PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044284

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044284

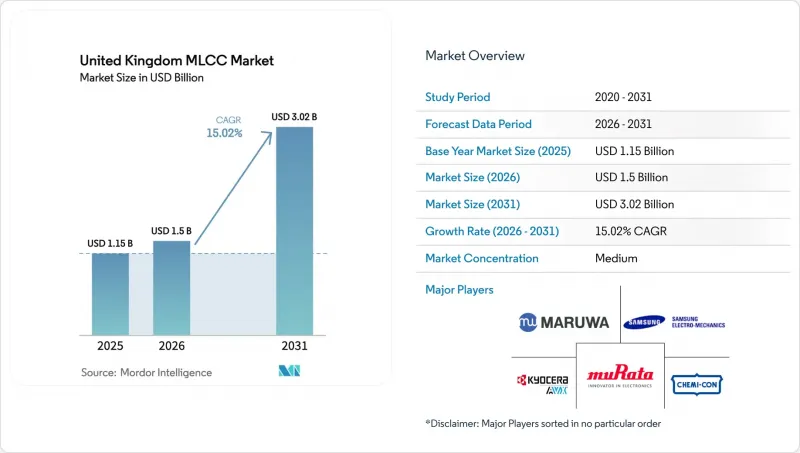

United Kingdom MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United Kingdom MLCC market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.50 billion in 2026 to reach USD 3.02 billion by 2031, at a CAGR of 15.02% during the forecast period (2026-2031).

Solid policy support for zero-emission vehicles, favorable capital-allowance rules inside Freeport zones, and defense-electronics localisation under AUKUS together energize local demand. Tight global capacity, however, continues to lift average selling prices, nudging buyers toward dual-sourcing and buffer-stock strategies. Local distributors are responding by expanding bonded inventory close to automotive and medical hubs to limit allocation risk. At the same time, the pivot to 800-volt vehicle platforms, miniaturised medical implants, and high-frequency 5G radios is tilting the product mix toward high-voltage, ultra-stable, and ultra-small capacitors.

United Kingdom MLCC Market Trends and Insights

Surge in EV Manufacturing Ahead of the 2030 UK ICE Ban

United Kingdom vehicle makers are scaling up electric-vehicle output to meet the 2030 ban on internal-combustion engines, lifting per-car capacitor content roughly threefold. Gigafactory investments by Tata in Somerset and AESC in Sunderland anchor local battery and power-electronics ecosystems, pulling qualification work into the United Kingdom MLCC market. The GBP 2.5 billion DRIVE35 program earmarks USD 2.6 billion for capital expenditure on power-electronics supply chains, signaling continued policy pull. Each electric vehicle contains about 10,000 capacitors, and design migration to 800-volt architectures further raises voltage-rating requirements. Local distributors now maintain bonded stock near West Midlands OEM sites to avoid Asian allocation shocks. These moves jointly amplify the growth outlook of the United Kingdom MLCC market.

Accelerated 5G Roll-Out Boosting Small-Cell Demand

Telecom operators are densifying 5G networks with thousands of small-cell base stations, each loaded with dozens of 0201 and 0402 capacitors for high-frequency bypass functions. Ofcom's Connected Nations data confirms rapid urban coverage expansion in London, Manchester, and Birmingham. Murata's capacitor revenue rose 9% year on year in the first half of fiscal 2025, driven partly by telecommunications orders. As power density climbs, designers prefer X7R and X5R dielectrics with stable capacitance under bias, and they favor suppliers with advanced material know-how. This telecom build-out therefore feeds an incremental tailwind into the United Kingdom MLCC market.

Persistent MLCC Supply-Demand Imbalance Inflating Lead-Times

Artificial-intelligence server demand has pushed Murata's global utilisation towards 95%, draining buffer inventory. Allocation risk forces UK buyers to accept longer contract horizons or pay premiums on the spot market. Automotive and defense programs that need traceable lots face the greatest exposure. Some tier-1s now dual-source with polymer hybrids or film capacitors, but re-qualification costs remain high, tempering substitution.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Compact Medical Wearables and Implantables

- Government Tax Incentives for On-Shore Passive-Component Production

- Nickel and Copper Price Volatility Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class 2 compositions held 45.72% of the United Kingdom MLCC market share in 2025, anchored by high-capacitance X7R and X5R grades. Their dominance comes from volumetric efficiency that suits decoupling and energy-storage tasks across consumer and industrial boards. However, Class 1 C0G and NP0 parts are projected to expand at a 15.42% CAGR through 2031 as automotive inverters, radar modules, and implantables prioritize near-zero aging and tight tolerance. The United Kingdom MLCC market for precision timing and sensing circuits is therefore tilting toward Class 1 technology.

Suppliers are widening high-voltage Class 1 offerings, such as TDK's 10 nF, 1,250 V C0G in 3225 format. Automotive engineers value stable capacitance under bias for battery-management accuracy, while medical device makers need temperature-invariant behavior over decades. These attributes let Class 1 parts capture design wins even where their cost per microfarad is higher, reinforcing their forecast outperformance in the United Kingdom MLCC market.

The 402 size accounted for 37.29% of the United Kingdom MLCC market share in 2025, reflecting its balance of pick-and-place yield and capacitance headroom. Yet board-area scarcity in 5G radios and glucose patches is driving a 15.83% CAGR for the 201 format. Designers can now achieve the same capacitance in fewer footprints due to breakthroughs such as TDK's 1608 case capacitors with tenfold capacitance gains at 100 V.

As more logic shifts to chiplet packages, the passive placement area shrinks further, raising demand for smaller formats. The United Kingdom MLCC market size allocated to 201 and even 01005 footprints will likely rise fastest in medical wearables and telecom small cells. In contrast, power-electronics boards in vehicles still rely on 1210 or larger parts for ripple-current handling. This dual-track demand keeps a broad case-size portfolio essential for suppliers.

The United Kingdom MLCC Market Report is Segmented by Dielectric Type (Class 1 and Class 2), Case Size (201, 402, 603, 1005, 1210, and Other Case Sizes), Voltage (Low Voltage, Mid Voltage, and High Voltage), MLCC Mounting Type (Metal Cap, Radial Lead, and Surface Mount), End-User Application (Aerospace and Defence, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kyocera AVX Components Corporation

- MARUWA Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Samwha Capacitor Co., Ltd.

- TAIYO YUDEN Co., Ltd.

- TDK Corporation

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Worth Elektronik GmbH and Co. KG

- Yageo Corporation

- Panasonic Industry Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- KEMET Corporation

- Darfon Electronics Corp.

- Shenzhen Sunlord Electronics Co., Ltd.

- Exxelia Group

- Knowles Precision Devices

- NIC Components Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV Manufacturing Ahead of 2030 UK ICE-Ban

- 4.2.2 Accelerated 5G Infrastructure Roll-Out Boosting Small-Cell Demand

- 4.2.3 Rising Demand for Compact Medical Wearables and Implantables

- 4.2.4 Government Tax Incentives for On-Shore Passive Component Production

- 4.2.5 Battery Management-System Design Shifts to Higher Capacitance

- 4.2.6 Defence Electronics Localisation under AUKUS and UK MoD Initiatives

- 4.3 Market Restraints

- 4.3.1 Persistent MLCC Supply-Demand Imbalance Inflating Lead-Times

- 4.3.2 Nickel and Copper Price Volatility Squeezing Margins

- 4.3.3 Regulatory Hurdles for New Fab Construction (Planning and ESG)

- 4.3.4 Growing Substitution by Embedded Capacitors in HDI PCBs

- 4.4 Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Dielectric type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 By Case Size

- 5.2.1 0201

- 5.2.2 0402

- 5.2.3 0603

- 5.2.4 1005

- 5.2.5 1210

- 5.2.6 Other Case Sizes

- 5.3 By Voltage

- 5.3.1 Low Voltage (Less Than or Equal to 100 V)

- 5.3.2 Mid Voltage (100-500 V)

- 5.3.3 High Voltage (Greater Than500 V)

- 5.4 By MLCC Mounting Type

- 5.4.1 Metal Cap

- 5.4.2 Radial Lead

- 5.4.3 Surface Mount

- 5.5 By End-User Application

- 5.5.1 Aerospace and Defense

- 5.5.2 Automotive

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Medical Devices

- 5.5.6 Power and Utilities

- 5.5.7 Telecommunication

- 5.5.8 Other End-User Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kyocera AVX Components Corporation

- 6.4.2 MARUWA Co., Ltd.

- 6.4.3 Murata Manufacturing Co., Ltd.

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics Co., Ltd.

- 6.4.6 Samwha Capacitor Co., Ltd.

- 6.4.7 TAIYO YUDEN Co., Ltd.

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology, Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Worth Elektronik GmbH and Co. KG

- 6.4.12 Yageo Corporation

- 6.4.13 Panasonic Industry Co., Ltd.

- 6.4.14 Holy Stone Enterprise Co., Ltd.

- 6.4.15 KEMET Corporation

- 6.4.16 Darfon Electronics Corp.

- 6.4.17 Shenzhen Sunlord Electronics Co., Ltd.

- 6.4.18 Exxelia Group

- 6.4.19 Knowles Precision Devices

- 6.4.20 NIC Components Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment