PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061502

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061502

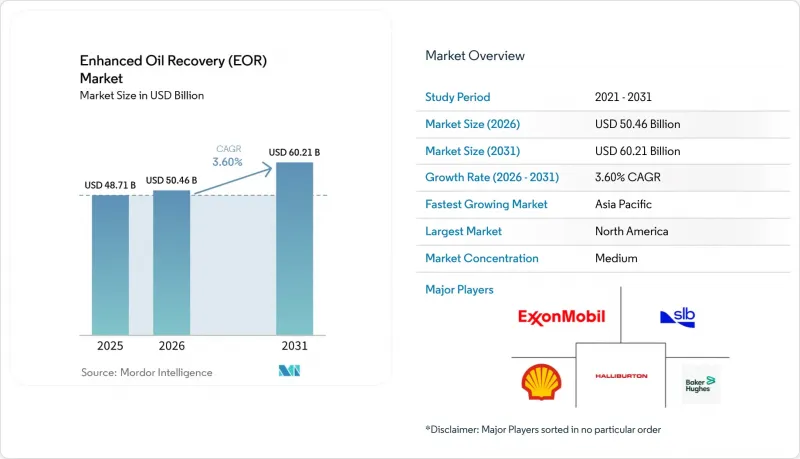

Enhanced Oil Recovery (EOR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the enhanced oil recovery market size is expected to grow from USD 48.71 billion in 2025 to USD 50.46 billion in 2026 and is forecast to reach USD 60.21 billion by 2031 at 3.6% CAGR over 2026-2031.

This report is Segmented by Technology (Gas Injection, Thermal Injection, Chemical Injection, Microbial EOR, and Hybrid and Emerging), Reservoir Type (Sandstone, Carbonate, Heavy Oil and Bitumen, and Tight/Shale), Field Maturity (Mature Fields, Brownfields, and Greenfields), Location of Deployment (Onshore and Offshore), and Geography (North America, Europe, Asia-Pacific, South America, and More).

Global Enhanced Oil Recovery (EOR) Market Trends and Insights

Depleting Conventional Reserves Pushing Tertiary Recovery

Global production still relies on reservoirs first drilled 30 or more years ago, and primary plus secondary techniques leave as much as 60% of original oil in place. Operators are therefore prioritizing tertiary methods that can be layered onto existing infrastructure with minimal surface disruption. Improved reservoir imaging now pinpoints previously unswept zones, enabling selective injection that boosts recovery without the need for extensive infill drilling. Digital twins further reduce trial-and-error cycles by simulating fluid behaviour before field execution. As discovery volumes shrink and development wells move into more costly frontier acreage, EOR becomes the economically rational route for sustaining supply, insulating the enhanced oil recovery market against crude price swings.

Government-Backed CO2 Tax Incentives & CCUS Build-out

Production tax credits and severance tax reductions in key jurisdictions compress the payback periods for CO2 flood projects. The United States' 45Q credit adds a separate revenue stream for every tonne of CO2 permanently stored, converting emissions compliance into a cash flow. Saudi Arabia's plan for a 9 million tonnes per year capture hub at Jubail demonstrates how state entities are integrating capture, transport, and sequestration into a single, unified value chain. Fiscal support lowers the weighted average cost of capital, drawing ESG-constrained investors into barrels that now qualify as carbon-neutral. As more regions impose explicit carbon prices, the enhanced oil recovery market gains structural tailwinds rather than cyclic boosts.

High Cap-ex & Opex of Thermal Processes Under Price Volatility

Steam generators, water-treatment units, and fuel gas lines make thermal EOR the most capital-intensive option. Margins compress sharply when crude prices dip or natural-gas feedstock rises, causing operators to defer workovers. Regions with water scarcity must pay to truck in freshwater or install large recycling plants, adding operational burden. Emerging down-hole combustion tools promise efficiency gains yet still demand specialised crews and hardware logistics. These cost sensitivities divert budgets toward gas or chemical methods, limiting near-term expansion of steam-dominated projects in the enhanced oil recovery market.

Other drivers and restraints analyzed in the detailed report include:

- Mature Fields in North America & Middle East Nearing Decline Curves

- CO2 Availability via New Blue/Green Hydrogen Projects

- ESG-Linked Lenders Excluding Incremental-Oil Projects

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermal methods contributed 44.85% of 2025 revenue, underscoring their entrenched role in heavy-oil plays across Canada and California. Steam-assisted gravity drainage and cyclic steam stimulation continue to yield predictable barrels, even as operators retrofit boilers with burners that use low-carbon fuels. Gas injection, led by miscible CO2 flooding, is posting the quickest global adoption, with a 6.42% CAGR outlook through 2031. The enhanced oil recovery market size for gas-injection projects is therefore expanding faster than any other technology cohort. Hybrid processes, low-salinity water alternating with CO2 or polymer slugs, are gaining traction in pilots because they combine the sweep of water floods with the miscibility gains of solvents. Laboratory breakthroughs in biosurfactants and electromagnetic heating show promise but remain at pre-commercial stages.

The competitiveness of gas injection rises where industrial hubs guarantee a low-cost anthropogenic CO2 supply. U.S. Gulf-Coast clusters already mix refinery off-gases into trunk lines that feed Permian injectors, while Middle East operators leverage ammonia and methanol plants for the same purpose . Steam remains dominant in bitumen deposits because reservoir viscosity still rules process choice. Nevertheless, the drive to curb scope-1 emissions nudges producers toward solvent-assisted steam generation, further blurring technology boundaries inside the enhanced oil recovery market.

Sandstone delivers 46.35% of current volumes thanks to its favourable porosity and long history of water flooding that preconditions reservoirs for tertiary stages. The enhanced oil recovery market share, led by sandstone, is under pressure from unconventional formations, where tight/shale reservoirs are expected to show a 7.59% CAGR outlook. Micro-fracture networks formed during horizontal drilling serve as pathways for surfactant and gas slugs, facilitating significant incremental recovery despite low matrix permeability. Carbonates pose wettability challenges; nonetheless, surfactant-polymer blends and smart-water techniques are incrementally improving recovery factors, especially in Middle East super-giants.

Digital-rock analytics helps operators model pore-scale flow in heterogenous carbonates, trimming design time for chemical formulations. Heavy-oil reservoirs still require thermal inputs due to their high viscosity, yet solvent-steamed hybrids are reducing water requirements by up to 30%, thereby easing ESG pressures. As geology dictates method selection, suppliers offering multi-technology portfolios capture greater value across reservoir classes, thereby reinforcing their competitive positioning in the enhanced oil recovery market.

Geography Analysis

North America leads the enhanced oil recovery market with a 39.75% revenue share in 2025, generated by large-scale CO2 floods in the Permian Basin and thermal operations in Alberta's oil sands. Federal and state incentives such as the 45Q credit and Wyoming's severance-tax exemption materially lower project breakevens, while an 8,000-km pipeline grid delivers anthropogenic CO2 at the field gate. ExxonMobil's 2024 earnings of USD 33.7 billion underscore the importance of integrated capture-to-pipeline business models in driving profitability, even under volatile market conditions.

The Asia-Pacific region is the fastest-growing, forecasted to grow at an 7.86% CAGR through 2031. PetroChina's polymer-flood programs in Daqing and CNOOC's pilot gas injection in Bohai Bay illustrate rapid technology diffusion. PTTEP earmarked THB 261 billion for 2025 upstream cap-ex, including pilot miscible gas systems in the Gulf of Thailand. Australia's Darwin CCUS hub and Japan's long-running offshore CO2 reinjection trials further expand regional skill sets. As industrial decarbonisation progresses, hydrogen-linked CO2 supply clusters in China, Korea, and India will reinforce growth fundamentals for the enhanced oil recovery market.

Europe maintains steady momentum, anchored by the UK and Norway, where North Sea operators integrate CO2 storage with extended-reach drilling to tap attic oil zones. EU taxonomy rules classify permanent CO2 storage as sustainable, unlocking green bond financing channels for selected assets. The Middle East leverages giant naturally fractured carbonates; Saudi Aramco's Jubail hub targets 9 million tons per year (t/y) capture, much of which will enter miscible-gas floods at Ghawar and other super-giants. South America's growth centres on Brazilian pre-salt FPSOs equipped for reinjection loops and Venezuelan heavy-oil blocks poised for solvent-steam hybrids once sanctions ease in the enhanced oil recovery market.

Together, geography-specific policy and resource conditions shape divergent adoption curves; yet, each region now embeds EOR into its long-term supply planning, thereby cementing demand across the enhanced oil recovery market.

- Baker Hughes Company

- Schlumberger Ltd.

- Halliburton Company

- Exxon Mobil Corp.

- Shell plc

- BP plc

- TotalEnergies SE

- Chevron Corp.

- Weatherford International plc

- Praxair/Linde plc

- Occidental Petroleum Corp.

- Denbury Inc.

- Cenovus Energy Inc.

- China National Petroleum Corp. (CNPC)

- Sinopec

- Petrobras

- Petronas

- ConocoPhillips

- Eni SpA

- EOG Resources

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Depleting conventional reserves pushing tertiary recovery

- 4.2.2 Government-backed CO2 tax incentives & CCUS build-out

- 4.2.3 Mature fields in N. America & Middle East nearing decline curves

- 4.2.4 CO? availability via new blue/green hydrogen projects

- 4.2.5 Offshore digital-rock analytics cutting EOR screening cost

- 4.2.6 Low-salinity nanofluid blends lowering chemical dose

- 4.3 Market Restraints

- 4.3.1 High cap-ex & opex of thermal processes under price volatility

- 4.3.2 Water-use & emissions permitting delays

- 4.3.3 Food-grade CO2 shortages outside U.S. pilot clusters

- 4.3.4 ESG-linked lenders excluding incremental-oil projects

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Gas Injection (CO2 Miscible Flooding, Nitrogen Injection, Hydrocarbon Gas Injection)

- 5.1.2 Thermal Injection (Steam Flooding, In-situ Combustion, Cyclic Steam Stimulation)

- 5.1.3 Chemical Injection (Polymer Flooding, Surfactant-Polymer (SP), Alkali-Surfactant-Polymer (ASP), Nanofluid EOR)

- 5.1.4 Microbial EOR (Biosurfactant Flooding, Biopolymer Flooding)

- 5.1.5 Hybrid and Emerging (Low-Salinity Waterflooding, CO2-WAG, EM-Assisted Heating)

- 5.2 By Reservoir Type

- 5.2.1 Sandstone

- 5.2.2 Carbonate

- 5.2.3 Heavy Oil and Bitumen

- 5.2.4 Tight/Shale

- 5.3 By Field Maturity

- 5.3.1 Mature Fields

- 5.3.2 Brownfields

- 5.3.3 Greenfields

- 5.4 By Location of Deployment

- 5.4.1 Onshore

- 5.4.2 Offshore

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Egypt

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Baker Hughes Company

- 6.4.2 Schlumberger Ltd.

- 6.4.3 Halliburton Company

- 6.4.4 Exxon Mobil Corp.

- 6.4.5 Shell plc

- 6.4.6 BP plc

- 6.4.7 TotalEnergies SE

- 6.4.8 Chevron Corp.

- 6.4.9 Weatherford International plc

- 6.4.10 Praxair/Linde plc

- 6.4.11 Occidental Petroleum Corp.

- 6.4.12 Denbury Inc.

- 6.4.13 Cenovus Energy Inc.

- 6.4.14 China National Petroleum Corp. (CNPC)

- 6.4.15 Sinopec

- 6.4.16 Petrobras

- 6.4.17 Petronas

- 6.4.18 ConocoPhillips

- 6.4.19 Eni SpA

- 6.4.20 EOG Resources

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment