PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044259

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044259

Asia-Pacific Epoxy Adhesive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

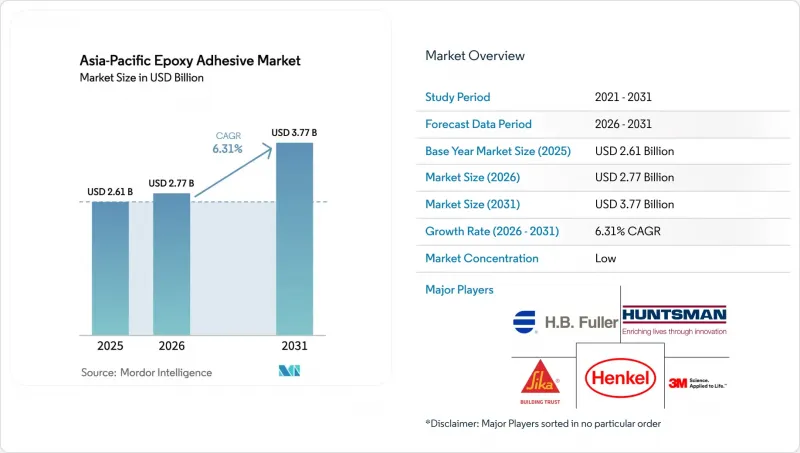

The Asia-Pacific epoxy adhesives market size is expected to grow from USD 2.61 billion in 2025 to USD 2.77 billion in 2026 and is forecast to reach USD 3.77 billion by 2031 at 6.31% CAGR over 2026-2031. Steady electrification of transport, an upturn in semiconductor packaging investments, and record urban infrastructure spending are converging to lift structural bonding demand across the region, allowing the Asia-Pacific epoxy adhesives market to outpace global averages. Two-component reactive systems continue to command pricing power as vehicle makers replace welding with lightweight composite bonding, while stringent indoor-air-quality rules are steering construction projects toward low-VOC hardeners that cure at near-ambient temperatures. Major chemical suppliers are scaling regional laboratories to shorten formulation cycles for electric-vehicle batteries, photonics chiplets, and high-rise facade panels, a shift that tilts competitive advantage toward firms with local application-engineering depth.

Asia-Pacific Epoxy Adhesive Market Trends and Insights

Surging EV And Lightweight Automotive Output

In the Asia-Pacific region, electric vehicle plants are increasingly turning to adhesive solutions for various components, including battery modules, cell-to-pack systems, and aluminum-composite body panels. This trend is bolstering the region's epoxy adhesives market, especially as original-equipment manufacturers aim to reduce curb weight by 15-20%. Major investments from industry giants like BYD, Hyundai, and LG Energy Solution are driving a multi-gigawatt-hour battery capacity. These batteries rely on gap-filling epoxies known for their high thermal conductivity and rapid green strength. Additionally, a newly commercialized silver-paste epoxy, which can be stored at room temperature for up to six months, is revolutionizing the production of silicon-carbide power modules. By eliminating the traditional sintering steps, this innovation not only streamlines inverter production but also reduces energy consumption by as much as 40%.

Rapid Infrastructure And High-Rise Construction

In 2025, governments across the Asia-Pacific region invested over USD 5 trillion in construction. This surge in urbanization heightened the demand for products like facade glazing, anchor grouts, and repair mortars, all of which depend on high-toughness epoxies. Additionally, a newly introduced low-temperature hardener, capable of curing between 5 °C and 10 °C, is revolutionizing winter concreting. This innovation is particularly beneficial for northern China's construction and India's high-altitude rail projects, eliminating the need for expensive heating blankets.

Volatility In Bisphenol A And Epichlorohydrin Feedstocks

Mid-tier mixers, lacking long-term resin contracts, face margin compression due to quarterly price swings exceeding 20%. As a restraint, several processors in Southeast Asia are turning to bio-based epoxies. These epoxies, sourced from rosin and cardanol, boast glass-transition temperatures surpassing 230 °C, albeit at a 30% price premium.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Electronics And Semiconductor Assembly

- Anti-Dumping Tariffs Spurring Backward Integration

- Stringent VOC And Indoor-Air-Quality Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electronics and semiconductor applications are expanding at a rate of 6.58% CAGR. This segment is surpassing the automotive sector as fabs for power devices and photonic modules emerge across regions, including Hsinchu and Kulim. The automotive sector, however, remains the largest contributor, holding a 23.18% share. The Asia-Pacific epoxy adhesives market within this segment continues to grow, driven by applications in vehicle structures, battery packs, and powertrains.

The high-frequency gallium-nitride and silicon-carbide devices segment is fueling demand for silver-filled epoxies with bulk thermal conductivity exceeding 150 W/m-K. This trend is strengthening R&D collaborations between chemical suppliers and substrate manufacturers. Additionally, the construction, energy, and marine segments collectively maintain steady demand. Government investments in infrastructure are focusing on projects such as bridges, wind blades, and hull refurbishments, all of which require high-modulus bonding.

The Asia-Pacific Epoxy Adhesives Market Report is Segmented by End-User Industry (Aerospace and Defense, Automotive, Electrical and Electronics, Construction, Other End-User Industries), Technology (Reactive, Solvent-Borne, UV-Cured, Water-Borne), and Geography (Australia, China, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Thailand, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Dow Inc.

- Dymax Corporation

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co., Ltd.

- Huntsman Corporation

- ITW Performance Polymers

- Jowat SE

- Kangda New Materials (Group) Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV and lightweight automotive manufacturing

- 4.2.2 Rapid infrastructure and high-rise construction spending

- 4.2.3 Expansion of electronics and semiconductor assembly

- 4.2.4 Domestic aircraft programs adopt localized qualifications

- 4.2.5 Anti-dumping tariffs spurring backward integration

- 4.3 Market Restraints

- 4.3.1 Volatile BPA and ECH feedstock prices

- 4.3.2 Stringent VOC and IAQ regulations on solvent systems

- 4.3.3 Performance gap and cost premium of water-borne epoxies

- 4.4 Value Chain Analysis

- 4.5 Distribution Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Distribution Channel Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Aerospace and Defense

- 5.1.2 Automotive

- 5.1.3 Marine

- 5.1.4 Electrical and Electronics

- 5.1.5 Construction

- 5.1.6 Energy and Power

- 5.1.7 Other End-User Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-Cured

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 artience Co., Ltd.

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 Dow Inc.

- 6.4.7 Dymax Corporation

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hubei Huitian New Materials Co., Ltd.

- 6.4.11 Huntsman Corporation

- 6.4.12 ITW Performance Polymers

- 6.4.13 Jowat SE

- 6.4.14 Kangda New Materials (Group) Co., Ltd.

- 6.4.15 NANPAO RESINS CHEMICAL GROUP

- 6.4.16 Permabond LLC

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment