PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061536

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061536

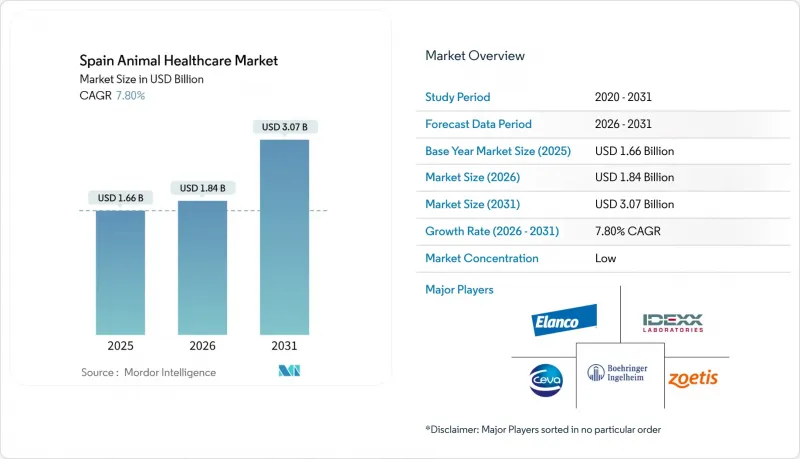

Spain Animal Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the spain animal healthcare market size is projected to be USD 1.66 billion in 2025, USD 1.84 billion in 2026, and reach USD 3.07 billion by 2031, growing at a CAGR of 7.80% from 2026 to 2031.

This report is Segmented by Product (Therapeutics and Diagnostics), Animal Type (Companion Animals and Livestock Animals), Route of Administration (Oral, Parenteral, Topical, Others), and Distribution Channel (Veterinary Clinics & Hospitals, Retail Pharmacies, Online Pharmacies & E-Commerce, On-Farm / Direct Supply). Market Forecasts are Provided in Terms of Value (USD).

Spain Animal Healthcare Market Trends and Insights

Rising Pet Ownership & Humanisation

In 2024, Spain's pet population reached 9.46 million dogs and 5.95 million cats, with 49% of households owning at least one pet and 39% of owners identifying as "pet parents." Increased attachment is evident as 74% of pet owners include pets in family photos and 71% purchase holiday gifts, driving demand for vaccines, parasiticides, and diagnostics. Pet-related spending is projected to hit EUR 3.8 billion (USD 4.18 billion) by 2030, with urban households favoring premium products and frequent clinic visits. Preferences lean towards palatable chews and combination parasiticides, while lighter regulatory pathways for companion products accelerate innovation cycles.

EU "One-Health" Regulation Stimulating Preventive Care

EU Regulation 2019/6, implemented through Spanish Royal Decree 1157/2021, restricts prophylactic antimicrobial use and enforces stricter prescribing standards, redirecting budgets to vaccinations and diagnostics. By 2024, Spain reduced livestock antibiotic use by 70%, the highest in the EU, boosting vaccine adoption and alternatives to critical antimicrobials. Producers must now identify pathogens before accessing restricted classes, increasing demand for rapid tests and PCR panels. Compliance costs challenge smallholders, while integrated producers benefit from economies of scale. Non-compliance penalties push preventive strategies as standard practice, aligning the market with vaccines and diagnostics.

Veterinarian Shortage, Particularly in Rural Spain

In 2024, Spain reported 37,836 registered veterinarians, yet rural areas face persistent staffing shortages relative to livestock populations. This gap delays treatments and increases reliance on non-specialist labor. New graduates prefer urban areas due to better compensation and predictable schedules, while rural livestock roles struggle to compete. Consolidators attract young veterinarians with salaried roles and centralized support, further concentrating talent in urban clinics. The shortage impacts the economy, as delayed disease diagnoses can lead to movement restrictions and reduced farm revenues, as seen during the lumpy skin disease outbreak in Catalonia. Government proposals for mandatory rural service were withdrawn after objections, and alternatives like telemedicine and mobile units have not fully replaced hands-on care. This structural gap hinders disease control and modernization for smallholder farms lacking resources to standardize protocols.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Point-of-Care Diagnostics

- Growing Pet-Insurance Penetration Enabling Spend

- High Cost of Advanced Therapeutics & Diagnostics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, therapeutics dominated Spain's animal healthcare market with a 64.6% share, but diagnostics are projected to grow at an 11.5% CAGR through 2031, outpacing the baseline. Vaccines remain central to therapeutics, driven by national programs targeting diseases such as bovine tuberculosis and brucellosis, ensuring predictable purchasing and adherence to protocols. Subsidized vaccine campaigns enhance herd immunity and reduce reliance on antimicrobials. Parasiticides, particularly isoxazoline combinations, are gaining traction due to their broad-spectrum coverage and ease of administration, aligning with urban pet owners' preferences. Anti-infectives remain vital for specific cases, though diagnostics-first policies are increasingly emphasized in livestock. Diagnostics are advancing as clinics adopt in-house platforms delivering rapid results, enabling same-visit treatments and boosting client satisfaction. In livestock, tools like PCR screening and rapid tests help detect pathogens early, reducing depopulation costs. This shift toward diagnostics is driving sustained growth despite price sensitivity, as clinics embed point-of-care workflows.

In 2025, companion animals accounted for 58.5% of Spain's animal healthcare market, growing at a 10.2% CAGR, supported by urban ownership rates and increased spending on diagnostics, vaccines, and preventive care. Cats are the fastest-growing sub-segment, driven by the 2024 launch of feline-specific vaccines. Policy stability and lighter regulations enable premium pricing through formulation upgrades, while rising insurance penetration supports higher-ticket procedures. Livestock is projected to grow faster at an 11.8% CAGR through 2031, as producers prioritize biosecurity to protect exports and productivity. Spain's leadership in pig production and ruminant herds ensures steady demand for vaccines and diagnostics, supported by digital platforms consolidating health data for better oversight. Recent disease outbreaks highlight the importance of early detection and prevention-first strategies, which are driving livestock growth dynamics alongside companion demand.

List of Companies Covered in this Report:

- Bioiberica

- BioVet SA

- Boehringer Ingelheim

- Ceva

- Dechra Pharmaceuticals Inc.

- Elanco

- Hipra

- IDEXX

- Laboratorios Eurisko

- Laboratorios Karizoo

- Laboratorios Syva

- MSD Animal Health (Merck)

- Neogen

- S.P. Veterinaria

- Super's Diana S.L.

- Vetoquinol

- Virbac

- Zoetis

- Zoopan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Pet Ownership & Humanisation

- 4.2.2 EU One-Health Regulation Stimulating Preventive Care

- 4.2.3 Technological Advances in Point-of-Care Diagnostics

- 4.2.4 Growing Pet-Insurance Penetration Enabling Spend

- 4.2.5 Tele-Veterinary Adoption in Underserved Rural Areas

- 4.2.6 Government Subsidies for Iberian-Pig Disease Eradication

- 4.3 Market Restraints

- 4.3.1 Veterinarian Shortage, Particularly in Rural Spain

- 4.3.2 High Cost of Advanced Therapeutics & Diagnostics

- 4.3.3 Strict Antibiotic-Use Curbs Raising R&D Costs

- 4.3.4 Fragmented Distribution to Smallholder Farms

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Therapeutics

- 5.1.1.1 Vaccines

- 5.1.1.2 Parasiticides

- 5.1.1.3 Anti-infectives

- 5.1.1.4 Medical Feed Additives

- 5.1.1.5 Other Therapeutics

- 5.1.2 Diagnostics

- 5.1.2.1 Immunodiagnostic Tests

- 5.1.2.2 Molecular Diagnostics

- 5.1.2.3 Diagnostic Imaging

- 5.1.2.4 Clinical Chemistry

- 5.1.2.5 Other Diagnostics

- 5.1.1 Therapeutics

- 5.2 By Animal Type

- 5.2.1 Companion Animals

- 5.2.1.1 Dogs

- 5.2.1.2 Cats

- 5.2.1.3 Other Companion Animals

- 5.2.2 Livestock Animals

- 5.2.2.1 Ruminants (Cattle, Sheep, Goats)

- 5.2.2.2 Swine

- 5.2.2.3 Poultry

- 5.2.2.4 Other Livestock Animals

- 5.2.1 Companion Animals

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Parenteral (Injectables)

- 5.3.3 Topical

- 5.3.4 Others

- 5.4 By Distribution Channel

- 5.4.1 Veterinary Clinics & Hospitals

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies & e-Commerce

- 5.4.4 On-Farm / Direct Supply

6 Competitive Landscape

- 6.1 Market Concentration Analysis

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Bioiberica S.A.U.

- 6.3.2 BioVet SA

- 6.3.3 Boehringer Ingelheim GmbH

- 6.3.4 Ceva Sante Animale

- 6.3.5 Dechra Pharmaceuticals Inc.

- 6.3.6 Elanco Animal Health

- 6.3.7 HIPRA

- 6.3.8 IDEXX Laboratories

- 6.3.9 Laboratorios Eurisko

- 6.3.10 Laboratorios Karizoo

- 6.3.11 Laboratorios Syva

- 6.3.12 MSD Animal Health (Merck)

- 6.3.13 Neogen Corporation

- 6.3.14 S.P. Veterinaria

- 6.3.15 Super's Diana S.L.

- 6.3.16 Vetoquinol SA

- 6.3.17 Virbac

- 6.3.18 Zoetis Inc.

- 6.3.19 Zoopan

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment