PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044143

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044143

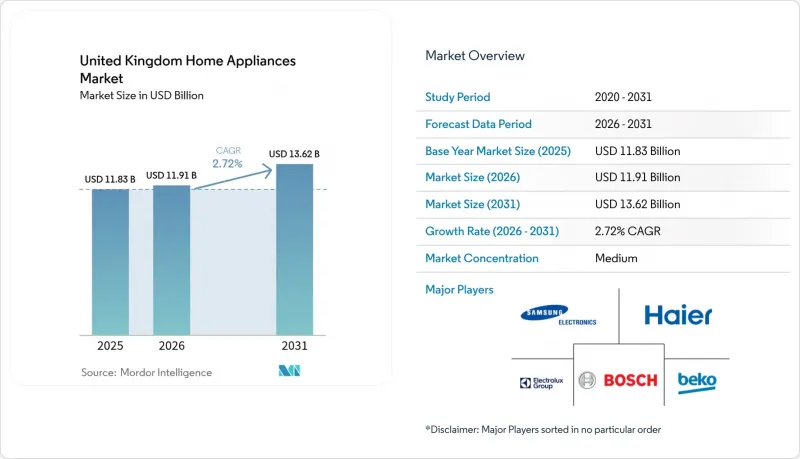

United Kingdom Home Appliances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United Kingdom home appliances market size is expected to grow from USD 11.83 billion in 2025 to USD 11.91 billion in 2026 and is forecast to reach USD 13.62 billion by 2031 at a 2.72% CAGR over 2026-2031.

The growth path reflects long appliance lifecycles, a steady push toward net-zero by 2050, and clearer efficiency signals from the 2021 A to G energy label rescaling that simplify consumer choice and sharpen product differentiation. The Clean Heat Market Mechanism, Boiler Upgrade Scheme grants, and consultations to raise standards for tumble dryers align efficiency with policy objectives, while right-to-repair measures and expanded spare parts access may extend replacement intervals and temper volumes at the margin. Channel dynamics remain in transition, with multi-brand stores holding a sizable share today, while online channels post the fastest gains on the back of better tools, logistics options, and greater convenience for younger cohorts.

United Kingdom Home Appliances Market Trends and Insights

Energy Label Rescaling and UK Ecodesign Standards Accelerate A-Rated Replacements From 2026

Across Europe, consumers are highly aware of energy labels and often use them as a key factor in purchasing decisions. This trend has supported the popularity of A-rated refrigerators and washing machines, especially after price caps highlighted significant lifetime savings in 2025 and 2026. With Ofgem setting its dual-fuel price cap at GBP 1758 (USD 2,371.7), retailers are increasingly emphasizing kilowatt-hour consumption, both in-store and online, to present a clearer picture of the total cost of ownership relative to the upfront price. Northern Ireland's regulatory alignment through the Windsor Framework enables manufacturers to adopt dual-compliance strategies that cater seamlessly to both Great Britain and Northern Ireland. This alignment simplifies product planning and labeling processes. In July 2025, the United Kingdom proposed new requirements for tumble dryers, aiming to phase out inefficient models, introduce repairability indices, and tighten standards for condensation efficiency and low-power modes. These measures establish a compliance baseline that benefits heat-pump dryers. In response, brands are expanding heat-pump dryer offerings and providing extended warranties, emphasizing the link between efficiency and post-sale support. This strategy reduces payback periods for consumers willing to invest more upfront. NIQ GfK data show smart A-rated washing machines up 38% in unit sales (August 2023-July 2024), accounting for over 50% of all machines sold, while Beko's Which? Best Value Appliance Brand award for 2024 and 2025 underscores competitive intensity at the efficiency frontier.

Smart/Connected Appliances Adoption And Interoperability Ecosystems Mature In UK Homes

Broadband upgrades and smart meter rollout underpin a wave of connected appliances that can automate energy use and coordinate with time-of-use tariffs. National Grid ESO's Demand Flexibility Service became a year-round program and demonstrated that households will shift appliance usage during peak events when compensated, which validates the value proposition for scheduleable devices. Partnerships between appliance makers and energy suppliers, such as Haier with Octopus Energy, show how low off-peak prices can help recover device premiums through optimized cycles and smart scheduling. September 2025, refrigerators, washers, dryers, air conditioners with seven years of software updates, Knox Matrix security, and enhanced AI Vision Inside, elevate interoperability expectations beyond single-brand ecosystems, while LG's AI Core-Tech in MoodUP(TM) fridge-freezers and Bespoke AI Jet Ultra vacuums showcase machine-learning optimization of cooling curves and suction profiles.

Cost-of-Living Squeeze Defers Discretionary Upgrades And Compresses Volumes

Inflation remained above the Bank of England's target into late 2025, and real wage gains were modest into early 2026, which kept budgets tight for many households. Ofgem's energy price cap at GBP 1,758 (USD 2,371.7) in early 2026 reinforced household sensitivity to energy bills, and many buyers continued to delay non-essential upgrades until failure rather than replacing a still-functional unit. Retail pricing in some categories softened in 2025 as retailers absorbed deflation and used promotions to stimulate demand, which compressed gross margins in the process. Entry-tier volumes held better as consumers prioritized essential items and lower upfront prices, while premium buyers in affluent areas remained active on value, longevity, and design integration. Financing options and subscriptions helped lower barriers to higher-efficiency dryers and connected washers, though energy bill pressures still limited uptake among price-sensitive cohorts. This environment narrows the near-term growth runway for the United Kingdom home appliances market, yet it also elevates the pitch for efficient and smart products that can clearly document bill savings over time.

Other drivers and restraints analyzed in the detailed report include:

- Electrification Of Heating And Kitchen Retrofits Boosts Demand For Energy-Efficient White Goods

- Premiumisation Trend Lifts Average Selling Prices Through Design-Led And Feature-Rich Models

- Housing Slowdown And Fewer New Completions Weigh On Built-In Installations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerators accounted for 24.78% of the United Kingdom home appliances market in 2025, driven by mandatory placement, long service lives, and energy visibility, which sustained high replacement intent, supporting premium models that meet stricter efficiency standards. Flagship launches include Liebherr's Energy Class A integrated models, LG's InstaView configurations with app controls and precise temperature stability, and Samsung's Family Hub with vision-based food recognition, which sustain average selling prices through a clear feature and efficiency case. A-rated refrigeration and laundry now stand out under the rescaled A to G label, and retailers emphasize kilowatt-hours and total cost of ownership in-store and online. Tumble dryers are shifting to heat-pump architectures to meet proposed standards and repairability requirements, which link energy savings with longer warranties and better diagnostics. The United Kingdom home appliances market benefits when brands position warranties, service networks, and software updates as part of the overall value proposition across refrigeration, laundry, and cooking.

Air fryers are forecast to expand at a 3.51% CAGR through 2031 as healthier cooking, smaller footprints, and efficient operation align with hybrid work patterns and price-sensitive meal preparation. Multifunctional devices from Ninja, Instant Brands, and Tefal combine multiple cooking modes into single countertop appliances, which increases appeal among urban households with limited kitchen space and busy routines. In major appliances, washing machines and dishwashers integrate auto-dosing, soil sensing, and cycle optimization, which reduce resource use without sacrificing performance. Beko's platform highlights algorithms to reduce energy use and enhance garment care across programs beyond eco modes, pointing to iterative efficiency gains in mainstream price bands. Ovens and hobs are adding AI-assisted presets and induction for better control, speed, and safety, which pairs well with time-of-use tariffs and smart meter participation in flexibility events. Robotic and cordless vacuums continue to split the cleaning category as automation and higher suction at lighter weights show up in premium launches.

The United Kingdom Home Appliances Market is Segmented by Product (Major Home Appliances and Small Home Appliances), Distribution Channel (Multi-Brand Stores, Exclusive Brand Outlets, and More), and Geography (England, Scotland, Wales, Northern Ireland). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Beko (Arcelik)

- Bosch

- Siemens

- Neff

- Haier

- Samsung Electronics UK

- LG Electronics UK

- Miele GB

- Electrolux Group (AEG)

- Zanussi (Electrolux Group)

- Hisense UK

- Smeg UK

- Glen Dimplex Home Appliances

- Rangemaster (AGA Rangemaster)

- Dyson

- SharkNinja (Ninja, Shark)

- Groupe SEB (Tefal, Rowenta, Krups)

- Versuni (Philips Domestic Appliances)

- De'Longhi UK (incl. Kenwood)

- Russell Hobbs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy label rescaling and UK ecodesign standards accelerate A-rated replacements from 2026

- 4.2.2 Smart/connected appliances adoption and interoperability ecosystems mature in UK homes

- 4.2.3 Electrification of heating and kitchen retrofits boosts demand for energy-efficient white goods

- 4.2.4 Premiumisation trend lifts average selling prices through design-led and feature-rich models

- 4.2.5 Demand flexibility services and time-of-use tariffs favor scheduleable smart appliances

- 4.2.6 Private-label growth at entry-tier reshapes OEM opportunities and price architecture

- 4.3 Market Restraints

- 4.3.1 Cost-of-living squeeze defers discretionary upgrades and compresses volumes

- 4.3.2 Rising repair, logistics and compliance costs pressure margins across manufacturers and retailers

- 4.3.3 Housing slowdown and fewer new completions weigh on built-in installations

- 4.3.4 New import controls and border checks increase lead times and costs for imports

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Major Home Appliances

- 5.1.1.1 Refrigerators

- 5.1.1.2 Freezers

- 5.1.1.3 Washing Machines

- 5.1.1.4 Dishwashers

- 5.1.1.5 Ovens (Incl. Combi & Microwave)

- 5.1.1.6 Air Conditioners

- 5.1.1.7 Other Major Home Appliances

- 5.1.2 Small Home Appliances

- 5.1.2.1 Coffee Makers

- 5.1.2.2 Food Processors

- 5.1.2.3 Grills & Roasters

- 5.1.2.4 Electric Kettles

- 5.1.2.5 Juicers & Blenders

- 5.1.2.6 Air Fryers

- 5.1.2.7 Vacuum Cleaners

- 5.1.2.8 Electric Rice Cookers

- 5.1.2.9 Toasters

- 5.1.2.10 Counter-top Ovens

- 5.1.2.11 Other Small Home Appliances

- 5.1.1 Major Home Appliances

- 5.2 By Distribution Channel

- 5.2.1 Multi-Brand Stores

- 5.2.2 Exclusive Brand Outlets

- 5.2.3 Online

- 5.2.4 Other Distribution Channels

- 5.3 By Geography

- 5.3.1 England

- 5.3.2 Scotland

- 5.3.3 Wales

- 5.3.4 Northern Ireland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Beko (Arcelik)

- 6.4.2 Bosch

- 6.4.3 Siemens

- 6.4.4 Neff

- 6.4.5 Haier

- 6.4.6 Samsung Electronics UK

- 6.4.7 LG Electronics UK

- 6.4.8 Miele GB

- 6.4.9 Electrolux Group (AEG)

- 6.4.10 Zanussi (Electrolux Group)

- 6.4.11 Hisense UK

- 6.4.12 Smeg UK

- 6.4.13 Glen Dimplex Home Appliances

- 6.4.14 Rangemaster (AGA Rangemaster)

- 6.4.15 Dyson

- 6.4.16 SharkNinja (Ninja, Shark)

- 6.4.17 Groupe SEB (Tefal, Rowenta, Krups)

- 6.4.18 Versuni (Philips Domestic Appliances)

- 6.4.19 De'Longhi UK (incl. Kenwood)

- 6.4.20 Russell Hobbs

7 Market Opportunities & Future Outlook

- 7.1 Expansion of heat-pump dryers and low-carbon appliances aligned with net-zero 2050 targets

- 7.2 Integration of appliances into home energy management systems, enabling grid participation and recurring service revenues