PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044267

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044267

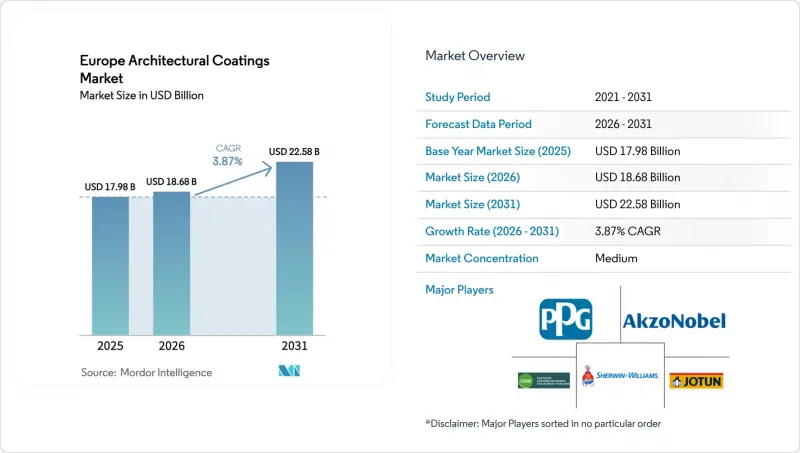

Europe Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Architectural Coatings Market size is projected to grow from USD 17.98 billion in 2025 to USD 18.68 billion in 2026, and reach USD 22.58 billion by 2031, growing at a CAGR of 3.87% from 2026 to 2031.

A measured pivot toward high-value, low-emission formulations has started to outweigh pure volume growth, as purchasers respond to tougher European Union VOC ceilings and a building stock whose average age now tops 50 years. Demand for waterborne systems already dominates because professional painters favor low-odor, easy-clean products, and retailers have delisted many solventborne lines to avoid compliance risk. Suppliers are also repositioning toward repair and refurbishment projects that promise steadier margins than new-build work, weakened by high borrowing costs. Consolidation among leading producers is accelerating in order to spread raw-material inflation, fund greener research and development pipelines, and strengthen go-to-market scale.

Europe Architectural Coatings Market Trends and Insights

Aging Housing-Stock Renovation Boom

Europe counts more than 220 million dwellings built before 1990; many now require facade repair, moisture protection, and interior upgrades to meet modern health standards. Eurostat recorded EUR 310 billion spent on housing renovation in 2025, up 12% from the prior year. France, Germany, Italy, and Spain delivered 60% of that spending, with Italy alone surging 20% thanks to generous tax credits for energy-efficient coatings. The European Parliament wants to double annual renovation rates to 2% by 2030, lifting demand for durable acrylic and polyurethane finishes that extend repaint cycles from seven to twelve years. Consequently, the Europe architectural coatings market continues to rotate toward high-margin segments while sustaining steady headline growth.

EU VOC Regulations Accelerating Waterborne Shift

The European Commission updated EU Ecolabel rules in February 2026, lowering both VOC and SVOC caps and adding fitness-for-use tests that discourage binder dilution. Retailers quickly delisted non-compliant solventborne lines; by end-2025 waterborne products already formed 70% of decorative volume, up five points in five years. Pure acrylic emulsions now dominate interior walls, while styrene-acrylic blends migrate to budget exteriors. BASF, AkzoNobel, and Arkema validated bio-attributed resins that cut coating carbon footprints 40% during 2025 pilot runs. These moves confirm that tighter regulation not only accelerates waterborne uptake but also raises entry barriers for smaller formulators lacking research and development scale. As a result, the Europe architectural coatings market is tilting toward larger incumbents with science-based sustainability credentials.

Titanium-Dioxide and Petro-Feedstock Price Volatility

Spot TiO2 hovered between EUR 2,800 and EUR 3,400 per ton in 2025, a 21% swing that squeezed gross margins for mass-market interior emulsions. Producers offset part of the spike with extender pigments and composite opacifiers, yet these substitutions risk reduced scrub resistance or color fidelity at higher tint levels. Simultaneously, acrylic-monomer costs tracked Brent crude, which ranged from USD 75 to USD 95 per barrel. Because EU duties keep cheap Chinese TiO2 out of the bloc, local formulators face a persistently high cost floor relative to Asian rivals.

Other drivers and restraints analyzed in the detailed report include:

- Post-COVID Rebound in Commercial Fit-Outs

- Demand for Energy-Saving Thermal-Insulation Paints

- High Interest Rates Dampening New-Build Housing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential projects generated 68.96% of 2025 revenue and will climb at a 4.04% CAGR through 2031. Renovation dominates because owners must preserve asset value in an aging building stock, and national tax credits now reimburse up to 30% of energy-saving exterior paint costs. Italy led spending with a 20% uptick in 2025 after enhancing its Eco-Bonus scheme. Consumers increasingly specify low-odor paints carrying asthma-allergy labels, and anti-scuff interior emulsions advertised to last a decade between coats. That dynamic lifts average selling prices even as liters per dwelling shrink.

Commercial applications are also witnessing increasing demand for architectural coatings. Offices are adapting to hybrid work, which trims square footage requirements by roughly 15%. Yet hotel, healthcare, and education refurbishments have accelerated, each demanding fast-dry zero-VOC or antimicrobial coatings to minimize disruption. The segment relies on supply partners able to stage rapid weekend repaints, a service advantage mid-tier regional brands exploit. Nonetheless, volume recovery remains uneven across Europe; Spain posts double-digit hospitality gains, whereas Germany's office pipeline stalls under financing constraints.

The Europe Architectural Coatings Market Report is Segmented by End-User Industry (Commercial and Residential), Technology (Solventborne and Waterborne), Resin (Acrylic, Alkyd, Epoxy, Polyester, Polyurethane, and Other Resin Types), and Geography (France, Germany, Italy, Nordic Countries, Poland, Russia, Spain, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AkzoNobel N.V.

- Benjamin Moore & Co.

- Brillux GmbH & Co. KG

- CIN S.A.

- DAW SE

- Flugger group A/S

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- KOBER SRL

- Nippon Paint Holdings Co., Ltd.

- POLICOLOR SA

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Sniezka SA

- Sto SE & Co. KGaA

- Teknos Group

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing housing-stock renovation boom

- 4.2.2 EU VOC regulations accelerating waterborne shift

- 4.2.3 Post-COVID rebound in commercial fit-outs

- 4.2.4 Demand for energy-saving thermal-insulation paints

- 4.2.5 On-site tint-as-a-service platforms

- 4.3 Market Restraints

- 4.3.1 Titanium-dioxide and petro-feedstock price volatility

- 4.3.2 High interest rates dampening new-build housing

- 4.3.3 Professional painter labour shortages

- 4.4 Value Chain Analysis

- 4.5 Regulatory Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Commercial

- 5.1.2 Residential

- 5.2 By Technology

- 5.2.1 Solventborne

- 5.2.2 Waterborne

- 5.3 By Resin

- 5.3.1 Acrylic

- 5.3.2 Alkyd

- 5.3.3 Epoxy

- 5.3.4 Polyester

- 5.3.5 Polyurethane

- 5.3.6 Other Resin Types

- 5.4 By Geography

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Nordic Countries

- 5.4.5 Poland

- 5.4.6 Russia

- 5.4.7 Spain

- 5.4.8 United Kingdom

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Benjamin Moore & Co.

- 6.4.3 Brillux GmbH & Co. KG

- 6.4.4 CIN S.A.

- 6.4.5 DAW SE

- 6.4.6 Flugger group A/S

- 6.4.7 Hempel A/S

- 6.4.8 Jotun

- 6.4.9 Kansai Paint Co., Ltd.

- 6.4.10 KOBER SRL

- 6.4.11 Nippon Paint Holdings Co., Ltd.

- 6.4.12 POLICOLOR SA

- 6.4.13 PPG Industries, Inc.

- 6.4.14 The Sherwin-Williams Company

- 6.4.15 Sniezka SA

- 6.4.16 Sto SE & Co. KGaA

- 6.4.17 Teknos Group

- 6.4.18 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment