PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044228

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044228

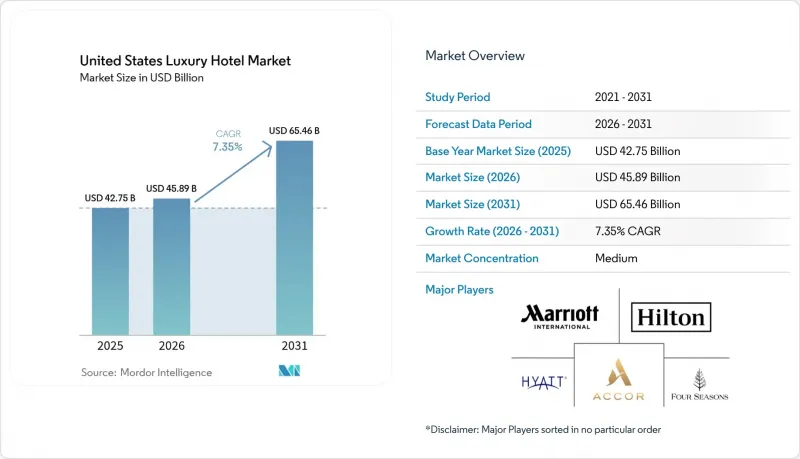

United States Luxury Hotel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States luxury hotel market size was USD 45.89 billion in 2026, up from USD 42.75 billion in 2025, and it is projected to reach USD 65.46 billion by 2031 at a 7.35% CAGR.

This growth pace surpassed the broader United States hotel sector, where RevPAR growth across all categories averaged 0.5% in 2025. Share gains from direct digital bookings, asset-light expansion strategies, and brand-led mixed-use projects have improved yield resilience across cycles within the United States luxury hotel market. Corporate travelers blending business and leisure have extended average stays and lifted ancillary revenue, supporting premium pricing within the United States luxury hotel market. Regionally, the South led in 2025, while the West is the fastest-growing region into 2031, a pattern that informs brand development and capital allocation in the United States luxury hotel market.

United States Luxury Hotel Market Trends and Insights

Experiential luxury demand surges, driven by rising wealth among UHNW individuals and millennials

Affluent travelers in 2026 continue to prioritize high-quality experiences that combine wellness, privacy, and personalization, which sustains premium pricing across the United States luxury hotel market. Brand portfolios that curate bespoke wellness and culinary programs have seen a stronger rate integrity because high-spend guests value distinct experiences over standardized services within the United States luxury hotel market. Younger affluent cohorts define luxury around comfort, design, and access to wellness rather than legacy status, which is reshaping product mix and amenity design for new-builds and renovations in the United States luxury hotel market. Operators that combine discrete service with privacy-forward room categories secure longer stays and steadier repeat visitation from these guests. Portfolio expansion focused on conversions and signings adds supply that targets this preference shift while keeping capital intensity in check across the United States luxury hotel market.

Corporate "bleisure" policies lead to an uptick in long-stay luxury room bookings

Bleisure adoption has become a structural driver, with 62% of United States business travelers blending leisure in 2024 and 42% adding personal days, which lengthens stay patterns and boosts ancillary revenue for luxury properties positioned to serve both needs. Hotels report a high propensity for guests to extend at the same property during bleisure trips, and a large share of these travelers used the same hotel for added nights in 2025, reinforcing loyalty and direct engagement. Extended-stay performance has remained healthier than broader categories, supported by corporate accounts and longer booking windows through late 2024, which favors upscale suite products. The result is steadier weekday occupancy, two extra nights per trip on average in many corporate use cases, and stronger spend across dining, spa, and on-property experiences at higher-tier hotels. These dynamics give the United States luxury hotel market better demand visibility, which supports revenue management discipline and ADR consistency across the calendar.

Ultra-luxury vacation rentals and branded residences intensify competition

Private villas and branded residences offer privacy, space, and dedicated service that appeal to affluent travelers who value seclusion and bespoke experiences, which increases substitution risk at the high end of the United States luxury hotel market. Hotels face intensified competition in coastal and mountain destinations where larger accommodations and private access are viewed as core benefits. Platforms and professional managers support concierge-level service and curated experiences, which narrows service differentiation versus top-tier hotels in these locations. Luxury hotel operators respond by strengthening suite and villa inventory, deepening loyalty benefits, and emphasizing integrated wellness, culinary range, and on-property activities. Brands with owned distribution and high recognition maintain an advantage in trust and standards, but sustained product and service innovation is required to keep pace in the United States luxury hotel market.

Other drivers and restraints analyzed in the detailed report include:

- Direct digital bookings reduce distribution costs

- Mixed-use hotel-residence projects contribute to the stabilization of RevPAR

- Payroll costs surge due to ongoing labor shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Suites captured 42.88% of the United States luxury hotel market share in 2025, while villas and bungalows are projected to expand at a 7.42% CAGR through 2031, reflecting a dual demand pattern for flexible space and high-privacy stays within the United States luxury hotel market. Suites serve corporate travelers who extend trips, multigenerational families, and couples seeking separate living and sleeping areas, which keeps occupancy steadier across weekdays and weekends. These configurations are aligned to work-from-anywhere lifestyles and offer attractive layouts with living rooms and workspaces that elevate both productivity and comfort in the United States luxury hotel market. Villas and bungalows attract ultra-wealthy travelers who prefer standalone residences, private outdoor areas, and dedicated service teams, which reinforces privacy as a premium feature. Operators have upgraded suites and villa categories to integrate wellness spaces, in-room dining potential, and curated amenities that match longer-stay expectations across the United States luxury hotel market.

Branded examples highlight how premium suite categories anchor positioning and rate on property. The Joseph in Nashville showcases a Presidential Suite with expansive square footage, curated art, and high-spec finishes, which illustrates how luxury rooms evolve into multifunctional sanctuaries suited to work and leisure within the United States luxury hotel industry. At Bellagio in Las Vegas, top-tier suites emphasize entertainment-ready living areas, large bathrooms, and premium bar setups that support hosting and special-occasion travel in the United States luxury hotel industry. As operators manage a mix, suites anchor steady revenue while villa-style options expand the guest base among privacy-seeking UHNW travelers. This balance supports rate integrity and length-of-stay gains within the United States luxury hotel market.

The United States Luxury Hotel Market Report is Segmented by Room Type (Standard Luxury Room, Suites, Villas/Bungalows, Penthouses & Presidential Suites), Booking Channel (Direct Booking, Online Travel Agencies, and Other), Service Type (Business Hotels, Airport Hotels, Suite Hotels, Resorts, Other Service Types), and Geography (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Marriott International

- Hilton Worldwide

- Hyatt Hotels Corporation

- Four Seasons Hotels & Resorts

- Accor SA

- InterContinental Hotels Group (IHG)

- Belmond Ltd.

- Mandarin Oriental Hotel Group

- Rosewood Hotel Group

- Auberge Resorts Collection

- Aman Resorts International

- Montage International

- Nobu Hospitality

- The Peninsula Hotels

- Six Senses Hotels Resorts Spas

- Viceroy Hotel Group

- Leading Hotels of the World (LHW)

- Relais & Chateaux

- Omni Hotels & Resorts

- Preferred Hotels & Resorts

- Salamander Hotels & Resorts

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Experiential luxury demand surges, driven by rising wealth among UHNW individuals and millennials

- 4.2.2 Inbound travel to US gateway cities rebounds, supported by eased visa restrictions

- 4.2.3 Corporate "bleisure" policies lead to an uptick in long-stay luxury room bookings

- 4.2.4 Direct digital bookings reduce distribution costs

- 4.2.5 Mixed-use hotel-residence projects contribute to the stabilization of RevPAR

- 4.2.6 LEED-certified assets buoyed by ESG incentives enjoy higher ADR premiums

- 4.3 Market Restraints

- 4.3.1 Ultra-luxury vacation rentals and branded residences intensify competition

- 4.3.2 Payroll costs surge due to ongoing labor shortages

- 4.3.3 Climate-driven weather events push insurance premiums higher

- 4.3.4 Domestic travelers feel rate fatigue, grappling with inflation pressures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Room Type

- 5.1.1 Standard Luxury Room

- 5.1.2 Suites

- 5.1.3 Villas / Bungalows

- 5.1.4 Penthouses & Presidential Suites

- 5.2 By Booking Channel

- 5.2.1 Direct Booking (Brand Website, Call Center)

- 5.2.2 Online Travel Agencies (OTA)

- 5.2.3 Travel Agents / Tour Operators

- 5.2.4 Corporate Contracts

- 5.3 By Service Type

- 5.3.1 Business Hotels

- 5.3.2 Airport Hotels

- 5.3.3 Suite Hotels

- 5.3.4 Resorts

- 5.3.5 Other Service Types

- 5.4 By Geography

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 South

- 5.4.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Marriott International

- 6.4.2 Hilton Worldwide

- 6.4.3 Hyatt Hotels Corporation

- 6.4.4 Four Seasons Hotels & Resorts

- 6.4.5 Accor SA

- 6.4.6 InterContinental Hotels Group (IHG)

- 6.4.7 Belmond Ltd.

- 6.4.8 Mandarin Oriental Hotel Group

- 6.4.9 Rosewood Hotel Group

- 6.4.10 Auberge Resorts Collection

- 6.4.11 Aman Resorts International

- 6.4.12 Montage International

- 6.4.13 Nobu Hospitality

- 6.4.14 The Peninsula Hotels

- 6.4.15 Six Senses Hotels Resorts Spas

- 6.4.16 Viceroy Hotel Group

- 6.4.17 Leading Hotels of the World (LHW)

- 6.4.18 Relais & Chateaux

- 6.4.19 Omni Hotels & Resorts

- 6.4.20 Preferred Hotels & Resorts

- 6.4.21 Salamander Hotels & Resorts

7 Market Opportunities & Future Outlook

- 7.1 Ultra-luxe remote-working retreat packages for C-suite digital nomads

- 7.2 Asset-light conversions of landmark buildings into experiential boutique luxury