PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063730

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063730

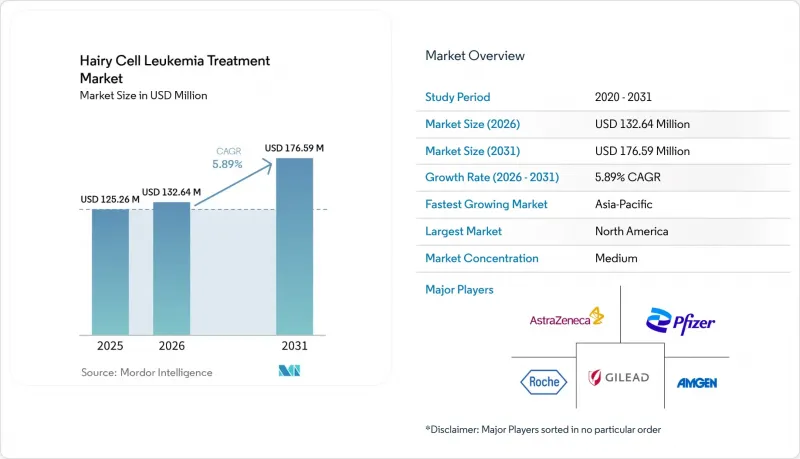

Hairy Cell Leukemia Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hairy cell leukemia treatment market size is expected to increase from USD 125.26 million in 2025 to USD 132.64 million in 2026 and reach USD 176.59 million by 2031, growing at a CAGR of 5.89% over 2026-2031.

This report is Segmented by Therapy Type (Chemotherapy, Targeted Therapy, Immunotherapy, and Others), Patient Type (Classic HCL, Variant HCL, and More), Route of Administration (Intravenous Infusion, Subcutaneous Injection, and Oral), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Hairy Cell Leukemia Treatment Market Trends and Insights

Growing Burden of Leukemia Cases & Higher Diagnosis Rates

Flow cytometry and immunophenotyping now uncover cases that previously slipped under clinical radar, raising confirmed incidence counts and enabling prompt therapeutic intervention. AI-enabled pattern recognition archives a 97.5% concordance with manual reads while trimming processing time by 60.3%, increasing throughput and standardizing quality. Telemedicine links provincial laboratories with metropolitan reference centers, accelerating second opinions for atypical findings. Refinement of morphological scoring has also clarified epidemiology; the near-universal BRAF V600E hallmark provides a single-gene anchor that removes diagnostic ambiguity. These advances collectively swell treatment-eligible populations and shorten lead times to first treatment.

Rising Geriatric Population

Median presentation age remains between 50 and 55 years, yet prevalence rises sharply in octogenarian cohorts. Bone marrow biopsy audits in individuals aged 85 plus revised initial diagnoses in 44.1% and reshaped therapy plans in 25.4% without added complications. Older patients push demand for regimens that offer deep responses without myelosuppressive intensity, tilting prescribing toward BRAF or BTK inhibition. Subcutaneous dosing schedules reduce hospital stays, align with mobility constraints, and thus resonate with senior lifestyle preferences. Prolonged post-remission survival further necessitates structured surveillance and retreatment triggers.

Limited Awareness & Specialist Access in Rural Areas

Resource limitations confine immunophenotyping and molecular labs to tertiary centers. Case series from low-income regions reveal splenectomy still substituted for cladribine because supply chains do not consistently stock purine analogues. Hematologist shortages persist, with 113 radiation oncologists serving 110 million citizens in the Philippines, a ratio that illustrates systemic gaps. Tele-oncology mitigates but does not yet erase these disparities, as patchy internet coverage curtails video consultation reliability in remote districts.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Next-Generation Targeted Therapies

- MRD-Guided Retreatment Algorithms

- High Cost of Novel Targeted Agents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Targeted modalities are registering the swiftest momentum, as the segment is expected to grow at an 8.21% CAGR through 2031. Near-universal BRAF V600E positivity provides a clear biomarker, and the vemurafenib-rituximab pair achieves a 96% complete response, solidifying the proof of concept. BTK inhibition furnishes an alternative axis for relapsed or mutation-resistant subsets, and early-line integration trials are underway. Immunotoxin therapy, such as CD22-directed moxetumomab pasudotox, remains reserved for multiply relapsed disease because of capillary leak risk and price considerations.

Chemotherapy maintains a significant presence, accounting for 60.78% of the hairy cell leukemia treatment market share in 2025. Cladribine and pentostatin remain frontline standards, thanks to 80% or higher complete remission rates and decades of clinician familiarity. Rituximab co-administration enhances the depth of response while reducing relapse frequency, thereby maintaining the relevance of chemotherapy. Emerging subcutaneous formulations support outpatient or home deployment, helping to fend off share erosion.

Geography Analysis

North America steered 41.95% of 2025 global sales, anchored by dense networks of specialty hematology centers that facilitate rapid adoption of innovative regimens and real-time MRD surveillance. FDA decisions continue to influence worldwide standard-setting, with breakthrough labels cutting development timelines from years to months. Tele-oncology services have grown rapidly; the Mayo Clinic reports oncology virtual-care completion rates above 90%, broadening specialist reach.

Asia-Pacific is set to grow at an 8.55% CAGR owing to expanding tertiary care capacity and policy frameworks that encourage clinical trial hosting. Chinese leukemia incidence stabilizes, yet survival metrics improve as technology diffusion continues. India's updated trial guidelines now align with ICH-GCP, accelerating start-up timelines and enhancing safety governance. This ecosystem invites multinational sponsors to enroll previously unserved patients, bolstering early access.

Europe benefits from the EMA's centralized approval mechanism, permitting simultaneous market entry across member states once reimbursement dossiers clear national HTA bodies. Pan-regional cooperative research groups sustain high enrollment for investigator-initiated trials, particularly those comparing novel kinase inhibitors against purine analog benchmarks.

Latin America, the Middle East, and Africa record gradual uptake, yet supply chain gaps and reimbursement constraints hinder pace. Splenectomy persists in certain low-resource pockets, reflecting therapy access shortfalls. International partnerships that supply subsidized drug, diagnostic kits, and telepathology teaching promise to narrow disparity margins over the coming decade.

- GlaxoSmithKline

- Roche

- AstraZeneca

- Bristol-Myers Squibb

- Pfizer

- Sanofi

- Eli Lilly and Company

- Merck

- Novartis

- Abbvie

- Aurinia Pharmaceuticals

- UCB

- Biogen

- Viatris

- ImmuPharma

- RemeGen

- Idorsia

- Equillium

- Kyverna Therapeutics

- AnaptysBio

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence & Earlier Diagnosis of SLE

- 4.2.2 Rapid Approvals of Novel Biologics

- 4.2.3 Expansion of Companion-Diagnostic Biomarkers

- 4.2.4 Tele-Rheumatology Boosting Access in Underserved Areas

- 4.2.5 Venture Funding Surge for Autoimmune Biotech Platforms

- 4.2.6 Favorable Orphan-Drug & Fast-Track Designations

- 4.3 Market Restraints

- 4.3.1 High Therapy Cost & Reimbursement Hurdles

- 4.3.2 Safety Concerns: Infection & Malignancy Risks

- 4.3.3 Cold-Chain Complexity for mAbs & Cell Therapies

- 4.3.4 Physician Inertia Toward Switching from Legacy Steroids

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Treatment Type

- 5.1.1 Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- 5.1.2 Antimalarials

- 5.1.3 Corticosteroids

- 5.1.4 Immunosuppressants / DMARDs

- 5.1.5 Biologics

- 5.1.6 Stem-cell & Gene-based Therapies

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Intravenous

- 5.2.3 Subcutaneous

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 GlaxoSmithKline

- 6.3.2 F. Hoffmann-La Roche

- 6.3.3 AstraZeneca

- 6.3.4 Bristol Myers Squibb

- 6.3.5 Pfizer

- 6.3.6 Sanofi

- 6.3.7 Eli Lilly and Company

- 6.3.8 Merck & Co.

- 6.3.9 Novartis AG

- 6.3.10 AbbVie

- 6.3.11 Aurinia Pharmaceuticals

- 6.3.12 UCB

- 6.3.13 Biogen

- 6.3.14 Viatris Inc.

- 6.3.15 ImmuPharma

- 6.3.16 RemeGen

- 6.3.17 Idorsia

- 6.3.18 Equillium

- 6.3.19 Kyverna Therapeutics

- 6.3.20 AnaptysBio

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment