PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061524

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061524

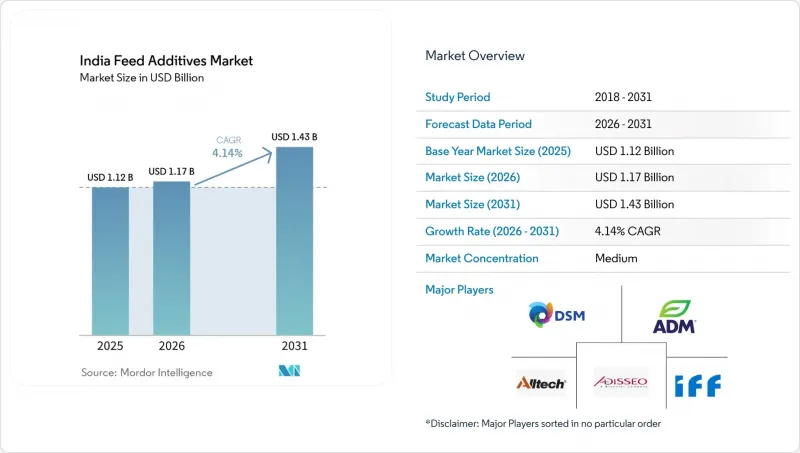

India Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, india feed additives market size in 2026 is estimated at USD 1.17 billion, growing from 2025 value of USD 1.12 billion with 2031 projections showing USD 1.43 billion, growing at 4.14% CAGR over 2026-2031.

This report is Segmented by Additive (Acidifiers, Amino Acids, Antibiotics, Antioxidants, Binders, Enzymes, Flavors and Sweeteners, Minerals, Mycotoxin Detoxifiers, Phytogenics, Pigments, Prebiotics, Probiotics, Vitamins, and Yeast), Animal (Aquaculture, Poultry, Ruminant, Swine, and Other Animals). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

India Feed Additives Market Trends and Insights

Rising Industrial Poultry Production

Commercial broiler and layer farms produced more than 4.5 million tons of chicken meat and over 140 billion eggs in 2024. Integration levels crossed 80%, creating uniform nutritional protocols that rely on enzymes, amino acids, and organic acids. Major integrators linked performance bonuses to feed conversion ratios, so nutritionists aggressively adopt solutions demonstrated to deliver a measurable return. Standardized housing and automated feeders enable precise inclusion rates for heat-stable phytogenics and next-generation phytases. Early adopters report a 4% improvement in feed efficiency when phytase is combined with probiotics, further entrenching demand for premium functional additives. These practices reinforce the long-term expansion path of the India feed additives market.

Ban on Antibiotic Growth Promoters

The Food Safety and Standards Authority of India banned colistin, chloramphenicol, and nitrofurans in 2024. Eliminating these growth promoters pushed integrators toward probiotics, prebiotics, enzymes, and phytogenics that safeguard gut health without antimicrobial residues. Probiotic sales rose 23% year over year in 2025 as poultry integrators reformulated rations to comply with updated maximum-residue thresholds. Feed compounders also replaced in-feed antibiotics with organic acids that lower gut pH and suppress pathogens. International suppliers capitalized on this inflection by launching heat-stable Bacillus spores engineered to survive pelleting temperatures up to 90 °C. As the ban expands to cover additional molecules, the India feed additives market will increasingly favor natural performance enhancers.

Raw-Material Price Volatility

Maize prices climbed to INR 2,425 per quintal (USD 293 per metric ton) in early 2025 due to ethanol diversion, while soybean meal hovered at INR 52,000 per ton (USD 630 per metric ton). Feed accounts for 65% of poultry production cost, so any spike immediately erodes margins. Feed mills responded by stockpiling 60-day inventory and reformulating with enzymes that unlock non-starch polysaccharides, reducing corn inclusion by 3-5 percentage points. However, currency swings and freight charges still feed uncertainty into pricing. Small dairy and swine farms cut additive budgets first, temporarily damping overall volumes in the India feed additives market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Aquaculture Output and Export Incentives

- Expansion of Integrated Feed Mills

- Cold-Chain Gaps Restraining Probiotic Viability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amino acids retained a 19.05% share of the India feed additives market in 2025, while antioxidants, though smaller, are growing fastest at a 4.65% CAGR because volatile ingredient prices lengthen feed storage cycles and raise rancidity risk. are forecast to rise at a 3.74% CAGR through 2031 as feed formulators fine-tune protein levels for margin relief. The category commanded USD 213.4 million of the India feed additives market size in 2025 and benefits from the Production Linked Incentive scheme that encourages domestic lysine and methionine capacity. Local fermentation reduces freight premiums and mitigates Chinese supply risk, allowing integrators to lock in contracts at steady prices. Tryptophan usage doubled since 2023, reflecting adoption in specialty layer rations aimed at stress reduction. Enzyme portfolios continue to diversify with xylanases and proteases tailored to high-fiber regional diets. Probiotics and phytogenics see variable uptake depending on cold chain access, but heat-stable Bacillus spores and turmeric-derived essential oils post above-market growth. BIS quality mandates are pushing out sub-scale blenders and consolidating share toward established brands, including DSM-Firmenich and Trouw Nutrition, which both operate ISO-certified premix lines.

Demand for vitamin and mineral premixes remains stable across livestock species. Mycotoxin detoxifiers are gaining traction after aflatoxin outbreaks in maize shipments heightened awareness in dairy cooperatives. Yeast cell-wall derivatives used as immune modulators are entering poultry starter diets as antibiotic replacements. Collectively, these trends underpin steady gains for additive suppliers that offer scientifically validated products and robust local distribution, reinforcing revenue momentum in the India feed additives market.

List of Companies Covered in this Report:

- Adisseo

- Archer Daniel Midland Co.

- BASF SE

- Alltech, Inc.

- Cargill Inc.

- DSM Nutritional Products AG

- Solvay S.A.

- IFF(Danisco Animal Nutrition)

- Kerry Group Plc

- SHV (Nutreco NV)

- Evonik Industries AG

- Elanco Animal Health Inc.

- Novus International, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Rising Industrial Poultry Production Drives Feed Additive Uptake

- 4.5.2 Antibiotic Growth-Promoter Ban Reshapes Additive Mix

- 4.5.3 Aquaculture Incentives Spur Specialty Additives

- 4.5.4 Integrated Feed Mill Expansion Boosts Distribution Efficiency

- 4.5.5 PLI scheme lowering domestic amino-acid costs

- 4.5.6 Precision livestock farming enabling micro-dosing

- 4.6 Market Restraints

- 4.6.1 Volatile Raw-Material Prices Inflate Production Costs

- 4.6.2 Lengthy and Complex Regulatory Approvals

- 4.6.3 Cold-chain gaps Restraining probiotic viability

- 4.6.4 Backyard desi poultry limiting additive uptake

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Additive

- 5.1.1 Acidifiers

- 5.1.1.1 By Sub Additive

- 5.1.1.1.1 Fumaric Acid

- 5.1.1.1.2 Lactic Acid

- 5.1.1.1.3 Propionic Acid

- 5.1.1.1.4 Other Acidifiers

- 5.1.1.1 By Sub Additive

- 5.1.2 Amino Acids

- 5.1.2.1 By Sub Additive

- 5.1.2.1.1 Lysine

- 5.1.2.1.2 Methionine

- 5.1.2.1.3 Threonine

- 5.1.2.1.4 Tryptophan

- 5.1.2.1.5 Other Amino Acids

- 5.1.2.1 By Sub Additive

- 5.1.3 Antibiotics

- 5.1.3.1 By Sub Additive

- 5.1.3.1.1 Bacitracin

- 5.1.3.1.2 Penicillins

- 5.1.3.1.3 Tetracyclines

- 5.1.3.1.4 Tylosin

- 5.1.3.1.5 Other Antibiotics

- 5.1.3.1 By Sub Additive

- 5.1.4 Antioxidants

- 5.1.4.1 By Sub Additive

- 5.1.4.1.1 Butylated Hydroxyanisole (BHA)

- 5.1.4.1.2 Butylated Hydroxytoluene (BHT)

- 5.1.4.1.3 Citric Acid

- 5.1.4.1.4 Ethoxyquin

- 5.1.4.1.5 Propyl Gallate

- 5.1.4.1.6 Tocopherols

- 5.1.4.1.7 Other Antioxidants

- 5.1.4.1 By Sub Additive

- 5.1.5 Binders

- 5.1.5.1 By Sub Additive

- 5.1.5.1.1 Natural Binders

- 5.1.5.1.2 Synthetic Binders

- 5.1.5.1 By Sub Additive

- 5.1.6 Enzymes

- 5.1.6.1 By Sub Additive

- 5.1.6.1.1 Carbohydrases

- 5.1.6.1.2 Phytases

- 5.1.6.1.3 Other Enzymes

- 5.1.6.1 By Sub Additive

- 5.1.7 Flavors & Sweeteners

- 5.1.7.1 By Sub Additive

- 5.1.7.1.1 Flavors

- 5.1.7.1.2 Sweeteners

- 5.1.7.1 By Sub Additive

- 5.1.8 Minerals

- 5.1.8.1 By Sub Additive

- 5.1.8.1.1 Macrominerals

- 5.1.8.1.2 Microminerals

- 5.1.8.1 By Sub Additive

- 5.1.9 Mycotoxin Detoxifiers

- 5.1.9.1 By Sub Additive

- 5.1.9.1.1 Binders

- 5.1.9.1.2 Biotransformers

- 5.1.9.1 By Sub Additive

- 5.1.10 Phytogenics

- 5.1.10.1 By Sub Additive

- 5.1.10.1.1 Essential Oil

- 5.1.10.1.2 Herbs & Spices

- 5.1.10.1.3 Other Phytogenics

- 5.1.10.1 By Sub Additive

- 5.1.11 Pigments

- 5.1.11.1 By Sub Additive

- 5.1.11.1.1 Carotenoids

- 5.1.11.1.2 Curcumin & Spirulina

- 5.1.11.1 By Sub Additive

- 5.1.12 Prebiotics

- 5.1.12.1 By Sub Additive

- 5.1.12.1.1 Fructo Oligosaccharides

- 5.1.12.1.2 Galacto Oligosaccharides

- 5.1.12.1.3 Inulin

- 5.1.12.1.4 Lactulose

- 5.1.12.1.5 Mannan Oligosaccharides

- 5.1.12.1.6 Xylo Oligosaccharides

- 5.1.12.1.7 Other Prebiotics

- 5.1.12.1 By Sub Additive

- 5.1.13 Probiotics

- 5.1.13.1 By Sub Additive

- 5.1.13.1.1 Bifidobacteria

- 5.1.13.1.2 Enterococcus

- 5.1.13.1.3 Lactobacilli

- 5.1.13.1.4 Pediococcus

- 5.1.13.1.5 Streptococcus

- 5.1.13.1.6 Other Probiotics

- 5.1.13.1 By Sub Additive

- 5.1.14 Vitamins

- 5.1.14.1 By Sub Additive

- 5.1.14.1.1 Vitamin A

- 5.1.14.1.2 Vitamin B

- 5.1.14.1.3 Vitamin C

- 5.1.14.1.4 Vitamin E

- 5.1.14.1.5 Other Vitamins

- 5.1.14.1 By Sub Additive

- 5.1.15 Yeast

- 5.1.15.1 By Sub Additive

- 5.1.15.1.1 Live Yeast

- 5.1.15.1.2 Selenium Yeast

- 5.1.15.1.3 Spent Yeast

- 5.1.15.1.4 Torula Dried Yeast

- 5.1.15.1.5 Whey Yeast

- 5.1.15.1.6 Yeast Derivatives

- 5.1.15.1 By Sub Additive

- 5.1.1 Acidifiers

- 5.2 By Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.1.1 By Sub Animal

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.2.1 By Sub Animal

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Adisseo

- 6.4.2 Archer Daniel Midland Co.

- 6.4.3 BASF SE

- 6.4.4 Alltech, Inc.

- 6.4.5 Cargill Inc.

- 6.4.6 DSM Nutritional Products AG

- 6.4.7 Solvay S.A.

- 6.4.8 IFF(Danisco Animal Nutrition)

- 6.4.9 Kerry Group Plc

- 6.4.10 SHV (Nutreco NV)

- 6.4.11 Evonik Industries AG

- 6.4.12 Elanco Animal Health Inc.

- 6.4.13 Novus International, Inc.

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS