PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2060415

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2060415

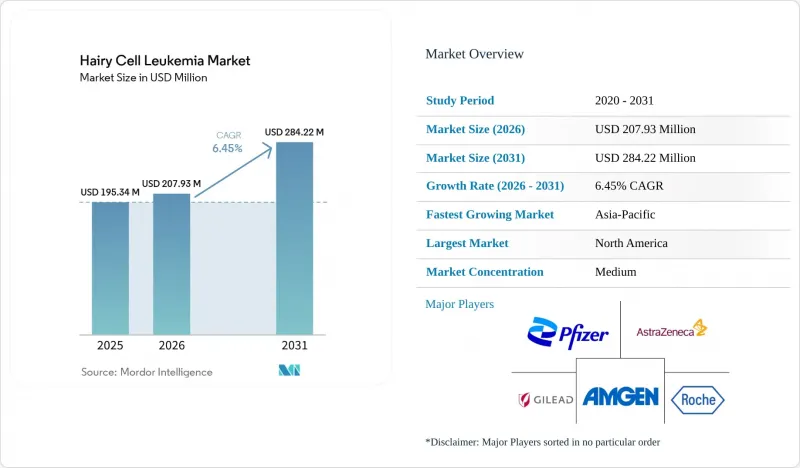

Hairy Cell Leukemia - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hairy cell leukemia market size was valued at USD 195.34 million in 2025 and is estimated to grow from USD 207.93 million in 2026 to reach USD 284.22 million by 2031, at a CAGR of 6.45% during the forecast period (2026-2031).

This report is Segmented by Product Type (Diagnostic and Therapy Type), Route of Administration (Oral, Intravenous, Subcutaneous), Treatment Setting (First-Line, Relapsed/Refractory), End User (Hospitals, Specialty Cancer Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Hairy Cell Leukemia Market Trends and Insights

MRD-Guided Retreatment Gains Traction

Bone-marrow MRD assays, capable of detecting BRAF V600E allele frequencies below 0.01%, are increasingly influencing the timing of salvage treatments. This advancement is reducing infection-related complications and lowering costs for pancytopenic patients. The adoption of Memorial Sloan Kettering's Phase 2 protocol, which requires MRD assessment at six months, has accelerated this trend. Early intervention with targeted therapies is minimizing hospitalizations. However, the absence of standardized MRD cut-offs presents challenges in aligning with payer requirements. Draft guidance expected in late 2025 may help standardize endpoints, but reimbursement will remain contingent on national health-technology assessments.

Companion Diagnostics for BRAF V600E Mutation Take Center Stage

With over 95% of classic cases linked to the BRAF V600E mutation, confirming this alteration is essential before prescribing vemurafenib. The industry is shifting toward multiplex, clinic-ready testing, as demonstrated by recent partnerships to develop high-throughput flow assays. Regulatory changes, such as the reclassification of these diagnostics from Class III to Class II, are expected to shorten pre-market timelines. However, stricter analytical validation requirements are likely to increase development costs. In Europe, delays in IVDR enforcement until 2029 are creating a two-speed market, where U.S. laboratories are advancing MRD platforms while many European facilities await regulatory-compliant kits.

Small Patient Pool Limits Trial Economics

With a global prevalence of only 15,000 to 20,000 cases, even 80-patient Phase 2 studies require three years for enrollment. Per-patient costs exceed USD 45,000, double that of standard oncology trials, due to multi-center activation fees and centralized MRD testing. While regulators permit single-arm designs, European payers often reject data without randomized comparators, delaying market access timelines.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Male Demographic Sees Rising Incidence

- Outpatient IV Push Formulations on the Rise

- High Relapse Rates With Purine-Analog Re-Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, therapy-type products accounted for 62.34% of the revenue, highlighting the Hairy cell leukemia market's reliance on cladribine, pentostatin, rituximab, and emerging BRAF-inhibitor regimens. As MRD testing becomes standard, diagnostics are growing at a 7.79% CAGR, evolving from four-color flow panels to high-parameter spectral cytometry with a 0.01% sensitivity threshold. While the market for advanced diagnostics in Hairy cell leukemia is expanding more rapidly than drug revenue, it is starting from a smaller base.

Spectral instruments, combined with next-generation sequencing, allow for allele-specific PCR confirmation of BRAF V600E at a 0.001% variant-allele frequency, enabling clinicians to time salvage therapy accurately. However, the adoption of this workflow is inconsistent; by 2025, only 11 out of 28 EU countries reimbursed molecular tests. Yet, centralized reference labs are growing to bridge this gap. With unified MRD guidance on the horizon, diagnostics are poised to play a significant role in shaping the future market share of Hairy cell leukemia.

In 2025, intravenous delivery accounted for 51.43% of spending, supported by established cladribine and rituximab protocols prevalent in community practice. However, oral vemurafenib is projected to expand at a 7.96% CAGR, gradually increasing the oral segment's share in the Hairy cell leukemia market. A two-hour IV push of cladribine reduces neutropenia risk compared to a five-day continuous infusion, also optimizing infusion chair usage for more profitable biologics, thus accelerating IV process innovation in the U.S.

While European adoption lags due to reimbursement codes favoring longer infusions, there is growing pressure to reduce inpatient stays. Subcutaneous rituximab, making up 8% of administration routes in 2025, could see an uptick as hospitals aim for better chair-time efficiency. Although oral therapies are challenging the IV's dominance, the ongoing need for combination rituximab infusions ensures IV's stronghold for the foreseeable future.

Geography Analysis

In 2025, North America accounted for 39.34% of the revenue, driven by Medicare's reimbursement for cladribine, rituximab, and the NCCN-listed off-label vemurafenib. These factors collectively support the Hairy Cell Leukemia market in the region. The U.S. benefits from a strong presence of academic institutions and the 2025 FDA orphan-drug fee waiver, which provides significant support to smaller sponsors. Meanwhile, Canada lags 12-18 months behind the U.S. due to Health Canada's requirement for explicit indications. Additionally, provincial formularies restrict access until cost-effectiveness reviews are completed.

Europe's 32% market share reflects regional disparities. Germany, with its 180-day automatic orphan-drug reimbursement rule, secures 28% of the region's sales. In contrast, Central and Eastern Europe face delays exceeding 24 months for national approvals. While the 2025 EU Joint Clinical Assessment aims to standardize evidentiary benchmarks, the negotiation of price-volume agreements remains under state jurisdiction. Although the Hairy Cell Leukemia market demonstrates stable potential, delayed MRD reimbursements in Poland and Bulgaria could hinder short-term growth.

Asia-Pacific, with an 8.25% CAGR, is fueled by South Korea's hematology reimbursement expansion in March 2026 and China's 2025 NRDL update, which signals a favorable stance towards targeted therapies. Japan's established orphan-drug framework facilitates quicker access. However, smaller ASEAN countries, lacking specialized hematopathology infrastructure, dampen the region's overall averages. Despite this, ongoing modernization among payers indicates a consistent growth trajectory for the Hairy Cell Leukemia market through 2031.

- Abbvie

- Adaptive Biotechnologies Corp.

- ADC Therapeutics

- Amgen

- AstraZeneca

- BeiGene

- Bristol-Myers Squibb

- Roche

- Genmab

- Gilead Sciences

- Innate Pharma SA

- Johnson & Johnson

- Merck

- Merck

- Novartis

- Pfizer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Leukemia Cases & Higher Diagnosis Rates

- 4.2.2 Rising Geriatric Population

- 4.2.3 Rapid Uptake of Next-Generation Targeted Therapies

- 4.2.4 MRD-Guided Retreatment Algorithms

- 4.2.5 Home-Based Sub-Cutaneous Cladribine Protocols

- 4.2.6 Support of Regulatory Authorities

- 4.3 Market Restraints

- 4.3.1 Limited Awareness & Specialist Access in Rural Areas

- 4.3.2 High Cost of Novel Targeted Agents

- 4.3.3 Orphan-Drug Exclusivity Expiries Post-2028

- 4.3.4 Severe Immunosuppression & Infection Risk with Purine Analogues

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Therapy Type

- 5.1.1 Chemotherapy (purine analogues)

- 5.1.2 Targeted Therapy (BRAF, BTK, MEK inhibitors)

- 5.1.3 Immunotherapy (mAbs, immunotoxins)

- 5.1.4 Others (interferon-a, splenectomy)

- 5.2 By Patient Type

- 5.2.1 Classic HCL (cHCL)

- 5.2.2 Variant HCL (HCL-V)

- 5.2.3 SDRPL & other HCL-like disorders

- 5.3 By Route of Administration

- 5.3.1 Intravenous Infusion

- 5.3.2 Sub-cutaneous Injection

- 5.3.3 Oral

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Adaptive Biotechnologies Corp.

- 6.3.3 ADC Therapeutics SA

- 6.3.4 Amgen Inc.

- 6.3.5 AstraZeneca plc

- 6.3.6 BeiGene Ltd

- 6.3.7 Bristol-Myers Squibb Co.

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 Genmab A/S

- 6.3.10 Gilead Sciences Inc.

- 6.3.11 Innate Pharma SA

- 6.3.12 Johnson & Johnson (Janssen)

- 6.3.13 Merck & Co., Inc.

- 6.3.14 Merck KGaA

- 6.3.15 Novartis AG

- 6.3.16 Pfizer Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment