PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062184

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062184

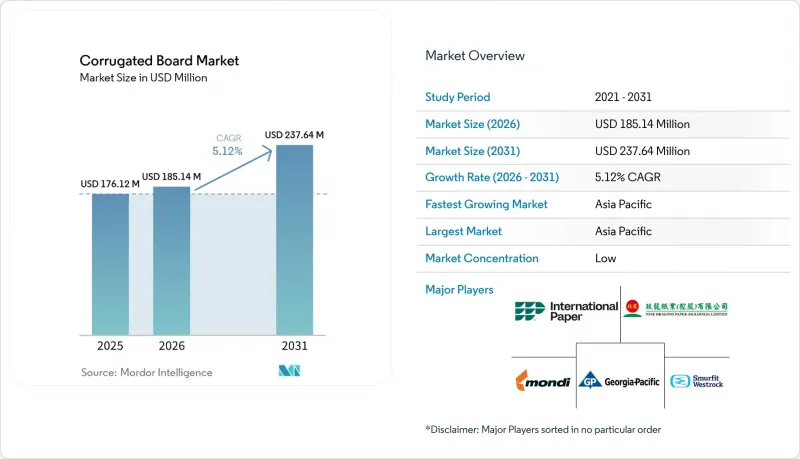

Corrugated Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the corrugated board market size is projected to be USD 176.12 million in 2025, USD 185.14 million in 2026, and reach USD 237.64 million by 2031, growing at a CAGR of 5.12% from 2026 to 2031.

This report is Segmented by Board Type (Single-Wall, Double-Wall, and Triple-Wall), Material Type (Linerboard, Medium, Recycled Fiber, and Virgin Fiber), End-User Industry (Food and Beverage, E-Commerce and Retail, Consumer Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Corrugated Board Market Trends and Insights

Explosive Growth of E-Commerce Shipments

Integrated right-sizing systems from Packsize and Panotec cut board blanks within 5 millimeters of SKU dimensions, lowering void fill by up to 40% and reducing dimensional-weight surcharges levied by global couriers. China's export of 1,274,503 containers of paper packaging in 2025 dwarfed India's 272,348 tally, underscoring the region's infrastructure depth. QR-coded single-pass digital presses from Canon and Domino now personalize B-flute and E-flute cartons at 200 meters per minute, turning shipping boxes into marketing assets. These advances collectively keep the corrugated board market aligned with parcel-volume expansion across continents.

Sustainability Regulations Favouring Paper Recycling

The EU's Packaging and Packaging Waste Regulation 2025/40 mandates 85% collection for paper by 2030 and bans non-recyclable formats by 2030, escalating demand for recycled linerboard. U.S. states such as California, Maine, and Oregon shifted recycling costs to brand owners via extended producer responsibility schemes effective 2024-2026, steering procurement toward high-recovery substrate. Recycled-fiber capacity additions totaling 3.6 million tons since 2017 have already lowered containerboard carbon intensity by up to 20. PFAS bans in food-contact packaging, effective January 2026, further boost aqueous-coated corrugated pizza and take-out boxes. ISO 14001 certification and forest-chain traceability now appear in nearly every multinational procurement tender, embedding sustainability as a competitive necessity.

Competition from Flexible Plastic Mailers

Polyethylene mailers captured 8-12% of North American lightweight parcels in 2025, delivering 30-40% cost savings against single-wall corrugated in sub-2 kg bands. Dimensional shipping charges favor flexible pouches that hug apparel contours, saving USD 0.50-1.00 on residential deliveries. Yet Maine, Oregon, and Colorado now assess USD 0.02-0.05 recycling fees per plastic mailer, narrowing economics and prompting Amazon to test fiber-padded mailers eligible for curbside recycling. The EU Single-Use Plastics Directive layers similar EPR levies, nudging brands toward micro-flute cartons as thin as 1.5 millimeters that meet automated sortation rigors. Corrugated converters that match mailer thickness reclaim volumes otherwise lost to plastic.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Food and Beverage Distribution in Emerging Markets

- Shift Toward Lightweight, Cost-Efficient Packaging

- Carbon Border Taxes on Paper Exports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-wall held 49.11% revenue in 2025, yet double-wall is growing at a 5.43% CAGR to 2031 as appliance shippers consolidate two cartons into one reinforced unit that still meets Amazon's Frustration-Free 2.0 metrics. Triple-wall remains niche for chemical drums and auto parts requiring burst strength above 1,000 kPa. Engineered BC-flute replaces AC-flute in electronics, trimming impact damage by up to 40% and enhancing shelf presentation.

Micro-flute E- and F-profiles are penetrating cosmetics and pharma because they permit high-definition litho and rigid micro-cartons. Smurfit Westrock shuttered 600,000 tons of legacy C-flute capacity in 2024 while funding B-flute upgrades that serve premium direct-to-consumer channels. Fewer, stronger cartons reduce freight cube and align with sustainability goals, giving double-wall formats durable tailwinds inside the corrugated board market.

Geography Analysis

Asia-Pacific commanded 50.24% of revenue in 2025 and is projected to grow at a 5.88% CAGR through 2031, lifted by China's vast export base and India's PLI-driven electronics clusters. Japan's Rengo opened a heavy-duty plant in Germany in 2025, underscoring outbound investments aimed at serving European auto clients. South Korea's container exports back its role as electronics-packaging hub.

North America faces linerboard price hikes yet benefits from Amazon's fulfillment build-out and nearshored Mexican manufacturing. International Paper's USD 9.9 billion DS Smith deal adds transatlantic scale and USD 514 million. Capacity closures totaling 4 million tons keep supply tight, reinforcing disciplined pricing.

Europe grapples with PPWR recyclability mandates and CBAM levies. Mondi's EUR 1.2 billion capex at Steti and Duino aligns with low-carbon trends, while its EUR 634 million acquisition of Schumacher accelerates access to premium converters. Nordic mills like Stora Enso's Oulu 750,000 tpa board line capitalize on integrated pulp energy efficiencies. South America benefits from Klabin's Puma II export flows, whereas the Middle-East builds industrial carton capacity for Vision 2030 infrastructure. These regional dynamics jointly influence the corrugated board market trajectory.

- Georgia-Pacific LLC

- International Paper

- Klabin S.A.

- Mondi

- Nine Dragons Worldwide (China) Investment Group Co., Ltd.

- NIPPON PAPER INDUSTRIES CO., LTD.

- Oji Holdings Corporation

- Ondupack

- Packaging Corporation of America

- Pratt Industries, Inc.

- Rengo Co., Ltd.

- Saica

- Smurfit Westrock

- Stora Enso

- Thai Containers Group Co., Ltd.

- Visy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth of E-Commerce Shipments

- 4.2.2 Sustainability Regulations Favouring Paper Recycling

- 4.2.3 Expansion of Food and Beverage Distribution in Emerging Markets

- 4.2.4 Shift Toward Lightweight, Cost-Efficient Packaging

- 4.2.5 On-Demand Digital Printing Custom Packs

- 4.3 Market Restraints

- 4.3.1 Kraft Linerboard Price Volatility

- 4.3.2 Competition from Flexible Plastic Mailers

- 4.3.3 Carbon Border Taxes on Paper Exports

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Board Type

- 5.1.1 Single-wall

- 5.1.2 Double-wall

- 5.1.3 Triple-wall

- 5.2 By Material Type

- 5.2.1 Linerboard

- 5.2.2 Medium

- 5.2.3 Recycled Fiber

- 5.2.4 Virgin Fiber

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage

- 5.3.2 E-commerce and Retail

- 5.3.3 Consumer Electronics

- 5.3.4 Personal Care and Household

- 5.3.5 Industrial and Heavy-Duty

- 5.3.6 Pharmaceuticals and Healthcare

- 5.3.7 Other (Furniture, Agriculture, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Georgia-Pacific LLC

- 6.4.2 International Paper

- 6.4.3 Klabin S.A.

- 6.4.4 Mondi

- 6.4.5 Nine Dragons Worldwide (China) Investment Group Co., Ltd.

- 6.4.6 NIPPON PAPER INDUSTRIES CO., LTD.

- 6.4.7 Oji Holdings Corporation

- 6.4.8 Ondupack

- 6.4.9 Packaging Corporation of America

- 6.4.10 Pratt Industries, Inc.

- 6.4.11 Rengo Co., Ltd.

- 6.4.12 Saica

- 6.4.13 Smurfit Westrock

- 6.4.14 Stora Enso

- 6.4.15 Thai Containers Group Co., Ltd.

- 6.4.16 Visy

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment