PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061573

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061573

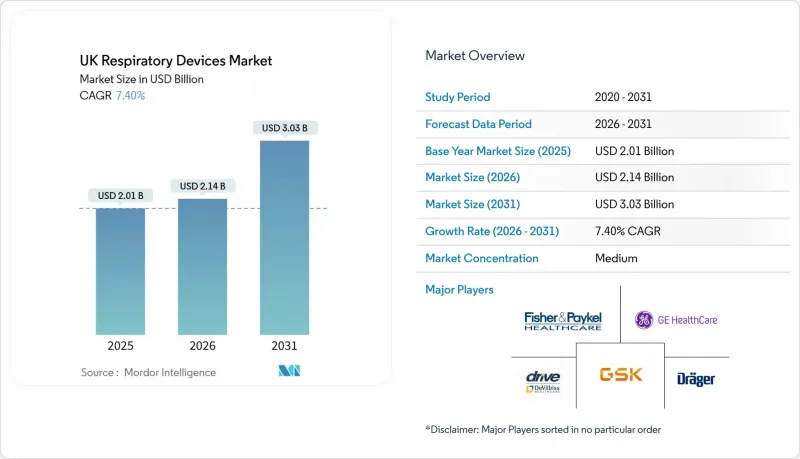

UK Respiratory Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the uK respiratory devices market size is projected to be USD 2.01 billion in 2025, USD 2.14 billion in 2026, and reach USD 3.03 billion by 2031, growing at a CAGR of 7.40% from 2026 to 2031.

This report is Segmented by Type (Diagnostic and Monitoring Devices, Therapeutic Devices, and Disposables), End-User (Hospitals & Clinics, Home Healthcare Settings, and More), Disease Indication (COPD, Asthma, and More), and Age Group (Adult, Geriatric, Pediatric). The Market Forecasts are Provided in Terms of Value (USD).

UK Respiratory Devices Market Trends and Insights

Rising Prevalence of COPD, Asthma & Sleep Apnea

Chronic respiratory conditions now affect about 12 million UK residents, raising emergency admissions for asthma by 17% in the financial year ending 2024. The prevalence of sleep apnea is around 8% among adults. Yet, underdiagnosis keeps a wide care gap, which home sleep-testing devices approved by the National Institute for Health and Care Excellence (NICE) in 2024 are beginning to close. Obesity reached 29% of adults in 2025, further boosting demand for continuous positive airway pressure (CPAP) and bilevel positive airway pressure (BiPAP). New biologics such as GSK's Nucala reduce severe-asthma flare-ups but still require rescue inhalers and nebulizers, sustaining equipment volumes. Together, these epidemiological trends lift the UK respiratory devices market by expanding both therapeutic and monitoring use cases.

Ageing Population & Co-Morbidities

Citizens aged 65 and older climbed to 12.9 million in 2025, and COPD prevalence in this group is four times that of younger adults. Two-thirds of individuals over 75 live with multiple chronic illnesses, which pushes clinicians to favor platforms that monitor oxygen saturation, heart rate, and respiration in one unit. Frailty screenings now routinely include spirometry, broadening the diagnostic installed base beyond pulmonology departments. Higher co-morbidity also lengthens therapy duration, lifting recurring sales of disposables. These demographic realities reinforce long-run demand in the UK respiratory devices market.

High Device Cost & NHS Budget Limits

The 2025-2026 NHS allocation of GBP 165 billion held capital budgets flat amid inflation, curbing new-equipment outlays. BiPAP units range from GBP 1,200-2,500 (USD 1,639 -3,414), while portable concentrators cost up to GBP 3,500 (USD 4,780), stretching trust finances. Home oxygen reimbursement has not changed since 2018, dimming suppliers' incentive to refresh fleets. Scotland's 2025 tender rewarded the lowest total cost of ownership, favoring makers that bundle maintenance. Private CPAP purchases average GBP 800 and remain out of reach for many undiagnosed apnea patients.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances & Home-Care Shift

- NHS Low-Carbon-Inhaler Initiative

- MHRA Post-Brexit Regulatory Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic models captured 58.10% of the UK respiratory devices market share in 2025 as CPAP, BiPAP, and concentrators remain integral to chronic-care pathways. Continuous-positive-airway-pressure equipment benefited from NICE-endorsed home testing, which cut wait times from 22 to 8 weeks, creating a brisk referral flow. BiPAP devices saw higher uptake in virtual wards where clinicians remotely adjust settings via cloud dashboards, improving adherence and reducing readmissions. Nebulizers remain relevant for acute flares and pediatric asthma, with PARI's eFlow delivering treatments in under 3 minutes. Oxygen concentrators serve roughly 150,000 long-term patients, yet stagnant reimbursement hampers fleet modernization.

Disposable masks, circuits, and filters posted an 8.80% annual growth rate, the fastest within this segmentation, encouraged by strict infection-prevention guidelines. Pulse oximeters, widely distributed during the pandemic, now face a replacement cycle that favors Bluetooth-enabled models with trend analytics. Fisher & Paykel's Evora nasal mask shows how incremental ergonomic tweaks sustain premium positioning. High-priced ventilators from Drager and Hamilton remain essential in intensive care, although volumes are smaller than for sleep-apnea and COPD hardware.

Hospitals and clinics accounted for 60.04% of revenue in 2025, yet home-health sites are expanding by 10.40% annually as the NHS diverts chronic follow-up to community settings. Virtual wards enrolled 50,000 respiratory patients in 2025, using pulse oximeters and capnographs to monitor daily vitals. ResMed's myAir platform reduced the average length of stay by 3 days in pilot trusts, freeing acute beds for surgical cases. Ambulatory surgery centers increasingly rely on portable spirometers for pre-op risk stratification in patients aged 60 and older, as advised by NICE.

Home-health momentum in the UK respiratory devices market reflects gains in portability: concentrators with eight-hour batteries enable work and travel, while smart-inhaler data integrate with electronic records to auto-alert clinicians. Hospitals still dominate invasive ventilation and complex diagnostics, such as bronchoscopy. Ambulatory centers, which performed 1.2 million procedures in 2024, adopted end-tidal CO2 monitoring following an MHRA safety alert. Long-term care facilities are now adopting handheld spirometers so staff can conduct on-site lung function screening.

List of Companies Covered in this Report:

- Becton, Dickinson and Company (CareFusion)

- Chart Industries (AirSep)

- Drive DeVilbiss Healthcare

- Dragerwerk

- Fisher & Paykel Healthcare

- GE Healthcare

- GlaxoSmithKline

- Hamilton Medical

- Honeywell International

- Intersurgical

- Invacare

- Koninklijke Philips

- Masimo

- Medtronic

- NDD Medical Technologies

- OMRON Healthcare Co. Ltd

- PARI Medical Ltd

- Resmed

- Smiths Group

- Vitalograph

- Vyaire Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of COPD, Asthma & Sleep Apnea

- 4.2.2 Ageing Population & Co-Morbidities

- 4.2.3 Technological Advances & Home-Care Shift

- 4.2.4 NHS Low-Carbon-Inhaler Initiative

- 4.2.5 AI-Enabled Diagnostics in UK Primary Care

- 4.2.6 Decentralised Clinical-Trial Adoption of Connected Spirometry

- 4.3 Market Restraints

- 4.3.1 High Device Cost & NHS Budget Limits

- 4.3.2 MHRA Post-Brexit Regulatory Hurdles

- 4.3.3 Sustainability Phase-Out of High-Propellant MDIs

- 4.3.4 Semiconductor-Sensor Supply Fragility

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 Spirometers

- 5.1.1.2 Sleep Test Devices

- 5.1.1.3 Peak Flow Meters

- 5.1.1.4 Pulse Oximeters

- 5.1.1.5 Capnographs

- 5.1.1.6 Other Diagnostic & Monitoring

- 5.1.2 Therapeutic Devices

- 5.1.2.1 CPAP Devices

- 5.1.2.2 BiPAP Devices

- 5.1.2.3 Humidifiers

- 5.1.2.4 Nebulizers

- 5.1.2.5 Oxygen Concentrators

- 5.1.2.6 Ventilators

- 5.1.2.7 Inhalers

- 5.1.2.8 Other Therapeutic Devices

- 5.1.3 Disposables

- 5.1.3.1 Masks

- 5.1.3.2 Breathing Circuits

- 5.1.3.3 Other Disposables

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By End-User

- 5.2.1 Hospitals & Clinics

- 5.2.2 Home Healthcare Settings

- 5.2.3 Ambulatory Surgical Centers

- 5.2.4 Others

- 5.3 By Disease Indication

- 5.3.1 COPD

- 5.3.2 Asthma

- 5.3.3 Sleep Apnea

- 5.3.4 Pneumonia & Acute Respiratory Infections

- 5.3.5 Others

- 5.4 By Age

- 5.4.1 Adult

- 5.4.2 Geriatric

- 5.4.3 Pediatric

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Becton, Dickinson and Company (CareFusion)

- 6.3.2 Chart Industries (AirSep)

- 6.3.3 DeVilbiss Healthcare LLC

- 6.3.4 Dragerwerk AG & Co. KGaA

- 6.3.5 Fisher & Paykel Healthcare Ltd

- 6.3.6 GE Healthcare

- 6.3.7 GlaxoSmithKline plc

- 6.3.8 Hamilton Medical AG

- 6.3.9 Honeywell International Inc.

- 6.3.10 Intersurgical Ltd

- 6.3.11 Invacare Corporation

- 6.3.12 Koninklijke Philips NV

- 6.3.13 Masimo Corporation

- 6.3.14 Medtronic plc

- 6.3.15 NDD Medical Technologies

- 6.3.16 OMRON Healthcare Co. Ltd

- 6.3.17 PARI Medical Ltd

- 6.3.18 ResMed Inc.

- 6.3.19 Smiths Medical (ICU Medical)

- 6.3.20 Vitalograph Ltd

- 6.3.21 Vyaire Medical Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment