PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061588

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061588

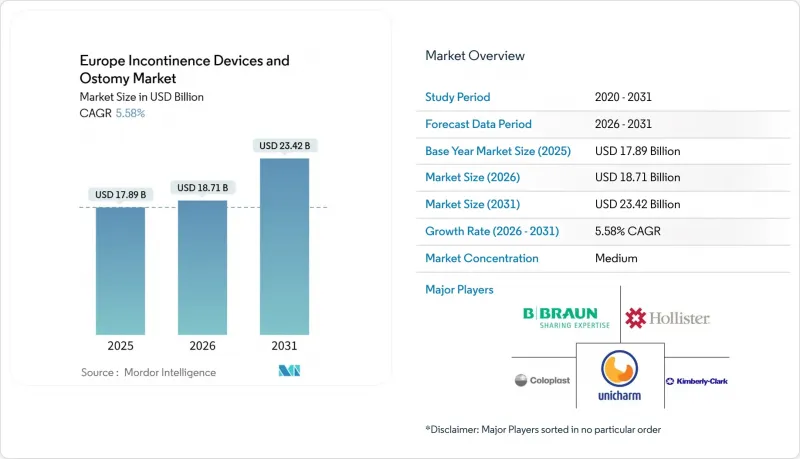

Europe Incontinence Devices And Ostomy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe incontinence devices and ostomy market size was valued at USD 17.89 billion in 2025 and is estimated to grow from USD 18.71 billion in 2026 to reach USD 23.42 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

This report is Segmented by Product Type (Incontinence Care Products and Ostomy Care Products), Application (Bladder Cancer, and More), End-User (Hospitals and More), by Distribution Channel (Institutional Tender Procurement and More), by Technology / System (Disposable Products and More), and Geography (Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Incontinence Devices And Ostomy Market Trends and Insights

Rising Geriatric and Obese Population

Europe has the world's oldest regional median age, and 34% of citizens aged 65+ report urge or stress incontinence episodes every week. Obesity prevalence passes 22% in Germany and the United Kingdom, and excess abdominal pressure accelerates pelvic-floor weakening that triggers leakage. Urologists prescribe single-use catheters and pads to prevent recurrent urinary tract infections, driving bulk demand in outpatient clinics. Parallel gerontology guidelines recommend early adoption of bowel management pouches for seniors recovering from colorectal surgery, as they can increase ostomy bag volume. As life expectancy stretches to 83 years in Spain, years lived with chronic conditions and disability continue to rise, strengthening the customer base for the European incontinence devices and ostomy market.

Increasing Prevalence of Renal & Urological Disorders

Type 2 diabetes and hypertension increase chronic kidney disease incidence, which now affects 10% of adults in northern Europe. Hemodialysis patients often require intermittent catheterization and high-output urostomy pouches to manage fluid balance between sessions. National health funds reimburse closed-end drainage bags that allow secure night-time urine collection, expanding recurring unit sales. Awareness programs by urological associations encourage primary-care physicians to screen for neurogenic bladder after stroke and channel referrals to specialized continence centers. Device makers partner with dialysis clinics to bundle ostomy accessories with weekly treatment packs, thereby increasing product penetration among end-stage renal disease patients.

Complications & Peristomal Skin Issues with Long-Term Use

Nearly 35% of ostomates experience dermatitis or mucocutaneous separation in the first year post-surgery, raising readmission risk. Chronic leakage corrodes confidence in one-piece bags, fostering hesitation among new patients. Negative experiences circulate on patient forums, lengthening adoption curves in direct-to-consumer channels. Providers must invest in extra nursing hours and hydrocolloid dressing kits, inflating episode-of-care costs for insurers, such as quality-of-life concerns, tempering the rapid expansion of the European incontinence devices and ostomy market.

Other drivers and restraints analyzed in the detailed report include:

- Higher Incidence of Colorectal & Bladder Cancer

- Strong Reimbursement for Chronic Care in Western Europe

- Reimbursement Gaps in Eastern & Southern Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, incontinence care products captured 66.56% of the Europe incontinence devices and ostomy market, supported by large-volume contracts for adult diapers, pads, and intermittent catheters in public hospitals. The prevalence of urge and overflow incontinence among seniors drives procurement toward absorbent underpads that meet EU tensile-strength and biodegradability criteria. Manufacturers leverage plant-based fluff pulp and SAP blends to meet eco-label thresholds without compromising absorbency. The Europe incontinence devices and ostomy market size for disposable pads is now forecast to grow at an 8.80% CAGR through 2031 as aging households and nursing homes prioritize leak-proof nightwear.

Ostomy care products, while smaller in share, exhibit premium ASPs thanks to convexity technology and charcoal-infused filters that curb odor. Two-piece drainable systems are gaining favor among high-output ileostomy patients because barrier rings can prolong wear time up to 7 days. Skin-friendly hydrocolloid wafers with ceramide additives reduce peristomal dermatitis incidence by 21%, boosting switching momentum away from legacy PVC pouches. Vendors invest in pediatric pouches with cartoon imagery, a fast-growing micro-segment as survivorship improves in childhood Hirschsprung disease.

Colorectal cancer surgeries accounted for 34.55% of regional revenue in 2025, and the Europe incontinence devices and ostomy market size associated with these procedures is slated for a 7.20% CAGR during 2026-2031. Enhanced screening uptake via FIT tests boosts early detection, yet surgery rates remain high, sustaining stoma creation volumes. Fast-track recovery protocols mandate low-profile silicone baseplates, accelerating pull-through of one-piece bags.

Spinal cord injury and neurogenic bladder segments record steady growth as urban mobility accidents persist. Urostomy pouches with anti-reflux valves prevent ascending infections in paraplegic patients. Benign prostatic hyperplasia cases treated via trans-urethral resection continue to prescribe indwelling Foley catheters post-operatively, although intermittent self-catheterization programs lower infection risk and cut inpatient stay lengths.

List of Companies Covered in this Report:

- Abena A/S

- Alcare

- Atlantic Therapeutics Group

- Attindas Hygiene Partners

- Axonics Inc.

- B. Braun

- Becton Dickinson & Co. (BD)

- Boston Scientific

- Coloplast

- Convatec

- Essity AB (TENA)

- Hollister

- Johnson & Johnson Services, Inc. (Ethicon)

- Kimberly-Clark Worldwide

- Marlen Manufacturing

- Medtronic

- Ontex Group NV

- Hartmann Group

- Salts Healthcare

- Teleflex

- Unicharm

- Welland Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Geriatric and Obese Population

- 4.2.2 Increasing Prevalence of Renal & Urological Disorders

- 4.2.3 Higher Incidence of Colorectal & Bladder Cancer

- 4.2.4 Strong Reimbursement for Chronic Care in Western Europe

- 4.2.5 Shift Toward Tele-Urology & Remote Continence Monitoring

- 4.2.6 EU Circular Economy Pressure Spurring Eco-Friendly Disposables

- 4.3 Market Restraints

- 4.3.1 Complications & Peristomal Skin Issues with Long-Term Use

- 4.3.2 Reimbursement Gaps in Eastern & Southern Europe

- 4.3.3 High Lifetime Cost of Advanced Ostomy Supplies

- 4.3.4 MDR Post-Market Surveillance Raising Compliance Costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Incontinence Care Products

- 5.1.1.1 Absorbent Pads & Underpads

- 5.1.1.2 Intermittent Catheters

- 5.1.1.3 Incontince Bags

- 5.1.1.4 Pelvic-Floor Stimulation & Neuromodulation Devices

- 5.1.2 Ostomy Care Products

- 5.1.2.1 Ostomy Bags

- 5.1.2.1.1 One-piece Systems

- 5.1.2.1.2 Two-piece Systems

- 5.1.2.1.3 Drainable vs Closed-end

- 5.1.2.1.4 High-output & Pediatric Pouches

- 5.1.2.2 Skin Barriers & Seals

- 5.1.2.3 Irrigation & Accessories

- 5.1.2.4 Others

- 5.1.2.1 Ostomy Bags

- 5.1.1 Incontinence Care Products

- 5.2 By Application

- 5.2.1 Bladder Cancer

- 5.2.2 Colorectal Cancer

- 5.2.3 Crohns & Ulcerative Colitis

- 5.2.4 Benign Prostatic Hyperplasia / Post-Prostatectomy

- 5.2.5 Spinal Cord Injury & Neurogenic Bladder

- 5.2.6 Kidney Stone & Chronic Kidney Failure

- 5.2.7 Others

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home-Care Settings

- 5.3.4 Long-term Care & Nursing Homes

- 5.3.5 Others

- 5.4 By Distribution Channel

- 5.4.1 Institutional Tender Procurement

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies & Subscription Services

- 5.5 By Technology / System

- 5.5.1 Disposable Products

- 5.5.2 Reusable / Eco-friendly Products

- 5.5.3 Smart / Connected Continence & Ostomy Devices

- 5.6 By Region

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abena A/S

- 6.3.2 ALCARE Co. Ltd

- 6.3.3 Atlantic Therapeutics Group

- 6.3.4 Attindas Hygiene Partners

- 6.3.5 Axonics Inc.

- 6.3.6 B. Braun SE

- 6.3.7 Becton Dickinson & Co. (BD)

- 6.3.8 Boston Scientific Corporation

- 6.3.9 Coloplast A/S

- 6.3.10 ConvaTec Group Plc

- 6.3.11 Essity AB (TENA)

- 6.3.12 Hollister Incorporated

- 6.3.13 Johnson & Johnson Services, Inc. (Ethicon)

- 6.3.14 Kimberly-Clark Corporation

- 6.3.15 Marlen Manufacturing & Development

- 6.3.16 Medtronic plc

- 6.3.17 Ontex Group NV

- 6.3.18 Paul Hartmann AG

- 6.3.19 Salts Healthcare Ltd

- 6.3.20 Teleflex Incorporated

- 6.3.21 Unicharm Corporation

- 6.3.22 Welland Medical Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment