PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044184

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044184

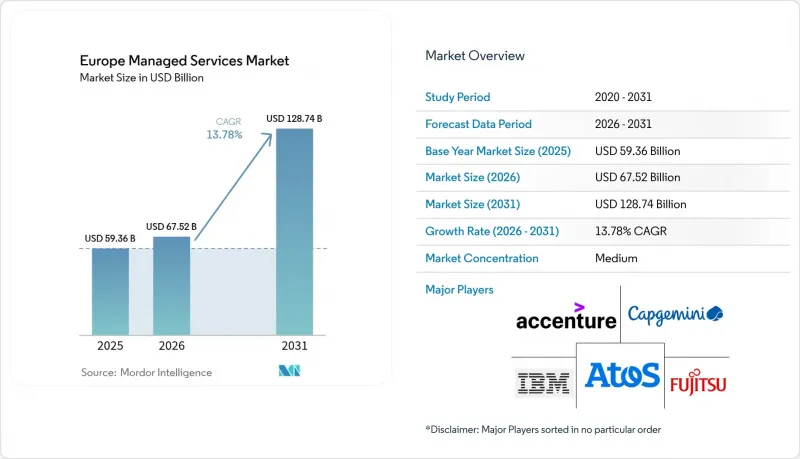

Europe Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe managed services market size is projected to be USD 59.36 billion in 2025, USD 67.52 billion in 2026, and reach USD 128.74 billion by 2031, growing at a CAGR of 13.78% from 2026 to 2031.

Demand is accelerating as organizations migrate from capital-intensive data-center assets to predictable operating-expense agreements that bundle infrastructure, security, and application management. Hybrid and multi-cloud strategies dominate because they let firms balance latency, compliance, and cost while still meeting strict EU data-sovereignty laws. Escalating cyber-threat volumes, the NIS2 Directive, and the Digital Operational Resilience Act are turning managed security into the fastest-growing service line, while EU grants for SME digitalization are widening the customer base. At the same time, edge-cloud data-centers positioned inside sovereign jurisdictions are helping providers support low-latency workloads for manufacturing, financial trading, and telemedicine. Competitive intensity remains moderate; global systems integrators, telecom carriers, and Indian IT services companies are racing to lock in multi-year contracts, often through platform-agnostic alliances with hyperscalers.

Europe Managed Services Market Trends and Insights

Accelerated Adoption of Hybrid and Multi-Cloud Architectures

European enterprises are increasingly distributing workloads across on-premises assets, private clouds, and several public-cloud platforms to align performance with compliance mandates. A PwC survey showed that 68% managed at least three clouds in 2025, but only 22% had enough in-house skills to integrate identity federation, network automation, and disaster-recovery workflows. Managed service providers are stepping in with Kubernetes control planes, unified observability, and cloud brokerage layers that keep data portable, an outcome reinforced by the EU Data Act's anti-lock-in clauses. Financial institutions exemplify the trend by keeping transaction data on-premises while pushing analytics to sovereign zones run by Deutsche Telekom, illustrating why sub-10 ms connectivity and SD-WAN overlays are now must-have features. Because latency budgets are tight, telecom carriers monetize dedicated interconnects as part of bundled managed services, blending network and security SLAs in a single contract.

Rising Demand for Cost Optimization and Predictable OPEX

Cloud overspending is eroding the savings that initially justified migration; Deloitte reported that 54% of European CFOs blew past their 2024 cloud budgets by more than 20%. FinOps modules embedded within managed services continuously right-size compute, enforce tagging for cost show-back, and park non-production workloads during off-peak hours, delivering 15-30% savings without refactoring. Bundled offerings appeal to SMEs that lack procurement teams, essentially converting unpredictable capital outlays into steady monthly fees. Public money amplifies the effect. The European Investment Bank issued EUR 1.2 billion (USD 1.28 billion) in 2025 to subsidize SME cloud uptake, with certified MSP engagement mandated for grant eligibility. Spain, Italy, and Poland, where SME digitization lags Northern Europe, are showing the steepest adoption curves because subsidies sharply lower entry barriers.

Complex EU Data-Sovereignty and Privacy Regulations

The coexistence of GDPR, the EU Data Act, and sector-specific frameworks such as the Medical Device Regulation forces MSPs to maintain separate infrastructure stacks, raising compliance overhead. Germany's BSI bars public-sector workloads from traveling outside sovereign clouds controlled by EU-headquartered operators. France's SecNumCloud certificate adds even stricter controls and can take 18 months to earn. Fragmentation inflates legal costs and stretches procurement cycles because each member state enforces slightly different audit standards. A voluntary CISPE initiative to harmonize certifications is still in pilot, so managed-services rollouts remain slowed by regulatory sprawl.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Cybersecurity Threats Driving Managed Security Uptake

- Shortage of In-House IT Talent Across Europe

- Integration Complexity with Legacy Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid and hosted environments captured 46.32% of Europe managed services market share in 2025, while cloud-only setups are recording a brisk 14.18% CAGR to 2031. Enterprises keep sensitive datasets on-premises to meet GDPR while exploiting cloud burst capacity for analytics. Edge-cloud zones inside telecom exchanges offer sub-5 ms latency and sovereign certifications, letting providers strike a balance between performance and compliance. Hosted deployments keep growing among mid-sized firms that prefer predictable fees without multitenancy risk, particularly in Frankfurt and Amsterdam where colocation capacity expanded in 2025. Although on-premises spending is declining as a share of the Europe managed services market size, absolute dollars remain steady because German manufacturers and Italian banks refresh hardware through managed-infrastructure contracts instead of full cloud migrations.

The Gaia-X federation is reshaping the landscape by certifying interoperable services that combine cloud scale with data-residency guarantees. MSPs now embed Gaia-X-compliant orchestration layers to move workloads among sovereign zones and hyperscaler regions, reinforcing hybrid as the long-term norm. SMEs accelerate straight to cloud because they lack capex budgets, but even they often adopt a light hybrid stance by running backups or sensitive HR data locally. Consequently, the Europe managed services market continues to favor providers that can optimize workload placement across this hybrid continuum.

Managed security held 29.54% revenue share in 2025 and is projected to remain the fastest-growing line at 15.58% CAGR. Regulatory deadlines, ransomware risk, and board-level scrutiny push enterprises to embed 24X7 monitoring, incident response, and forensic analysis within wider infrastructure contracts. Managed data-center services appeal to trading hubs that need low-latency proximity to exchanges in London, Frankfurt, and Paris, while managed network services such as SD-WAN and carrier-neutral interconnects weave together on-premises, edge, and multi-cloud domains. Communications and collaboration services have plateaued after the remote-work boom, causing vendors to shift focus toward real-time translation and contact-center AI.

Managed infrastructure and hosting remain baseline offerings but face commoditization as hyperscalers automate server provisioning through code templates. Consequently, providers differentiate by layering disaster-recovery drills and predictive capacity planning. Managed mobility is growing in healthcare and field services, where remote device provisioning and compliance enforcement are mission-critical. The convergence of managed security and network operations lets MSPs map threat intelligence to traffic anomalies in a single console, a feature regulators are starting to deem essential under DORA.

The Europe Managed Services Market Report is Segmented by Deployment Model (On-Premises, Cloud, and Hybrid/Hosted), Service Type (Managed Data Centre, Managed Security, and More), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), End-User Vertical (BFSI, Manufacturing, and More), and Country (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- IBM Corporation

- Fujitsu Limited

- Capgemini SE

- Atos SE

- Accenture plc

- AT&T Inc.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Microsoft Corporation

- Deutsche Telekom AG

- Orange S.A. (Orange Business Services)

- Tata Consultancy Services Limited

- Wipro Limited

- Cognizant Technology Solutions Corporation

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- NTT Data Corporation

- Tech Mahindra Limited

- DXC Technology Company

- Rackspace Technology, Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- Sopra Steria Group SA

- CGI Inc.

- Kyndryl Holdings, Inc.

- Capita plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of Hybrid and Multi-Cloud Architectures

- 4.2.2 Rising Demand for Cost Optimization and Predictable OPEX

- 4.2.3 Increasing Cybersecurity Threats Driving Managed Security Uptake

- 4.2.4 Shortage of In-House IT Talent Across Europe

- 4.2.5 Emergence of Edge-Cloud Zonal Datacentres for Data-Sovereign Workloads

- 4.2.6 MSP Bundling of AI Ops and FinOps Platforms to Automate Cost Governance

- 4.3 Market Restraints

- 4.3.1 Complex EU Data-Sovereignty and Privacy Regulations

- 4.3.2 Integration Complexity with Legacy Systems

- 4.3.3 Rising Energy Costs Squeezing Data-Centre Service Margins

- 4.3.4 Escalating Carbon-Accounting Scrutiny on Outsourced Workloads

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid/Hosted

- 5.2 By Service Type

- 5.2.1 Managed Data Centre

- 5.2.2 Managed Security

- 5.2.3 Managed Network

- 5.2.4 Managed Communication and Collaboration

- 5.2.5 Managed Infrastructure and Hosting

- 5.2.6 Managed Mobility

- 5.2.7 Managed Cloud and Application

- 5.2.8 Managed Workplace / Service Desk

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-User Vertical

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-Commerce

- 5.4.5 Government and Public Sector

- 5.4.6 IT and Telecom

- 5.4.7 Energy and Utilities

- 5.4.8 Rest of End-User Verticals

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Sweden

- 5.5.8 Russia

- 5.5.9 Poland

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Fujitsu Limited

- 6.4.3 Capgemini SE

- 6.4.4 Atos SE

- 6.4.5 Accenture plc

- 6.4.6 AT&T Inc.

- 6.4.7 Cisco Systems, Inc.

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 Microsoft Corporation

- 6.4.10 Deutsche Telekom AG

- 6.4.11 Orange S.A. (Orange Business Services)

- 6.4.12 Tata Consultancy Services Limited

- 6.4.13 Wipro Limited

- 6.4.14 Cognizant Technology Solutions Corporation

- 6.4.15 Nokia Corporation

- 6.4.16 Telefonaktiebolaget LM Ericsson

- 6.4.17 NTT Data Corporation

- 6.4.18 Tech Mahindra Limited

- 6.4.19 DXC Technology Company

- 6.4.20 Rackspace Technology, Inc.

- 6.4.21 Verizon Communications Inc.

- 6.4.22 Vodafone Group Plc

- 6.4.23 Sopra Steria Group SA

- 6.4.24 CGI Inc.

- 6.4.25 Kyndryl Holdings, Inc.

- 6.4.26 Capita plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment