PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044217

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044217

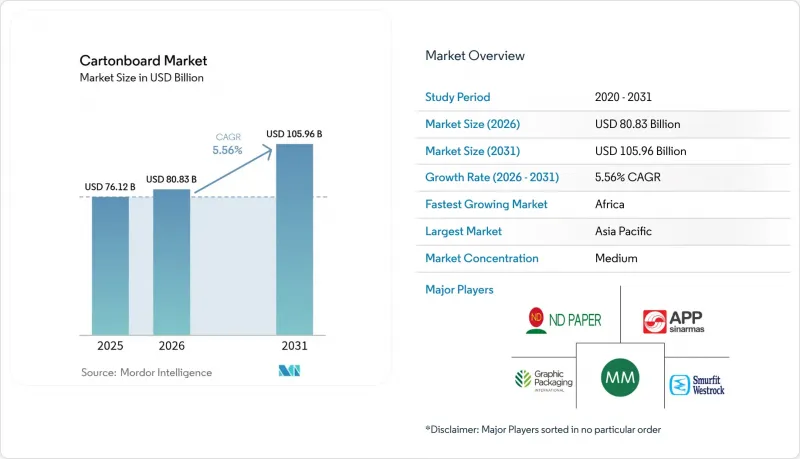

Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The cartonboard market size is projected to be USD 76.12 billion in 2025, USD 80.83 billion in 2026, and reach USD 105.96 billion by 2031, growing at a CAGR of 5.56% from 2026 to 2031.

Strong policy pressure for full recyclability, mounting consumer preference for plastic-free packs, and widespread e-commerce lightweighting are steering brand owners toward fiber-based solutions. Folding cartons, sleeves, and liquid packs made from barrier-coated board are displacing rigid polyethylene terephthalate and polypropylene formats, especially in food, beverage, and cosmetics channels. Digital printing presses are unlocking profitable micro-runs for direct-to-consumer brands, while high-yield microfibrillated cellulose enables 10%-15% basis-weight cuts that translate into lower dimensional-weight freight charges. On the supply side, virgin-fiber mills continue to win premium orders in pharmaceuticals and luxury goods, whereas integrated recyclers bank on optical sorting to offset declining bale quality.

Global Cartonboard Market Trends and Insights

E-commerce Corrugated-to-Cartonboard Substitution Surge

Direct-to-consumer networks are trading double-wall corrugated boxes for single-wall cartonboard sleeves that trim parcel mass by 20%-30%, lowering carrier dimensional-weight fees. Amazon and Alibaba now deploy paper void fill in lieu of plastic air pillows, driving 3.9% annual growth in cushioning grades. Nike and Apple redesigned apparel and electronics packs to remove corrugated altogether, opening demand pockets for 200-250 g-per-m2 folding boxboard with adequate stacking strength. The shift is creating fresh revenue for mills able to supply high-bulk, lightweight board in North American and European metro zones where same-day delivery dominates.

FMCG Pivot to Plastic-Free Primary Packaging

Global consumer-goods groups are retrofitting SKUs with dispersion-coated board that preserves grease, moisture, and oxygen barriers without polyethylene layers. Stora Enso's Performa Lumi, released January 2026, offers mineral pigment opacity tailored to beauty labels. Henkel rolled out paper cartridges for adhesives in October 2025, eliminating 120 tons of plastic per year. The European Packaging and Packaging Waste Regulation obliges all packs to be recyclable by 2030, accelerating board uptake despite a 4-5 x unit-cost premium relative to polyolefins.

Energy-Price Volatility Squeezing Mill Margins

Electricity and gas form 10%-15% of mill outlays. U.S. natural gas averaged USD 3.30 per MMBtu in January 2025, far below the USD 9.50 August 2022 peak, yet European power prices remain elevated. Integrated producers with captive generation or renewables PPAs shield margins, whereas stand-alone recyclers exposed to spot rates face compressed spreads.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Drives Logistics Cost Savings

- Regional Single-Use-Plastic Bans

- Chronic Recycled-Fiber Supply Imbalance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virgin fiber captured rising demand for liquid packaging board and solid bleached board, expanding at a forecast 5.93% CAGR as beverage and pharmaceutical buyers insist on brightness and tensile integrity. Billerud's FSC-certified Enviro-FBB has secured cosmetics contracts that emphasize opacity for shelf appeal. Sappi's 520,000-short-ton Somerset mill addition in 2024 widened U.S. supply of FDA-compliant substrates. Although recycled grades hold 57.82% of 2025 volume, elevated contamination and fiber fatigue hamper their suitability for high-brightness applications. DS Smith's commitment to 100% recycled fiber in containerboard underscores its cost edge, yet the cartonboard market size attached to virgin folds still outpaces recycled in profit per ton.

Recycled fiber maintains leadership in folding boxboard where unit economics dominate, and Graphic Packaging extracts 80% of input from recovered streams while sustaining brightness above 80 ISO through advanced de-inking. Nine Dragons Paper operates 160 Asian sites processing domestic and North American post-consumer bales. The cartonboard market share of recycled medium will stay resilient, but virgin capacity is likely to win incremental value in premium niches subject to stringent FDA or EU food-contact rules.

Solid bleached board (SBB) is projected to clock the fastest 6.72% CAGR to 2031, driven by luxury cosmetics and pharma packs that prize pure-white aesthetics. Sappi's Somerset expansion directly feeds this surge, supplying blister cards and food trays that demand rigidity and FDA clearance. Folding boxboard (FBB) retained a 38.13% slice of the 2025 cartonboard market size owing to its versatility across cereal, confectionery, and frozen meals. Stora Enso's FiberLight-based Performa Nova helped converters shave 10%-15% material use without sacrificing bend stiffness.

Liquid packaging board thrives on Elopak's Natural White Board that trims greenhouse gases by 14% per unit relative to PET bottles. White-lined chipboard services cost-sensitive food sectors, while food service board steps in for polystyrene clamshells under African and Asian plastic bans. Despite SBB's growth momentum, FBB will remain the volume backbone as converters exploit its fine balance of stiffness, runnability, and graphic punch.

The Cartonboard Market Report is Segmented by Material (Virgin Fiber, and Recycled Fiber), Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, and More), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 43.62% of 2025 revenue, underpinned by China's 8% capacity additions and India's 24 million-t packaging consumption. Local mills benefit from government incentives for energy-efficient machines, and regional recyclers are expanding de-inking to offset import restrictions on old corrugated containers. Japan, South Korea, and Australia post recycling rates above 70%, enabling high substitution of recycled fiber in FBB grades, thereby bolstering the regional cartonboard market.

Africa is projected to expand fastest at 6.57% through 2031. Kenya's plastics ban catalyzes folding carton demand, and South Africa's USD 2.5 billion paper sector attracts Mondi and Sappi investments. Nigeria, Egypt, and Ethiopia record double-digit FMCG volume growth, stimulating need for secondary packs that withstand hot-chain logistics. Middle East markets such as Saudi Arabia and the United Arab Emirates will grow 5.8% as retail chains proliferate and e-commerce accelerates.

North America and Europe are consolidating capacity while funneling capital into digital presses and barrier-coat lines. International Paper removed 1 million t of legacy containerboard in 2024 and Packaging Corporation of America acquired Greif's unit for USD 1.8 billion to tighten supply. Europe's 72% paper recycling rate complements its Packaging Waste Regulation, which obliges recyclability by 2030. South America is buoyed by Klabin's 900,000-t PUMA II line due in 2027, positioning Brazil as an export platform to North Atlantic buyers.

- Asia Pulp & Paper Company Ltd.

- Mayr-Melnhof Karton AG

- Nine Dragons Paper (Holdings) Limited

- Smurfit WestRock

- Graphic Packaging Holding Company

- Stora Enso Oyj

- International Paper Company

- Metsa Board Corporation

- Pankaboard Oyj

- Klabin S.A.

- Oji Holdings Corporation

- Mondi plc

- Rengo Co., Ltd.

- Lee & Man Paper Manufacturing Ltd.

- Georgia-Pacific LLC

- Clearwater Paper Corporation

- Sappi Limited

- Holmen AB

- DS Smith plc

- Huhtamaki Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Corrugated-to-Cartonboard Substitution Surge

- 4.2.2 FMCG Pivot to Plastic-Free Primary Packaging

- 4.2.3 Lightweighting Drives Logistics Cost Savings

- 4.2.4 Regional Single-Use-Plastic Bans

- 4.2.5 High-Speed Digital Printing Unlocks SKU Proliferation

- 4.2.6 Luxury Goods' Demand for Premium Folding Cartons

- 4.3 Market Restraints

- 4.3.1 Energy-Price Volatility Squeezing Mill Margins

- 4.3.2 Chronic Recycled-Fiber Supply Imbalance

- 4.3.3 Capital-Intensive Barrier Coatings Compliance

- 4.3.4 Converters' Shift to Molded-Fiber Alternatives

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Investment Analysis

- 4.7 Industry Value / Supply-Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fiber

- 5.1.2 Recycled Fiber

- 5.2 By Product Grade

- 5.2.1 Solid Bleached Board

- 5.2.2 Solid Unbleached Board

- 5.2.3 Folding Boxboard

- 5.2.4 White-Lined Chipboard

- 5.2.5 Liquid Packaging Board

- 5.2.6 Food Service Board

- 5.3 By Packaging Format

- 5.3.1 Folding Cartons

- 5.3.2 Liquid Packaging

- 5.3.3 Sleeve and Tray

- 5.3.4 Other Packaging Format

- 5.4 By End-User Industry

- 5.4.1 Beverage

- 5.4.2 Food

- 5.4.3 Pharmaceutical and Healthcare

- 5.4.4 Cosmetics and Toiletries

- 5.4.5 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Asia Pulp & Paper Company Ltd.

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Nine Dragons Paper (Holdings) Limited

- 6.4.4 Smurfit WestRock

- 6.4.5 Graphic Packaging Holding Company

- 6.4.6 Stora Enso Oyj

- 6.4.7 International Paper Company

- 6.4.8 Metsa Board Corporation

- 6.4.9 Pankaboard Oyj

- 6.4.10 Klabin S.A.

- 6.4.11 Oji Holdings Corporation

- 6.4.12 Mondi plc

- 6.4.13 Rengo Co., Ltd.

- 6.4.14 Lee & Man Paper Manufacturing Ltd.

- 6.4.15 Georgia-Pacific LLC

- 6.4.16 Clearwater Paper Corporation

- 6.4.17 Sappi Limited

- 6.4.18 Holmen AB

- 6.4.19 DS Smith plc

- 6.4.20 Huhtamaki Oyj

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment