PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044208

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044208

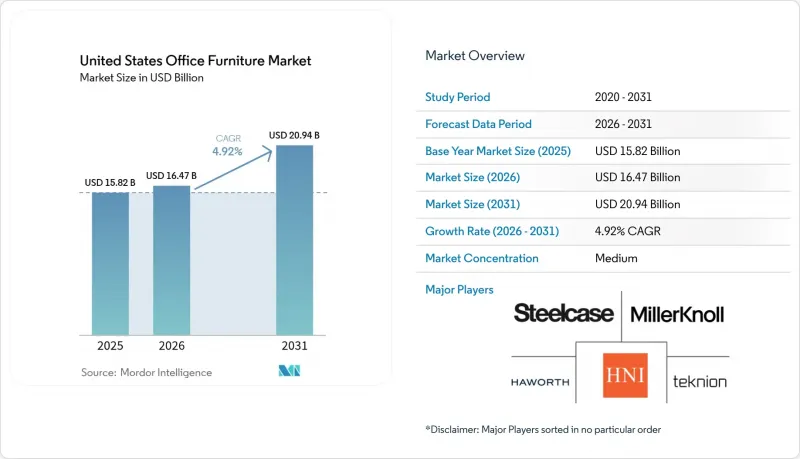

United States Office Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States office furniture market size was USD 15.82 billion in 2025, is set to reach USD 16.47 billion in 2026, and is forecast to rise to USD 20.94 billion by 2031, reflecting a 4.92% CAGR during 2026-2031.

Demand is recalibrating as employers reinforce hybrid attendance and return-to-office rules, which lifts retrofit spending and shifts procurement toward adaptive layouts and ergonomic upgrades that support variable headcounts. Office utilization improved to 53% in 2026, up from depressed 2023 levels, confirming that the United States office furniture market is now driven more by refresh cycles than by new construction starts. Section 179 expensing continues to motivate small- and mid-sized buyers to replace aging workstations without straining operating budgets, while tariff exposure on China-origin inputs and components sustains cost pressure that manufacturers manage through selective nearshoring and pass-through pricing. Regulatory scrutiny of chemicals and indoor air quality standards increases the strategic value of certified materials and documented emissions performance across core categories, which, in turn, guides specifications in public-sector and institutional tenders.

United States Office Furniture Market Trends and Insights

Return-to-Office Refresh Cycles Propel Replacement Demand

Office utilization reached 53% in 2026 as many large employers reinstated minimum on-site attendance to strengthen collaboration, which created a structural pivot toward continuous refresh cycles in the United States office furniture market. Procurement teams are updating open areas and focus zones with modular systems and ergonomic seating that can be reconfigured without disrupting daily operations, a shift that prioritizes agility over long fixed layouts as organizations fine-tune their hybrid models. Steelcase reported higher order activity in the Americas and a year-over-year backlog increase to USD 694 million in fiscal 2025, which signals that refresh spending has moved from deferral to planned programs that support talent engagement and workspace productivity. Competitive differentiation now hinges on product performance and service value rather than features alone, since most buyers require ergonomic baselines and look to installation speed, warranty terms, and post-sale service to decide among similar options in the United States office furniture market. Early adopters are piloting furniture with integrated sensors and device power to enhance comfort and utilization tracking, although adoption remains selective among cost-conscious mid-market buyers who prioritize proven designs and predictable lead times.

Hybrid Work Ergonomics Upgrade Demand Reshapes Product Mix

Hybrid remains the dominant pattern for remote-capable roles, and 52% of such employees worked in hybrid arrangements in 2025, which sustains twin demand for standardized office setups and high-quality home workstations in the United States office furniture market. Corporate buyers now favor plug-and-play stations with height-adjustable desks, lumbar-support chairs, and integrated power modules that maintain consistent ergonomic experiences across floors and sites, reflected in repeat orders for validated SKUs that meet durability benchmarks and certification thresholds. Home office purchases emphasize compact modular systems that deliver function in smaller footprints, which channels incremental volume into brands that can serve both B2B and direct-to-consumer fulfillment with fast shipping and simple assembly in the United States office furniture market. Extended warranties and part-replacement programs now influence selection criteria because buyers seek to extend lifecycle value and reduce unscheduled downtime for high-use seating and desks that support rotating teams. This ergonomic focus favors suppliers that can prove testing, safety, and emissions compliance during RFPs, especially where employee health and comfort are linked to retention goals and hybrid attendance targets in the United States office furniture market.

Elevated Office Vacancy and Footprint Densification Compress Addressable Market

Vacancy rates remain elevated in many markets even as utilization improves, compressing the near-term runway for net new installations and signaling that refresh activity will dominate the United States office furniture market. Many firms are reducing square footage per employee and leaning into hoteling and touchdown concepts, so desks and storage units are refreshed for flexibility rather than expanded for headcount growth across multi-tenant buildings and campuses. This environment creates a two-speed cycle where class A properties invest to attract and retain tenants, while older buildings face longer approval cycles and deferrals that weigh on volume in the United States office furniture market. The installed base still exceeds current occupancy in many corridors, which moderates unit growth even as replacement demand lifts orders for task seating and reconfigurable partitions that support hybrid collaboration. Suppliers that focus on amenity-rich, experience-led spaces and on clients with stable capital plans are better positioned to offset the slow churn in underperforming buildings in the United States office furniture market.

Other drivers and restraints analyzed in the detailed report include:

- Digital Procurement and E-Commerce Penetration Accelerate B2B Transactions

- Sustainability Certifications Shape Buying as Baseline Requirements

- Raw Material and Freight Cost Volatility Erodes Margin Predictability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chairs captured 37.88% of the United States office furniture market share in 2025, confirming their role as the most frequently replaced category and the ergonomic cornerstone of hybrid-ready workplaces. Task seating with adjustable lumbar support and breathable backs has become the baseline specification for enterprise buyers who want consistent comfort across rotating teams, helping keep replenishment cycles aligned with warranty life and health goals across large portfolios. Conference rooms and team areas are upgraded with meeting and guest chairs that balance mobility and durability, enabling space planners to increase throughput while preserving comfort standards in the United States office furniture market. The fastest-growing product grouping is booths and office dividers, which address acoustic privacy and on-demand video needs in open environments where hybrid collaboration increases noise sensitivity. The United States office furniture market for booths and office dividers is projected to expand at a 6.58% CAGR from 2026 to 2031, as buyers favor modular kits that install quickly without permits and support flexible reconfiguration as footprints evolve.

Tables and desks stabilize mid-portfolio demand as height-adjustable platforms penetrate deeper into corporate programs and into home workspaces that mirror in-office ergonomics in the United States office furniture market. Storage evolves as mobile pedestals and lockers replace legacy files in unassigned seating plans, which reinforces the shift toward lighter, more flexible fixtures that can be moved without disrupting IT or HVAC. Sofas and soft seating deliver hospitality cues in reception areas and team lounges, which support the push to make offices more attractive than home environments for high-impact collaboration moments in the United States office furniture industry. The remaining categories, including reception furniture and accessories, benefit from the emphasis on simple upgrades that elevate brand expression with faster lead times and lower risk during phased refresh plans. Across product types, certification and repairability are now table stakes rather than differentiators, as many buyers seek proof of emissions performance and part availability to extend service life in the United States office furniture market.

Wood held 41.26% of the United States office furniture market share in 2025, supported by its durability, finish options, and alignment with premium executive and client-facing spaces where materials act as brand signals. Engineered composites serve cost-focused casegoods and storage, and many buyers now require evidence that substrates meet formaldehyde emission thresholds under federalized TSCA Title VI standards that reflect CARB's long-standing framework. Metal continues to anchor seating frames, storage systems, and durable shelving, and its recyclability appeals to institutional purchasers that value lifecycle economics over initial price in the United States office furniture market. Buyers and suppliers are navigating duty exposure and input volatility by increasing regional sourcing and simplifying finish options to reduce complexity where possible across programmatic orders in the United States office furniture market. The combination of compliance requirements and cost focus steers many specifications toward verified panels and metals that support predictable schedules and post-install satisfaction in the United States office furniture market.

Plastics and polymers have the fastest trajectory, with a 5.74% CAGR during 2026-2031, as suppliers integrate higher recycled content and expand circular design programs that reduce carbon intensity without sacrificing performance. Haworth's closed-loop manufacturing for the Fern chair family, which continuously recycles 14 plastic parts and reduces the product's carbon footprint by 10%, demonstrates how operational innovation can scale circularity while preserving quality standards in the United States office furniture market. Lightweight polymer parts also reduce freight costs and installation labor, two areas of heightened focus as buyers push for faster turnarounds in phased refresh cycles spanning many floors and buildings. Other materials, including glass, acoustic textiles, and composite hybrids, are gaining share in collaboration zones as teams seek sound absorption without sacrificing openness in the United States office furniture market. State-level policies targeting select chemical classes are also shaping material roadmaps and timelines for reformulation across upholstered products and treated surfaces in the United States office furniture market.

The United States Office Furniture Market Report is Segmented by Product (Chairs, Tables, Storage, Sofas, Booths & Dividers, Others), Material (Wood, Metal, Plastic, Others), Price Range (Economy, Mid-Range, Premium), End-User (Corporate, Healthcare, Education, Government, Hospitality, Others), Distribution Channel (B2C Retail, B2B Direct), and Geography. Market Forecasts are Provided in Value (USD).

List of Companies Covered in this Report:

- Steelcase Inc.

- MillerKnoll, Inc.

- Haworth Inc.

- HNI Corporation (HON, Allsteel, Kimball)

- Teknion

- Global Furniture Group

- KI (Krueger International)

- OFS Brands

- Humanscale

- HON Company

- Allsteel Inc.

- National Office Furniture

- Gunlocke

- Nucraft

- Groupe Lacasse

- JSI (Jasper Group)

- AIS (Affordable Interior Systems)

- SitOnIt Seating (Exemplis)

- Inscape

- Safco Products (LDI)

- Workrite Ergonomics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Return-To-Office Refresh Cycles

- 4.2.2 Hybrid Work Ergonomics Upgrade Demand

- 4.2.3 Digital Procurement And E-Commerce Penetration

- 4.2.4 Sustainability Certifications Shaping Buying (Bifma Level, Greenguard)

- 4.2.5 Pfas-Free and Low-Voc Materials Adoption Accelerates Product Refresh

- 4.2.6 Tax-Advantaged Capex (E.G., Section 179) Supports Smb Furniture Purchases

- 4.3 Market Restraints

- 4.3.1 Elevated Office Vacancy And Footprint Densification

- 4.3.2 Raw Material and Freight Cost Volatility

- 4.3.3 Compliance Costs from Chemical Restrictions (PFAS, Vocs)

- 4.3.4 Import Tariff Persistence on China-Origin Inputs/Components

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Chairs

- 5.1.1.1 Employee Chairs

- 5.1.1.2 Meeting Chairs

- 5.1.1.3 Guest Chairs

- 5.1.2 Tables

- 5.1.2.1 Conference Tables

- 5.1.2.2 Desks

- 5.1.2.3 Other Tables

- 5.1.3 Storage Units

- 5.1.3.1 Filing Cabinets

- 5.1.3.2 Bookcases & Shelving

- 5.1.4 Sofas/Soft Seating

- 5.1.5 Booths and Office Dividers

- 5.1.6 Other Office Furniture (Stools, Reception Area Furniture, Accessories, Others)

- 5.1.1 Chairs

- 5.2 By Material

- 5.2.1 Wood

- 5.2.2 Metal

- 5.2.3 Plastic & Polymer

- 5.2.4 Other Materials

- 5.3 By Price Range

- 5.3.1 Economy

- 5.3.2 Mid-range

- 5.3.3 Premium

- 5.4 By End-user

- 5.4.1 Corporate Offices

- 5.4.2 Healthcare Offices

- 5.4.3 Educational Institutions

- 5.4.4 Government & Public Offices

- 5.4.5 Hospitality & Retail Back-office

- 5.4.6 Others

- 5.5 By Distribution Channel

- 5.5.1 B2C / Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Furniture Stores

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B / Directly from Manufacturers

- 5.5.1 B2C / Retail

- 5.6 By Geography

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Steelcase Inc.

- 6.4.2 MillerKnoll, Inc.

- 6.4.3 Haworth Inc.

- 6.4.4 HNI Corporation (HON, Allsteel, Kimball)

- 6.4.5 Teknion

- 6.4.6 Global Furniture Group

- 6.4.7 KI (Krueger International)

- 6.4.8 OFS Brands

- 6.4.9 Humanscale

- 6.4.10 HON Company

- 6.4.11 Allsteel Inc.

- 6.4.12 National Office Furniture

- 6.4.13 Gunlocke

- 6.4.14 Nucraft

- 6.4.15 Groupe Lacasse

- 6.4.16 JSI (Jasper Group)

- 6.4.17 AIS (Affordable Interior Systems)

- 6.4.18 SitOnIt Seating (Exemplis)

- 6.4.19 Inscape

- 6.4.20 Safco Products (LDI)

- 6.4.21 Workrite Ergonomics

7 Market Opportunities & Future Outlook

- 7.1 Furniture-As-A-Service And Leasing Models For Hybrid Demand

- 7.2 Modular Demountable Partitions And Acoustic Pods For Rapid Reconfiguration