PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044280

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044280

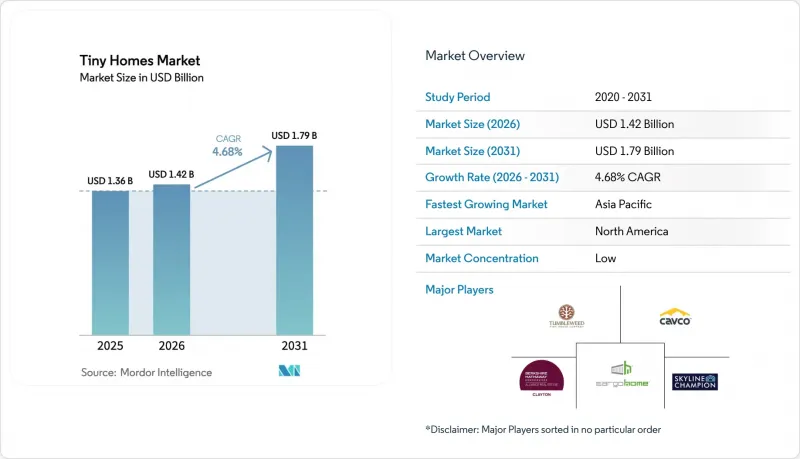

Tiny Homes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Tiny Homes Market size is expected to increase from USD 1.36 billion in 2025 to USD 1.42 billion in 2026 and reach USD 1.79 billion by 2031, growing at a CAGR of 4.68% over 2026-2031.

Deepening housing-affordability gaps, median prices topped eight times median household income across major Organisation for Economic Co-operation and Development (OECD) cities in 2025, are steering first-time buyers and retirees toward sub-400-square-foot dwellings that bypass conventional mortgage underwriting. Concurrently, remote work stabilized at 28% of U.S. full-time employees in 2025, untethering location decisions from offices and enabling buyers to site units on lower-cost rural parcels. Corporate fleet procurement, especially from renewable-energy developers and mining firms, adds a volume channel previously absent from single-family residential sales. Timber remains the dominant build material, yet steel-framed designs are gaining traction, while hospitality deployments are emerging as the fastest-growing application. Overall, the tiny homes market is transitioning from a lifestyle niche to an affordability-driven housing substitute, supported by sustainability mandates and flexible work patterns.

Global Tiny Homes Market Trends and Insights

Rising Housing Unaffordability Drives Demand for Cost-Effective Downsizing Solutions

Median purchase prices reached 8.2 times median household income across OECD economies in 2025, an unprecedented affordability gap that is pushing buyers toward USD 40,000-USD 80,000 turnkey tiny homes. Forty percent of U.S. adults under 35 could not cover an unexpected USD 400 expense in 2025, underscoring sensitivity to monthly housing payments. In coastal metros where land routinely exceeds USD 500 per square foot, sub-400-square-foot dwellings present one of the few ownership paths for median earners. Downsizers aged 55 and older, motivated by rising property taxes and the desire to monetize home equity, add a second major demand cohort, with 34% of U.S. baby boomers considering downsizing last year. The affordability wedge is no longer cyclical; it is reshaping the buyer profile, shifting tiny homes from an aspirational lifestyle option to a practical housing solution.

Growing Sustainability and Net-Zero Housing Initiatives Accelerate Tiny Home Adoption

Twelve European Union member states mandated near-zero-energy performance for new homes by 2025, creating a regulatory tailwind for compact dwellings that naturally require less heating and cooling. International Energy Agency (IEA) studies show that sub-500-square-foot units consume 45% less annual energy than conventional houses. Timber-framed construction sequesters close to 1 metric ton of carbon dioxide per cubic meter of wood, aligning tiny homes with national decarbonization targets. California's 2025 energy code extended rooftop-solar mandates to accessory units under 800 square feet, spurring manufacturers to bundle photovoltaic packages. Hospitality chains are also adopting tiny clusters to meet Leadership in Energy and Environmental Design (LEED) criteria, signaling that sustainability is now a structural growth driver rather than a marketing add-on.

Fragmented Zoning Regulations and Building Codes Restrict Legal Placement of Tiny Homes

Local ordinances categorize tiny dwellings variously as recreational vehicles, accessory dwelling units, or manufactured housing, creating legal gray zones that complicate resale and financing. Fewer than 30% of U.S. counties explicitly addressed tiny homes in 2025 zoning codes, forcing variance applications or limiting placement to rural plots. Europe faces similar fragmentation; Germany's state-level Bauordnung often requires permanent foundations that negate mobility benefits. Insurance carriers respond by classifying units as RVs, raising premiums. Until harmonized frameworks akin to California's 2024 ADU reforms proliferate, regulatory friction will cap adoption and dampen investor confidence.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Remote Work Enables Geographic Mobility and Supports Tiny Home Living

- Increasing Urban Land Scarcity in Megacities Encourages Compact Housing Alternatives

- Limited Mortgage Options and Financing Avenues Hinder Large-Scale Consumer Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stationary/fixed tiny homes held 54.10% of the tiny homes market share in 2025, reflecting consumer preference for code-compliant foundations and easier utility hookups. Fixed installations appeal to buyers seeking long-term asset appreciation, yet they require land purchase or long leases, which limit flexibility. Mobile tiny homes, forecast to grow at a 5.45% CAGR through 2031, ride the wave of workforce mobility and seasonal hospitality demand, offering relocatability without sacrificing quality. Construction-sector data show that 12% of U.S. wind- and solar-project laborers used temporary on-site housing in 2025, a niche where mobile tiny homes compete effectively against standard trailers.

Hybrid designs are emerging units built on steel chassis that satisfy International Residential Code (IRC) Appendix Q once sited, allowing owners to retain mobility while meeting strict local codes. Hospitality operators favor mobile clusters that can be redeployed across resorts as seasonal demand shifts, minimizing stranded assets. For manufacturers, the faster-growing mobile segment diversifies revenue and extends addressable markets into events, disaster response, and corporate fleet housing, positioning it as a key growth pillar.

The Tiny Homes Market Report is Segmented by Product Type (Mobile Tiny Homes, Stationary/Fixed Tiny Homes), by Material (Timber, Metal, Concrete and Others), by Application (Residential Households, Hospitality and Others), and by Geography (North America, South America, Europe, Middle East and Africa, and Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America supplied 42.93% of global revenue in 2025 as elevated house prices, high remote-work incidence, and progressive state regulations converged. Approximately 15,000 units were shipped in the United States that year, with sales balanced between affordability seekers and hospitality operators expanding glamping capacity. Canadian growth derives from younger households relocating to smaller municipalities, spurred by provincial pilots relaxing minimum-size rules. Mexico's coastal tourism sector is experimenting with tiny-home clusters as eco-friendly alternatives to concrete villas. Structural challenges remain chiefly fragmented zoning and scarce mortgage products, but model ordinances under review by the American Planning Association could catalyze a post-2027 acceleration.

Asia-Pacific is the fastest-growing region, poised for a 6.41% CAGR through 2031 thanks to urban land scarcity, supportive pilots, and a rising middle class. Japan's MLIT micro-housing program in Tokyo and Osaka legalized sub-200-square-foot units, while Australia's state-level code changes removed parking and lot-coverage hurdles for secondary dwellings. South Korea and China are exploring modular housing for retirees and migrant workers, though national standards lag. India and Indonesia offer longer-run potential once informal-housing norms yield to formal prefabrication. The tiny homes market size in Asia-Pacific could challenge North America's lead if regulatory timelines stay on track.

Europe remains smaller but strategically vital because net-zero codes elevate the value of compact formats. Germany, France, and the United Kingdom head demand, leveraging state-level Bauordnung reforms and planning-code adjustments that welcome sub-50-square-meter dwellings on existing lots. Scandinavia records high per-capita uptake on environmental grounds, whereas Southern Europe adopts slowly except in agritourism hubs. Although slower population growth tempers upside, carbon-reduction mandates and energy-price volatility offer a durable pull. Beyond the core regions, Latin America and the Middle East & Africa are at an exploratory stage, with isolated projects in Brazilian eco-tourism and Gulf infrastructure camps.

- Tumbleweed Tiny House Company

- Skyline Champion Corporation

- Cavco Industries Inc.

- Berkshire Hathaway (Clayton Homes)

- CargoHome

- Tiny SMART House Inc.

- Aussie Tiny Houses

- Mustard Seed Tiny Homes LLC

- Mini Mansions Tiny Home Builders LLC

- Nestron

- American Tiny House

- California Tiny House Inc.

- Incredible Tiny Homes

- Container Homes USA

- Wheelhaus

- ESCAPE Homes

- Tiny Mountain Houses

- New Frontier Tiny Homes

- Viva Collectiv

- TruForm Tiny

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising housing unaffordability drives demand for cost-effective downsizing solutions

- 4.2.2 Growing sustainability and net-zero housing initiatives accelerate tiny home adoption

- 4.2.3 Expansion of remote work enables geographic mobility and supports tiny home living

- 4.2.4 Increasing urban land scarcity in megacities encourages compact housing alternatives

- 4.2.5 Corporate fleet adoption for temporary workforce site housing boosts tiny home demand

- 4.2.6 Inter-generational granny-pod installations rise with ageing populations and family care needs

- 4.3 Market Restraints

- 4.3.1 Fragmented zoning regulations and building codes restrict legal placement of tiny homes

- 4.3.2 Limited mortgage options and financing avenues hinder large-scale consumer adoption

- 4.3.3 Perceived lack of space and privacy discourages potential homeowners from downsizing

- 4.3.4 Weak secondary resale market reduces long-term investment attractiveness for buyers

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Pricing & Cost-Structure Analysis

- 4.7 Consumer Demographics & Psychographics

- 4.8 Tiny-Home Community & Village Development

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Mobile Tiny Homes

- 5.1.2 Stationary/Fixed Tiny Homes

- 5.2 By Material

- 5.2.1 Timber

- 5.2.2 Metal

- 5.2.3 Concrete

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Residential Households

- 5.3.2 Hospitality

- 5.3.3 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Sweden

- 5.4.3.7 Rest of Europe

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 Indonesia

- 5.4.5.7 Rest of Asia-Pacific

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Tumbleweed Tiny House Company

- 6.3.2 Skyline Champion Corporation

- 6.3.3 Cavco Industries Inc.

- 6.3.4 Berkshire Hathaway (Clayton Homes)

- 6.3.5 CargoHome

- 6.3.6 Tiny SMART House Inc.

- 6.3.7 Aussie Tiny Houses

- 6.3.8 Mustard Seed Tiny Homes LLC

- 6.3.9 Mini Mansions Tiny Home Builders LLC

- 6.3.10 Nestron

- 6.3.11 American Tiny House

- 6.3.12 California Tiny House Inc.

- 6.3.13 Incredible Tiny Homes

- 6.3.14 Container Homes USA

- 6.3.15 Wheelhaus

- 6.3.16 ESCAPE Homes

- 6.3.17 Tiny Mountain Houses

- 6.3.18 New Frontier Tiny Homes

- 6.3.19 Viva Collectiv

- 6.3.20 TruForm Tiny

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment