PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073565

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073565

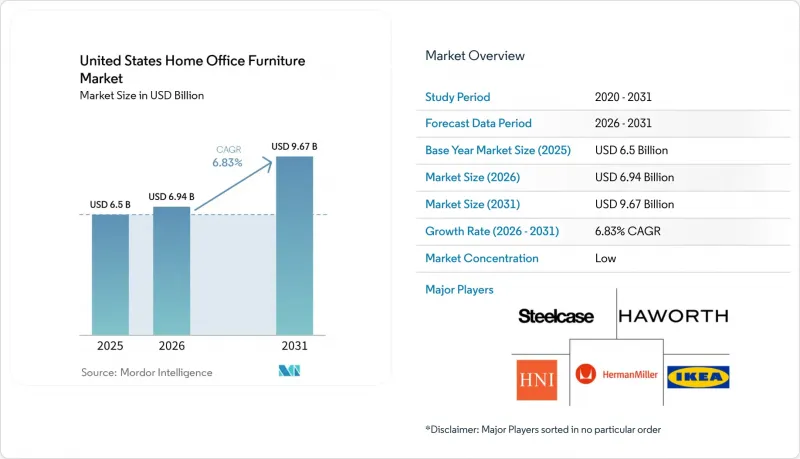

United States Home Office Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states home office furniture market size in 2026 is estimated at USD 6.94 billion, growing from 2025 value of USD 6.5 billion with 2031 projections showing USD 9.67 billion, growing at 6.83% CAGR over 2026-2031.

This report is Segmented by Product (Office Chairs, Desks (Height Adjustable Desks, Fixed Desks), and More), by Material (Wood, Metal, and More), by Price Range (Economy, Mid - Range, and More), by Distribution Channel (Home Centers, Specialty Specialty Stores, and More) and by Geography (Northeast, Southeast, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Home Office Furniture Market Trends and Insights

Adoption of Remote and Hybrid Work Models Accelerates Furniture Purchases

Hybrid attendance policies have become standard across professional services and finance, leaving workplace occupancy well below pre-2020 norms and reshaping demand for office furniture. This permanence has produced a second investment wave in dedicated home workstations as households replace makeshift solutions with furniture tailored to long-term use. As a result, products with residential aesthetics-soft woods, muted palettes, and fabric upholstery-are selling alongside overtly task-oriented items, merging office utility with living-space style. An emerging benefit for retailers is that business-hour demand is smoothing out traditional weekend sales peaks because remote workers browse and buy throughout the workweek

Increased Emphasis on Health and Ergonomics

Rising healthcare premiums and longer screen hours have transformed ergonomics from an optional feature to a primary purchase criterion. Height-adjustable desks, already the fastest-growing product segment at 8.1% CAGR, now ship with digital height presets and activity prompts that position them as wellness devices. Certification marks lend credibility, and employers frequently require such labels before reimbursing purchases, giving certified brands a clear sales edge. A secondary effect is that marketing content focusing on posture education converts shoppers at higher rates, implying that knowledge transfer is now part of the selling proposition.

Housing-Market Slowdown Curtailing Home-Office Upgrades

Elevated mortgage costs have cooled home-sales volumes, postponing the furniture purchases typically linked to moves. Sales data from major mid-tier chains confirm softer order flows tied to new-home completions, even as refurbishment-driven transactions hold steady. The pattern suggests that premium brands insulating their pipeline with upgrade-oriented marketing face less volatility than volume-driven value players that rely on household formations. Manufacturers targeting the middle price band are therefore pivoting to installment-financing options that spread payments over longer terms, cushioning the impact of a sluggish housing cycle.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of E-Commerce Channels

- Low-VOC Standards in California Prompting Premium Sustainable SKUs

- Elevated Lumber & Steel Costs Compressing Manufacturer Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The office-chair category commands 28.55% of the United States home office furniture market share in 2025, a leadership position underpinned by higher replacement frequency and direct links to user comfort. Even as volumes stabilize, seating suppliers that refresh fabric lines and integrate posture sensors find that households willingly upgrade within three-year intervals. Height-adjustable desks, representing the fastest-growing product slot at 7.78% CAGR, infiltrate mid-range portfolios along with programmable height memory, thereby normalizing technology once reserved for executive suites. This acceleration implies that value-tier producers risk obsolescence if they fail to migrate toward even basic sit-stand functionality over the next planning cycle.

A second wave of growth stems from accessories and "other products," such as monitor arms and portable privacy screens, which round out ergonomic ecosystems. Storage cabinets and shelving demonstrate slower but stable demand; still, their bundling with desk sets elevates average sale values and encourages aesthetic uniformity across entire rooms. Auxiliary tables for printers and peripherals remain niche, yet they capture incremental revenue in households dedicating separate zones for scanning and 3-D printing. Overall, integrated power management and wireless-charging hubs embedded in desks and chairs provide tangible proof that digital technology is now inseparable from physical furniture.

Wood maintains a 41.35% share of the United States home office furniture market size because natural grain and perceived durability resonate with domestic consumers. Continuing price inflation for hardwood species has not dampened enthusiasm; instead, buyers equate premium veneer with long-term asset value. Plastic and polymer alternatives, advancing at a 7.01% CAGR, transition from entry-level replacements to credible eco-friendly options thanks to recycled content and bio-resin innovations. Life-cycle assessments published in peer-reviewed journals show that upstream manufacturing stages generate most environmental impact, prompting designers to favor lower-emission polymers where structural strength is non-critical.

Metal frameworks, especially powder-coated steel and anodized aluminum, enjoy persistent demand for structural elements, while their recyclability records offer powerful marketing narratives. Niche materials-including bamboo laminates and mushroom-based composites-capture attention in design media even if current volumes are small, hinting at potential step-change adoption should cost curves fall. Across all substrates, the convergence of sustainability scoring and cost-containment goals drives experimentation, suggesting that hybrid constructions combining wood aesthetics with recycled-plastic cores may soon emerge as mainstream.

Complete Report Scope:

- By Product

- Office Chairs

- Desks

- Height Adjustable Desks

- Fixed Desks

- Tables (side tables, printer tables, etc.)

- Storage Cabinets & Shelving

- Other Products (stools, bookcase, desk accessories, etc.)

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centers

- Specialty Stores (including exclusive brand outlets)

- Online

- Other Distribution Channels

- By Geography

- Northeast

- Southeast

- Midwest

- Southwest

- West

List of Companies Covered in this Report:

- MillerKnoll, Inc.

- Steelcase Inc.

- Haworth Inc.

- HNI Corporation

- Ashley Furniture Industries

- IKEA

- La-Z-Boy Incorporated

- Humanscale Corporation

- Sauder Woodworking Company

- Bush Industries (BBF)

- RH (Restoration Hardware)

- Autonomous Inc.

- THE HON Company

- Martin Furniture

- Hooker Furniture Corporation

- Stuart David Home Furnishings

- Thos. Moser

- Global Furniture Group

- Eureka Ergonomic

- Stakmore

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Remote and Hybrid Work Models Accelerates Furniture Purchases

- 4.2.2 Increased Emphasis on Health and Ergonomics

- 4.2.3 Product Innovations Focus on Space Optimization and Functional Designs

- 4.2.4 Expansion of E-Commerce Channels

- 4.2.5 Low-VOC Standards in California Prompting Premium Sustainable SKUs

- 4.3 Market Restraints

- 4.3.1 Housing-Market Slowdown Curtailing Home-Office Upgrades

- 4.3.2 Elevated Lumber & Steel Costs Compressing Manufacturer Margins

- 4.3.3 Low-Cost Asian Imports Saturating Entry-Level Desk Segment

- 4.3.4 Expansion of Second-Hand & Furniture-Rental Platforms Cannibalising New Sales

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (new product launches, investment, capacity expansion, partnerships, acquisitions, etc.) in the Industry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Office Chairs

- 5.1.2 Desks

- 5.1.2.1 Height Adjustable Desks

- 5.1.2.2 Fixed Desks

- 5.1.3 Tables (side tables, printer tables, etc.)

- 5.1.4 Storage Cabinets & Shelving

- 5.1.5 Other Products (stools, bookcase, desk accessories, etc.)

- 5.2 By Material

- 5.2.1 Wood

- 5.2.2 Metal

- 5.2.3 Plastic & Polymer

- 5.2.4 Other Materials

- 5.3 By Price Range

- 5.3.1 Economy

- 5.3.2 Mid-Range

- 5.3.3 Premium

- 5.4 By Distribution Channel

- 5.4.1 Home Centers

- 5.4.2 Specialty Stores (including exclusive brand outlets)

- 5.4.3 Online

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 Northeast

- 5.5.2 Southeast

- 5.5.3 Midwest

- 5.5.4 Southwest

- 5.5.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 MillerKnoll, Inc.

- 6.4.2 Steelcase Inc.

- 6.4.3 Haworth Inc.

- 6.4.4 HNI Corporation

- 6.4.5 Ashley Furniture Industries

- 6.4.6 IKEA

- 6.4.7 La-Z-Boy Incorporated

- 6.4.8 Humanscale Corporation

- 6.4.9 Sauder Woodworking Company

- 6.4.10 Bush Industries (BBF)

- 6.4.11 RH (Restoration Hardware)

- 6.4.12 Autonomous Inc.

- 6.4.13 THE HON Company

- 6.4.14 Martin Furniture

- 6.4.15 Hooker Furniture Corporation

- 6.4.16 Stuart David Home Furnishings

- 6.4.17 Thos. Moser

- 6.4.18 Global Furniture Group

- 6.4.19 Eureka Ergonomic

- 6.4.20 Stakmore

7 Market Opportunities & Future Outlook

- 7.1 Adoption of Smart and Technology-Integrated Workstations

- 7.1.1 Rising Demand for Modular and Customizable Furniture Solutions

- 7.1.2 Growing Integration of Home Office Furniture with Interior Decor Trends Enhances Consumer Appeal