PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061544

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061544

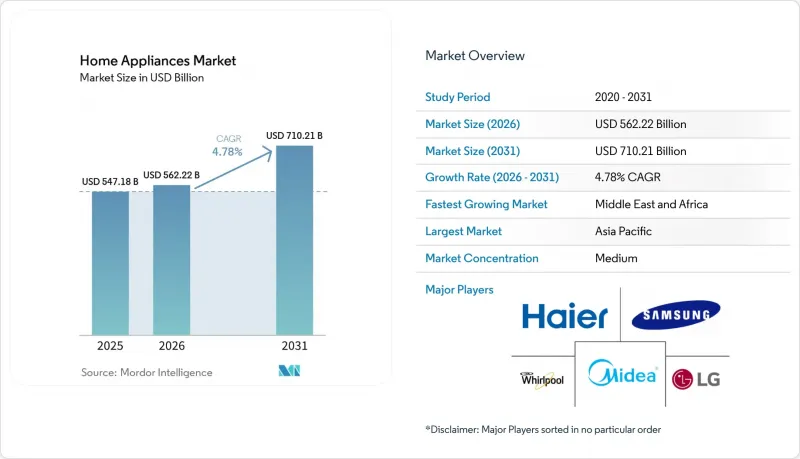

Home Appliances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the home appliances market size is expected to grow from USD 547.18 billion in 2025 to USD 562.22 billion in 2026 and is forecast to reach USD 710.21 billion by 2031 at 4.78% CAGR over 2026-2031.

This report is Segmented by Product (Major Appliances (Refrigerators, Freezers, and More), Small Appliances (Coffee Makers, Air Fryers, and More)), by Distribution Channel (Multi-Branded Stores, Exclusive Brand Outlets, Online, Other Distribution Channels), and by Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Home Appliances Market Trends and Insights

Rising Disposable Income and Consumer Spending Power

Rising disposable income across many economies supports upgrades and first-time purchases, which sustain unit volumes and enable trading up to premium features that save time and energy. Growth in real household income across several OECD economies in 2025 reinforced durable goods demand and created headroom for higher efficiency and smart-enabled appliances that reduce operating costs. Middle-class expansion in Asia and Latin America continues to influence the composition of the home appliances market, with household budgets tilting toward products that deliver tangible convenience or health benefits in daily routines. Policy support in large markets such as China has also encouraged replacement activity, lifting sales for compliant models and setting higher expectations for energy performance standards. As household budgets expand and urban lifestyles compress time available for chores, the adoption of dishwashers, efficient washers, and compact cooking appliances becomes more frequent in new-to-category cities. Income-led upgrades thus remain a durable catalyst for the home appliances market through 2031.

IoT-Enabled Convenience & Home Automation Boom

The proliferation of connected devices is fundamentally altering appliance value propositions, as consumers increasingly expect remote diagnostics, voice control, and integration with home energy-management platforms. The global count of connected IoT devices reached 21.1 billion in 2025, up 14% year-over-year, with Wi-Fi IoT claiming a 32% share of connections thanks to low-power Wi-Fi 6 features that enable battery-powered sensors and appliances. Home Energy Management Systems (HEMS) markets are projected to triple from USD 3.5 billion in 2023 to USD 10-12 billion by 2030, driven by clean-energy transitions and the need for demand flexibility in grids increasingly reliant on variable renewables. Smart home appliance penetration in U.S. households jumped from 13% to 22% in 2021 following pandemic-driven digital adoption, with manufacturers like LG and Samsung embedding AI chips directly into refrigerators and ovens to enable predictive maintenance alerts and automated recipe suggestions.

Commodity & Freight-Cost Volatility Compressing Margins

Input cost swings and logistics disruptions raise the delivered cost of appliances, prompting OEMs to balance pricing, promotion, and SKU mix. Commodity markets have shown intermittent tightness across base metals and energy, complicating cost planning and placing pressure on bill-of-materials for motors, compressors, and structural components. Freight networks have improved from peak congestion yet remain vulnerable to route disruptions and port delays that can create sporadic spikes in container costs. Manufacturers are expanding regional production and sourcing to cut shipping exposure and shorten lead times, which also improves service responsiveness in key end markets. Over the medium term, cost risk management and more localized manufacturing footprints are expected to remain core to margin resiliency in the home appliances market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of E-Commerce and Online Sales Channels

- Stricter Energy-Efficiency Mandates Spurring Replacement Demand

- High Initial Costs of Smart and Energy-Efficient Appliances

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerators accounted for 26.83% of the 2025 market size, reflecting their central role in replacement-driven demand and premiumization toward higher-efficiency formats. Refrigerators remain the single largest subcategory due to essential needs and long service lives that support upgrade cycles with better insulation, compressors, and connectivity. Laundry and cooling categories benefit from feature-led differentiation, including lower energy use and enhanced care modes, which help sustain higher average selling prices. Growing awareness of lifecycle running costs backs incremental trade-ups in large appliances, especially in urban middle-income households. With demand still tied to housing formation and renovations, the category's growth profile is steady rather than explosive, yet it underpins a large share of revenue in the home appliances market.

Small home appliances continue to outpace the overall market on unit growth, with air fryers registering an 8.0% CAGR as consumers seek healthier, space-saving cooking solutions. The category's appeal extends across demographics because it pairs quick preparation with lower energy use, a combination that is compelling for busy households. Robotic and cordless cleaning devices gain share as navigation improves and maintenance becomes more autonomous, lifting perceived value in daily use. Coffee makers and food preparation devices retain steady demand, supported by convenience and incremental smart features that simplify routines. This balance of accessible price points and visible utility keeps small appliances central to category expansion in the home appliances market.

Geography Analysis

Asia-Pacific led with 48.35% of the 2025 market size, confirming its role as the growth anchor for scale manufacturing, first-time ownership, and upgrading in key urban corridors. China's policy support for trade-ins and efficiency upgrades has encouraged replacement cycles that align with higher energy-performance thresholds. India's urbanization continues to expand the base of households purchasing frost-free refrigerators, split air conditioners, and front-load washers for the first time. Japan and South Korea show strong adoption of connected features, though replacement cycles are extending as repair services and warranties improve. Across the region, localization of manufacturing and targeted value engineering are central to price-accessible innovation in the home appliances market.

North America remains a high-value region characterized by replacement intensity and steady premiumization in efficiency and connected features. Expansions of United States manufacturing footprints by leading OEMs strengthen supply resilience, shorten lead times, and support service coverage in major categories. Domestic investments in air conditioning, water heating, and laundry lines also position manufacturers to capture demand from households upgrading for both comfort and energy savings. Retail remains a hybrid environment where research is often digital, but conversion and scheduling still favor trusted store formats for large items. This mix supports an environment where the home appliances market grows on the back of replacements, new construction, and targeted remodel activity.

Europe shows a large installed base under active efficiency and sustainability policies that shape product features and labeling across categories. Ecodesign frameworks and energy labels influence merchandising and consumer choice, which encourages replacement toward higher efficiency classes in refrigeration, laundry, and dishwashing. Specialty retail remains an important channel for premium brands, while e-commerce continues to gain share in smaller appliances. Product modularity and serviceability are rising priorities as right-to-repair initiatives move forward. This policy and retail context keep Europe central to innovation in energy efficiency within the home appliances market.

- Haier

- Whirlpool Corporation

- Samsung Electronics

- LG Electronics

- Bosch-Siemens Hausgerate

- Midea Group

- Electrolux AB

- Panasonic Corporation

- Philips Domestic Appliances

- GE Appliances

- Hisense

- Arcelik (Beko, Grundig)

- Sharp Corporation

- Gree Electric Appliances

- TCL Electronics

- Sub-Zero Group

- SMEG

- Dyson

- SharkNinja

- Fisher & Paykel

- Miele & Cie. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Disposable Income and Consumer Spending Power

- 4.2.2 IoT-Enabled Convenience & Home Automation Boom

- 4.2.3 Stricter Energy-Efficiency Mandates Spurring Replacement Demand

- 4.2.4 Growth of E-Commerce and Online Sales Channels

- 4.2.5 Urbanization and Changing Lifestyles

- 4.2.6 Premiumization and demand for feature-rich appliances

- 4.3 Market Restraints

- 4.3.1 Commodity & Freight-Cost Volatility Compressing Margins

- 4.3.2 High Initial Costs Of Smart And Energy-Efficient Appliances

- 4.3.3 Chip-Set Supply Bottlenecks Disrupting Production

- 4.3.4 Intense price competition and product commoditization

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Major Home Appliances

- 5.1.1.1 Refrigerators

- 5.1.1.2 Freezers

- 5.1.1.3 Washing Machines

- 5.1.1.4 Dishwashers

- 5.1.1.5 Ovens (Incl. Combi & Microwave)

- 5.1.1.6 Air Conditioners

- 5.1.1.7 Other Major Home Appliances (range hoods, cooktops, etc.)

- 5.1.2 Small Home Appliances

- 5.1.2.1 Coffee Makers

- 5.1.2.2 Food Processors

- 5.1.2.3 Grills and Roasters

- 5.1.2.4 Electric Kettles

- 5.1.2.5 Juicers and Blenders

- 5.1.2.6 Air Fryers

- 5.1.2.7 Vacuum Cleaners

- 5.1.2.8 Other Small Home Appliances (waffle makers, toasters, tea makers, rice cookers, etc.)

- 5.1.1 Major Home Appliances

- 5.2 By Distribution Channel

- 5.2.1 Multi-Brand Stores

- 5.2.2 Exclusive Brand Outlets

- 5.2.3 Online

- 5.2.4 Other Distribution Channels

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 Canada

- 5.3.1.2 United States

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Peru

- 5.3.2.3 Chile

- 5.3.2.4 Argentina

- 5.3.2.5 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Spain

- 5.3.3.5 Italy

- 5.3.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.3.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.3.3.8 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 India

- 5.3.4.2 China

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 South Korea

- 5.3.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.3.4.7 Rest of Asia-Pacific

- 5.3.5 Middle East And Africa

- 5.3.5.1 United Arab of Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East And Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Haier

- 6.4.2 Whirlpool Corporation

- 6.4.3 Samsung Electronics

- 6.4.4 LG Electronics

- 6.4.5 Bosch-Siemens Hausgerate

- 6.4.6 Midea Group

- 6.4.7 Electrolux AB

- 6.4.8 Panasonic Corporation

- 6.4.9 Philips Domestic Appliances

- 6.4.10 GE Appliances

- 6.4.11 Hisense

- 6.4.12 Arcelik (Beko, Grundig)

- 6.4.13 Sharp Corporation

- 6.4.14 Gree Electric Appliances

- 6.4.15 TCL Electronics

- 6.4.16 Sub-Zero Group

- 6.4.17 SMEG

- 6.4.18 Dyson

- 6.4.19 SharkNinja

- 6.4.20 Fisher & Paykel

- 6.4.21 Miele & Cie. KG

7 Market Opportunities & Future Outlook

- 7.1 Smart Home Ecosystem Integration