value / Supply-Chain Analysis

- 4.5 Government Regulations & Key Initiatives

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Recent Global Disruptions on the India Metal Fabrication Market

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Service Type

- 5.1.1 Cutting

- 5.1.2 Forming / Bending

- 5.1.3 Welding

- 5.1.4 Machining

- 5.1.5 Punching / Stamping

- 5.1.6 Finishing / Surface Treatment

- 5.1.7 Others (Assembling, etc.)

- 5.2 By Material

- 5.2.1 Carbon Steel

- 5.2.2 Stainless & Alloy Steel

- 5.2.3 Aluminium

- 5.2.4 Others (Copper, Brass, Specialty Alloys, Sheet Metal (CRCA, GI, HR))

- 5.3 By End-User Industry

- 5.3.1 Construction & Infrastructure

- 5.3.2 Automotive & Auto Components

- 5.3.3 Railways & Metro

- 5.3.4 Power & Utilities

- 5.3.5 Aerospace & Defence

- 5.3.6 Oil, Gas & Refinery

- 5.3.7 Marine and Shipbuilding

- 5.3.8 Manufacturing - Heavy Machinery & Consumer Durables

- 5.3.9 Others (Job shops, Agricultural Equipment, Electricals, Consumer Durables, etc)

- 5.4 By Region

- 5.4.1 Western India (Maharashtra, Gujarat, Goa)

- 5.4.2 Southern India (Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala)

- 5.4.3 Northern India (Delhi NCR, Haryana, Punjab, Uttar Pradesh, Uttarakhand, Himachal Pradesh, Rajasthan)

- 5.4.4 Eastern India (West Bengal, Jharkhand, Odisha, Bihar, Chhattisgarh)

- 5.4.5 Central India (Madhya Pradesh, parts of Chhattisgarh)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Larsen & Toubro Ltd

- 6.4.2 Kirby Building Systems India

- 6.4.3 Zamil Industrial Investment Co.

- 6.4.4 ISGEC Heavy Engineering Ltd

- 6.4.5 Pennar Industries Ltd

- 6.4.6 Salasar Techno Engineering Ltd

- 6.4.7 JSW Severfield Structures Ltd

- 6.4.8 Godrej Process Equipment

- 6.4.9 Diamond Engineering (India) Pvt Ltd

- 6.4.10 TEMA India Ltd

- 6.4.11 Novatech Projects (India) Pvt Ltd

- 6.4.12 Karamtara Engineering Pvt Ltd

- 6.4.13 Bharat Heavy Electricals Ltd (Fabrication Div.)

- 6.4.14 Tata Projects Ltd

- 6.4.15 Welspun Corp Ltd

- 6.4.16 Hindustan Dorr-Oliver Ltd

- 6.4.17 Jindal Stainless - Fabrication Unit

- 6.4.18 Bharat Forge Ltd (Fabrication Business)

- 6.4.19 Essar Heavy Engineering Services

- 6.4.20 Techno-Fab Engineering Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment