PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063826

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063826

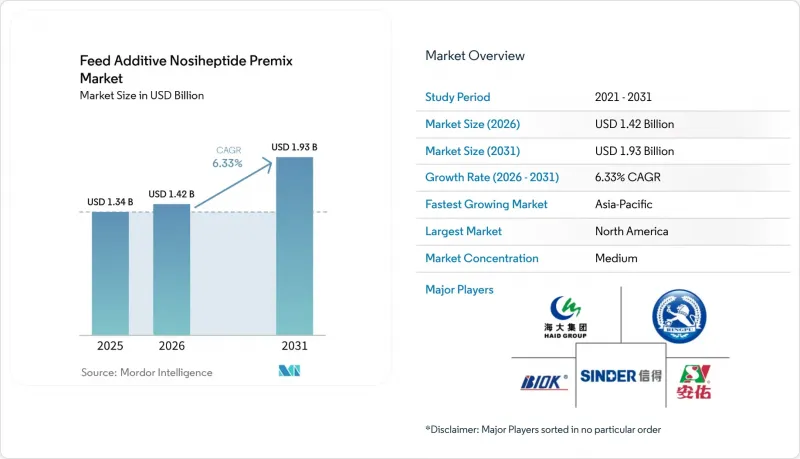

Feed Additive Nosiheptide Premix - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the feed additive nosiheptide premix market size is projected to grow from USD 1.34 billion in 2025 to USD 1.42 billion in 2026, reaching USD 1.93 billion by 2031, with a CAGR of 6.33% over 2026-2031.

This report is Segmented by Livestock (Poultry, Swine, Ruminants, Aquaculture, and Other Livestocks), by Formulation Type (Conventional Premix and Organic/Non-GMO Premix), by Source (Synthetic Nosiheptide and Bio-Fermented Nosiheptide), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Feed Additive Nosiheptide Premix Market Trends and Insights

Regulatory Push for Antibiotic Replacement

Stringent antimicrobial stewardship regulations in the United States are driving the adoption of alternatives such as nosiheptide premixes in animal feed. In 2024, the United States Food and Drug Administration (FDA) strengthened its antimicrobial resistance strategy through Guidance for Industry (GFI) 263 and related stewardship initiatives. These measures mandate that medically important antimicrobial drugs for animals remain under veterinary oversight and promote their judicious use in livestock production . As a result, feed manufacturers and producers are increasingly turning to non-medically important alternatives, such as nosiheptide, to sustain feed efficiency and productivity while complying with evolving antimicrobial resistance policies.

Growth of Poultry Meat Exports from Asia-Pacific

Increasing poultry meat exports from Asia are driving demand for specialized feed additives, including nosiheptide premixes. According to the Rabobank Global Poultry Quarterly (2025), global processed chicken trade reached approximately 400,000 metric tons in Q4 2024, marking a 15% year-on-year growth . This growth was supported by significant export contributions from Asian producers such as Thailand and China. The expansion in exports is prompting producers to adopt feed solutions that comply with strict residue and traceability standards, leading to greater use of nosiheptide to ensure compliance while maintaining productivity and efficiency.

Stringent Residue-Testing Regimes in the European Union

Stringent residue-testing regulations in the European Union are driving up compliance costs for feed additive manufacturers. Commission Regulation (EU) 2024/1229 sets maximum cross-contamination limits for 24 antimicrobial substances in non-target feed . This regulation requires the use of highly sensitive analytical methods for detection. The strict thresholds necessitate advanced technologies, such as high-resolution chromatography, which increase testing complexity and operational expenses. Smaller premix manufacturers, particularly those lacking dedicated production lines or accredited laboratories, face significant challenges in meeting these requirements. This situation limits their market participation and benefits larger, vertically integrated companies with established quality-control systems.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Antibiotic-Free Labeling Premiums

- Scale-Up of Precision-Fermentation Manufacturing

- Volatility of Nosiheptide API Supply from China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Poultry accounted for the largest 54% share of the feed additive nosiheptide premix market in 2025. This dominance was driven by intensive broiler production systems and strong export-oriented demand. Short production cycles enable quicker adjustments to feed formulations, leading to greater additive utilization in commercial operations. Export markets demand low-residue feed solutions to comply with stringent import standards, further solidifying poultry's leading position. Swine represents a secondary segment, supported by gut health management needs, while aquaculture adoption is gradually increasing due to stricter biosecurity and disease-prevention measures.

The poultry segment market size is projected to grow at the fastest CAGR of 7.8% from 2026 to 2031. This growth is attributed to increasing global poultry consumption and the expansion of intensive farming systems. The growing preference for antibiotic-free meat production is driving the adoption of non-medically important feed additives that ensure performance and feed efficiency. Poultry producers benefit from shorter production cycles, enabling faster integration of new feed technologies. This adaptability, combined with strong export demand and regulatory compliance, positions poultry as the fastest-growing segment in the market.

Geography Analysis

North America is accounted for the largest 36% of the feed additive nosiheptide premix market share in 2025. This dominance is attributed to strict regulatory frameworks and the widespread adoption of antibiotic-free livestock production systems. The United States Food and Drug Administration mandates veterinary oversight for medically important antimicrobials, driving the transition toward non-medically important alternatives. Additionally, vertically integrated poultry producers in the region leverage advanced feed management systems and quickly adopt new formulations, thereby ensuring steady demand for specialized feed additives such as nosiheptide in commercial livestock production.

The Asia-Pacific region is projected to register the fastest CAGR of 7.9% from 2026 to 2031, driven by the growth of livestock production and export-oriented supply chains. Rising meat consumption and the intensification of farming systems are promoting the adoption of performance-enhancing feed additives. Regional producers are investing in feed manufacturing infrastructure and modern production practices to serve both domestic and international markets. Countries like China, Thailand, and Vietnam are enhancing their roles in global poultry exports, which is driving the demand for specialized additives that comply with stringent residue and quality standards.

Europe represents a mature but value-driven market, supported by stringent regulatory frameworks and increasing demand for certified livestock production systems. Strict policies on antimicrobial usage and residue compliance are encouraging producers to shift toward non-medically important feed additives. Livestock producers are adopting advanced traceability systems and certified feed inputs to meet regulatory and retailer requirements. This transition increases operational complexity and production costs, particularly for smaller manufacturers. At the same time, strong demand for antibiotic-free and organic animal products supports premium pricing, enabling suppliers to offset compliance costs while maintaining profitability across the region.

- Zhejiang Shenghua Biok Biology Co., Ltd.

- Tianjin Ringpu Bio-Pharmacy Co., Ltd.

- Anyou Biotechnology Group Co., Ltd.

- Guangdong Haid Group Co., Ltd.

- Shandong Shengli Bioengineering Co., Ltd.

- Zhejiang Esigma Animal Health Co., Ltd.

- Shandong Sinder Technology Co., Ltd.

- Hainan Zhongxin Chemical Co., Ltd.

- Anyou Biotechnology Group Co., Ltd.

- Fengchen Group Co., Ltd.

- Anhui Wanbei Pharmaceutical Co., Ltd.

- Zhejiang University Sunny Nutrition Technology Co., Ltd.

- Chattha Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for antibiotic replacement

- 4.2.2 Growth of poultry meat exports from Asia-Pacific

- 4.2.3 Emergence of antibiotic-free labeling premiums

- 4.2.4 Scale-up of precision-fermentation manufacturing

- 4.2.5 Integration of premix dosing automation at feed mills

- 4.2.6 Rising venture funding for narrow-spectrum antimicrobials

- 4.3 Market Restraints

- 4.3.1 Stringent residue-testing regimes in the European Union

- 4.3.2 Volatility of nosiheptide API supply from China

- 4.3.3 Slower adoption in ruminant rations

- 4.3.4 Price competition from bacitracin and tylosin premixes

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Livestock

- 5.1.1 Poultry

- 5.1.2 Swine

- 5.1.3 Ruminants

- 5.1.4 Aquaculture

- 5.1.5 Other Livestock

- 5.2 By Formulation Type

- 5.2.1 Conventional Premix

- 5.2.2 Organic/Non-GMO Premix

- 5.3 By Source

- 5.3.1 Synthetic Nosiheptide

- 5.3.2 Bio-fermented Nosiheptide

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Zhejiang Shenghua Biok Biology Co., Ltd.

- 6.4.2 Tianjin Ringpu Bio-Pharmacy Co., Ltd.

- 6.4.3 Anyou Biotechnology Group Co., Ltd.

- 6.4.4 Guangdong Haid Group Co., Ltd.

- 6.4.5 Shandong Shengli Bioengineering Co., Ltd.

- 6.4.6 Zhejiang Esigma Animal Health Co., Ltd.

- 6.4.7 Shandong Sinder Technology Co., Ltd.

- 6.4.8 Hainan Zhongxin Chemical Co., Ltd.

- 6.4.9 Anyou Biotechnology Group Co., Ltd.

- 6.4.10 Fengchen Group Co., Ltd.

- 6.4.11 Anhui Wanbei Pharmaceutical Co., Ltd.

- 6.4.12 Zhejiang University Sunny Nutrition Technology Co., Ltd.

- 6.4.13 Chattha Group

7 Market Opportunities and Future Outlook