PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044220

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044220

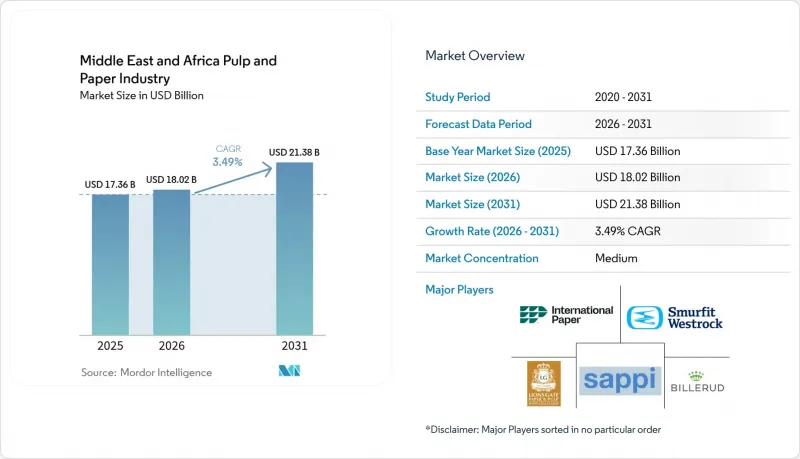

Middle East And Africa Pulp And Paper Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Middle East and Africa pulp and paper market size is projected to expand from USD 17.36 billion in 2025 and USD 18.02 billion in 2026 to USD 21.38 billion by 2031, registering a CAGR of 3.49% between 2026 and 2031.

Structural fiber shortages keep recovered-paper imports elevated, while sovereign capital in the Gulf Cooperation Council (GCC) bankrolls integrated mills and alternative-fiber pilots that temper raw-material risk. Rising e-commerce parcel volumes in South Africa and Saudi Arabia, single-use plastic bans in Kenya and the United Arab Emirates (UAE), and steady population growth across North and East Africa underpin boxboard, cartonboard, and tissue consumption. Currency depreciation in several African markets compresses converter margins but also accelerates import-substitution investments as producers seek to localize feedstock, energy, and logistics. Freight disruption on Red Sea lanes has reinforced the strategic premium on regional self-sufficiency, prompting leading mills to diversify shipping routes and sign longer-tenor supply contracts with Gulf and Indian suppliers.

Middle East And Africa Pulp And Paper Industry Trends and Insights

Growing E-Commerce Packaging Demand

Rapid digital-commerce adoption is rewriting corrugated-box demand curves. Domestic containerboard output in South Africa cannot keep pace with the 30% jump in online sales volume, prompting converters to source linerboard from Southeast Asia at elevated freight premiums. GCC logistics reforms that target faster customs clearance are expected to triple intra-regional parcel flows, encouraging mills to invest in light-weight, high-strength grades that trim shipping weight U.AE. The African Continental Free Trade Area (AfCFTA) digital-trade protocol further accelerates last-mile logistics into landlocked economies, reinforcing containerboard as the backbone of retail fulfillment packaging. Producers that couple post-consumer fiber procurement with automated fluting lines are best positioned to capture this incremental tonnage.

Rising Urban Middle-Class Consumption of Tissue Products

Urbanization in sub-Saharan Africa surpassed 43% in 2024, yet household tissue use still trails the global average by a wide margin. New tissue machines in Saudi Arabia and Kuwait deploy through-air-drying and structured-roll technologies that yield premium softness with lower fiber input, enabling mills to differentiate on quality while defending margins. Multinational hygiene brands report mid-single-digit regional sales growth, validating demand resilience even amid currency volatility. With hospitality pipelines expanding across GCC tourism hubs, away-from-home tissue demand is also rising, supporting diversified grade portfolios.

Chronic Water-Stress in MENA Limiting Mill Permitting

Middle East and North Africa (MENA) freshwater availability is forecast to slip below the 500 m3 per-capita scarcity threshold by 2030, forcing regulators to tighten industrial effluent limits. Egypt has already delayed several high-capacity pulp projects until mills can prove desalination or wastewater-reuse solutions. Because chemical pulping consumes roughly three times as much water as recycled-fiber lines, investors increasingly favor recovered-paper plants and non-wood feedstocks such as date-palm residues that require minimal bleaching. The cap-ex premium for water treatment, combined with rising desalinated-water tariffs, weighs on expansion economics and nudges project pipelines toward lower-intensity technologies.

Other drivers and restraints analyzed in the detailed report include:

- Government Bans on Single-Use Plastics Shifting Demand to Paper-Based Substitutes

- Surge in GCC Investment into Integrated Pulp and Paper Capacity

- Port Congestion and Red Sea Security Surcharges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled pulp secured the largest slice of 2025 revenue, reflecting chronic fiber shortages and EPR rules that incentivize post-consumer collection networks U.AE. Multiple mills upgraded drum pulpers and screening lines to handle mixed-paper bales imported from Europe, tightening loop economics and improving furnish quality. On the premium end, dissolving wood pulp is on track for the quickest growth, buoyed by viscose-staple-fiber expansion in Turkish and Egyptian textile clusters that target European apparel brands seeking sustainable cellulose inputs. The Middle East and Africa pulp and paper market size for dissolving wood pulp is projected to expand at a 4.43% CAGR through 2031, supported by a 110,000-tonne capacity addition at Sappi's Saiccor mill. Alternative fibers such as date-palm residues promise to displace up to 8% of imported wood chips once commercial trials reach scale, offering mills a hedge against volatile international chip prices.

The grade mix continues to favor closed-loop solutions. Integrated GCC projects pair Kraft lines with recycled furnish to flex grades in response to spot-pulp swings, while African converters rely on swing imports until local forestry programs mature. Government R&D grants in the UAE support solvent-based delignification of agricultural waste, with pilot runs demonstrating pulp yields above 50% and water savings of nearly 60% versus hardwood kraft U.AE.

Containerboard commanded 31.12% of 2025 application turnover, anchored by food-export packaging and surging e-commerce volumes. The Middle East and Africa pulp and paper market share for this segment is forecast to remain dominant as GCC mills add nearly 900,000 tpa of testliner and fluting by 2028. Lightweight, high-burst grades below 125 gsm are gaining ground among parcel shippers seeking freight savings, nudging furnish recipes toward higher recycled-fiber ratios. Tissue, however, exhibits the fastest trajectory at a 4.61% CAGR. Retail shelves across Kenya, Nigeria, and Egypt are broadening SKU ranges from economy one-ply to premium three-ply rolls, lifting average value per tonne. Tourism-led demand in the UAE and Saudi Arabia is driving growth in away-from-home products such as napkins and towels, prompting mills to commission energy-efficient crescent-former machines.

Printing and writing papers see secular volume erosion but remain relevant in textbook contracts funded by African education ministries. Specialty papers, though low in tonnage, deliver margins two to three times those of containerboard, prompting converters in Egypt and South Africa to install silicone-coating and security-thread embedding lines that serve regional label and banknote markets.

The Middle East and Africa Pulp and Paper Market Report is Segmented by Grade (Mechanical Pulp, Recycled Pulp, and More), Application (Newsprint, Tissue, and More), End-User Industry (Hygiene Products, Publishing and Education, and More), Product Type (Graphic Papers, Packaging Papers, and More), Process Technology (Chemical Pulping, and Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Smurfit WestRock

- International Paper Company

- Lions Gate Paper & Pulp LLC

- Sappi Limited

- Billerud AB

- Stora Enso Oyj

- Mondi plc

- Oji Holdings Corporation

- Resolute Forest Products Inc.

- Svenska Cellulosa Aktiebolaget SCA

- Nine Dragons Paper (Holdings) Limited

- Asia Pulp & Paper Co., Ltd.

- Kimberly-Clark Corporation

- Pro-Gest S.p.A.

- Metsa Group

- Lee & Man Paper Manufacturing Ltd.

- Mercer International Inc.

- Packaging Corporation of America

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing e-commerce packaging demand

- 4.2.2 Rising urban middle-class consumption of tissue products

- 4.2.3 Government bans on single-use plastics shifting demand to paper-based substitutes

- 4.2.4 Surge in GCC investment into integrated pulp and paper capacity

- 4.2.5 Date-palm agri-residue trials lowering fibre deficit

- 4.2.6 Maritime Free-Zone circular-economy incentives

- 4.3 Market Restraints

- 4.3.1 Volatile wood-chip import prices

- 4.3.2 Chronic water-stress in MENA limiting mill permitting

- 4.3.3 Port congestion and Red-Sea security surcharges

- 4.3.4 Currency depreciation in key African markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Grade

- 5.1.1 Bleached Chemical Pulp (BCP)

- 5.1.2 Dissolving Wood Pulp (DWP)

- 5.1.3 Unbleached Kraft Pulp

- 5.1.4 Mechanical Pulp

- 5.1.5 Recycled Pulp

- 5.2 By Application

- 5.2.1 Printing and Writing

- 5.2.2 Newsprint

- 5.2.3 Tissue

- 5.2.4 Cartonboard

- 5.2.5 Containerboard

- 5.2.6 Specialty Papers

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage Packaging

- 5.3.2 Consumer Goods Packaging

- 5.3.3 Hygiene Products

- 5.3.4 Publishing and Education

- 5.3.5 Industrial and Specialty Applications

- 5.4 By Product Type

- 5.4.1 Graphic Papers

- 5.4.2 Packaging Papers

- 5.4.3 Tissue Papers

- 5.4.4 Specialty Papers

- 5.5 By Process Technology

- 5.5.1 Chemical Pulping

- 5.5.2 Mechanical Pulping

- 5.5.3 Recycled Fibre Processing

- 5.5.4 Integrated Pulp and Paper Mills

- 5.6 By Geography

- 5.6.1 Middle East

- 5.6.1.1 Saudi Arabia

- 5.6.1.2 United Arab Emirates

- 5.6.1.3 Turkey

- 5.6.1.4 Rest of Middle East

- 5.6.2 Africa

- 5.6.2.1 South Africa

- 5.6.2.2 Kenya

- 5.6.2.3 Rest of Africa

- 5.6.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock

- 6.4.2 International Paper Company

- 6.4.3 Lions Gate Paper & Pulp LLC

- 6.4.4 Sappi Limited

- 6.4.5 Billerud AB

- 6.4.6 Stora Enso Oyj

- 6.4.7 Mondi plc

- 6.4.8 Oji Holdings Corporation

- 6.4.9 Resolute Forest Products Inc.

- 6.4.10 Svenska Cellulosa Aktiebolaget SCA

- 6.4.11 Nine Dragons Paper (Holdings) Limited

- 6.4.12 Asia Pulp & Paper Co., Ltd.

- 6.4.13 Kimberly-Clark Corporation

- 6.4.14 Pro-Gest S.p.A.

- 6.4.15 Metsa Group

- 6.4.16 Lee & Man Paper Manufacturing Ltd.

- 6.4.17 Mercer International Inc.

- 6.4.18 Packaging Corporation of America

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment