PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061603

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061603

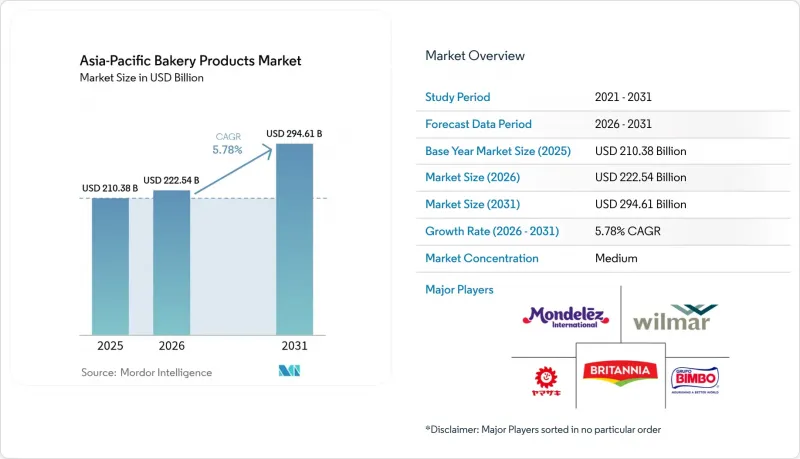

Asia-Pacific Bakery Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia pacific bakery products market size was valued at USD 210.38 billion in 2025 and estimated to grow from USD 222.54 billion in 2026 to reach USD 294.61 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031).

This report is Segmented by Product Type (Bread, Cakes and Pastries, Biscuits and Cookies, and More), Category (Conventional, Free From), Form (Fresh, Frozen), Distribution Channel (Foodservice/HORECA, Retail/Off Trade), and Geography (China, Japan, India, Australia, South Korea, Indonesia, Thailand, Malaysia, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia-Pacific Bakery Products Market Trends and Insights

Convenience-driven snacking boom

In bustling megacities, the demand for portable bakery items has surged, with many now serving as convenient meal replacements. With commuters often dedicating over 90 minutes daily to transit, there's a growing preference for on-the-go options like single-serve cakes, filled buns, and nutrient-rich breads that are easy to consume while traveling. Japan boasts a vast network of over 56,000 convenience stores, each rotating freshly baked goods multiple times a day to ensure optimal softness and aroma, catering to the fast-paced lifestyle of urban consumers. Meanwhile, in China, store operators have introduced on-site ovens, catering to shoppers' desires for warm, freshly baked items at any time of the day or night, enhancing the overall shopping experience. Recognizing the preferences of female professionals aged 26-40, brands are adopting portion-controlled packaging that balances calorie management with flavor diversity, addressing both health-conscious and taste-driven needs. Furthermore, to enhance energy sustenance and meet the nutritional demands of busy consumers, brands are infusing their offerings with slow-release carbohydrates and plant proteins, ensuring each serving provides long-lasting energy and satiety.

E-commerce acceleration for baked goods

Contributing a quarter of the world's digitally deliverable services, the region has developed platforms capable of managing temperature-sensitive orders, enabling the seamless delivery of perishable goods. Insulated "last-mile" carriers ensure that artisanal sourdough loaves, gluten-free muffins, and exclusive pastries arrive fresh at distant homes, maintaining product quality and customer satisfaction. Subscription models for weekly bread baskets not only generate recurring revenue but also enhance demand forecasting by providing businesses with consistent data on consumer preferences and purchasing patterns. Through cross-border channels, Taiwanese pineapple cakes and Japanese chiffon rolls are gaining popularity among fans in Malaysia, all without the need for physical storefronts, thereby reducing overhead costs and expanding their market reach. AI-driven search tools, by recommending products based on previous purchases, are boosting basket values and personalizing the shopping experience for consumers. However, achieving profitable scaling hinges on the presence of dense urban clusters, where the costs of same-day delivery remain feasible, ensuring operational efficiency and cost-effectiveness.

Volatile wheat and dairy input prices

Throughout 2024, wholesale wheat prices remained steady between INR 31,500 and 34,300 per tonne, squeezing the gross margins of branded breads and cookies. Concurrent surges in milk powder and butter prices have driven up costs for laminated dough. This situation has left producers with two choices: either raise list prices, which could risk losing price-sensitive customers, or reduce product weights, potentially impacting consumer perception of value. Economies reliant on imports, like Indonesia, face heightened vulnerabilities, sourcing over half of their wheat from abroad and consequently feeling the brunt of freight and currency fluctuations. These challenges are further exacerbated by global supply chain disruptions and geopolitical tensions, which add to the unpredictability of costs. To mitigate risks, larger buyers often turn to annual contracts, locking in prices to avoid volatility, or explore alternative grains, such as sorghum, to diversify their supply base. In contrast, smaller bakeries, without the leverage of scale, are either putting a hold on low-margin SKUs or postponing their innovation efforts, waiting for a return to stability in raw material prices. This delay in innovation could hinder their ability to compete in an already challenging market environment.

Other drivers and restraints analyzed in the detailed report include:

- Health-oriented product reformulation

- Expansion of in-store supermarket bakeries

- Stricter trans-fat regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, biscuits and cookies dominated the Asia Pacific bakery products market, capturing 38.02% of total sales. Their leading position stems from their long shelf life, convenience, and widespread flavor appeal among diverse consumers. Moreover, aggressive promotional pricing by both regional and international brands has bolstered their accessibility, particularly in cost-sensitive markets. Rural consumers, drawn to the affordability of multipack formats, have shown a consistent preference for traditional sweet biscuits, benefiting from their deep penetration in general trade channels. This category's resilience spans both premium and value ranges, granting it an edge over other bakery formats. Consequently, biscuits and cookies have solidified their status as a household staple, retaining significance in contemporary retail settings.

Conversely, cakes and pastries are set to experience the swiftest growth, boasting an impressive CAGR of 6.53% during the forecast period. Younger consumers increasingly perceive dessert-style bakery items as social symbols, especially during holidays, cafe visits, and celebrations, driving premium demand. In China, the cake segment alone exceeded USD 3 billion, with specialty shops proudly displaying hand-decorated sponges and creamy rolls, underscoring the artistry involved. Coastal cities, witnessing a shift in traditional breakfast habits due to an evolving cafe culture, have embraced Western delights like croissants and cruffins. This artisan approach fuels revenue, with patisserie houses marketing limited-batch entremets at prices two to three times higher than packaged counterparts. Beyond mere indulgence, the surge in digital food tutorials is encouraging home cooks to experiment with layered desserts, subsequently driving demand for essential ingredients like flour, butter, and yeast. This blend of experiential value, premium branding, and youthful enthusiasm positions the category for swift growth throughout the Asia Pacific region.

In 2025, conventional bakery SKUs commanded a dominant 92.74% share of the total turnover in the Asia Pacific market. Their widespread appeal, rooted in wheat-based, sweetened formulations, resonates with mass-market preferences. This not only underscores their popularity but also enables manufacturers to harness economies of scale. The enduring success of these products can be attributed to their familiarity, affordability, and efficient distribution channels, spanning both modern and traditional retail outlets. For consumers, whether in rural areas or mainstream urban centers, conventional baked goods are a staple, woven into the fabric of daily life. This strong foothold not only ensures consistent volume but also provides stability to companies, even amidst fluctuations in premium or niche formats. While health-focused alternatives are on the rise, conventional bakery items continue to thrive, serving the region's largest consumer base.

Free-from bakery goods, including gluten-free, sugar-free, and allergen-light varieties, are poised for the most significant growth, with a projected CAGR of 7.41%. Urban consumers, becoming increasingly discerning, are driving this demand, often seeking specific claims such as "no maltodextrin" and "zero lactose." Supermarkets, responding to this heightened interest, are dedicating more shelf and end-cap space to these specialized items. Countries like Australia and Singapore are seeing particularly strong traction, driven by increased awareness of celiac disease and broader wellness initiatives. In response, manufacturers are investing in allergen-segregated production lines, ensuring food safety and capitalizing on premium pricing that often exceeds conventional offerings by over 30%. Research into functional ingredient substitutions, such as apple puree, inulin, and stevia, allows manufacturers to cut sugar content while preserving sensory qualities, though these formulation challenges demand substantial research and development investment. Ingredient suppliers play a crucial role, introducing innovations like resistant starches, inulin, and natural sweeteners, ensuring health claims don't compromise texture and taste. Industry moves, like Grupo Bimbo's acquisition of a gluten-free specialty baker, highlight the segment's long-term promise, supported by a loyal consumer base that views these "free-from" options as essential health solutions rather than mere indulgences.

List of Companies Covered in this Report:

- Britannia Industries Ltd.

- Mondelez International Inc.

- Parle Products Pvt. Ltd.

- Wilmar Intl. Ltd. (Goodman Fielder)

- QAF Ltd. (Gardenia)

- Meiji Holdings Co. Ltd.

- President Bakery PLC

- Grupo Bimbo SAB de CV

- ITC Ltd.

- Bonn Group

- Yamazaki Baking Co. Ltd.

- Shikishima Baking Co. Ltd.

- Aryzta AG

- Lotte Confectionery (Co-Pang)

- Finsbury Food Group Plc

- Garden Pia Co. Ltd.

- Mankattan Food Co. Ltd.

- Yamazaki Nippon Food

- BreadTalk Group Ltd.

- SPC Samlip Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Convenience-driven snacking boom

- 4.2.2 E-commerce acceleration for baked goods

- 4.2.3 Health-oriented product reformulation

- 4.2.4 Expansion of in-store supermarket bakeries

- 4.2.5 Functional-fiber fortification initiatives

- 4.2.6 Sustainable packaging mandates

- 4.3 Market Restraints

- 4.3.1 Volatile wheat and dairy input prices

- 4.3.2 Sugar-tax ripple effects in ASEAN

- 4.3.3 Stricter trans-fat regulations (e.g., India FSSAI)

- 4.3.4 Supply-chain bottlenecks for frozen logistics

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE and VOLUME)

- 5.1 By Product Type

- 5.1.1 Bread

- 5.1.2 Cakes and Pastries

- 5.1.3 Biscuits and Cookies

- 5.1.4 Morning Goods (Muffins, Doughnuts, Croissants)

- 5.1.5 Others

- 5.2 Category

- 5.2.1 Conventional

- 5.2.2 Free From

- 5.3 Form

- 5.3.1 Fresh

- 5.3.2 Frozen

- 5.4 Distribution Channel

- 5.4.1 Foodservice/HORECA

- 5.4.2 Retail\Off Trade

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Convenience Stores

- 5.4.2.3 Specialist Bakeries

- 5.4.2.4 Online Retail Retails

- 5.4.2.5 Others

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 Indonesia

- 5.5.7 Thailand

- 5.5.8 Malaysia

- 5.5.9 Philippines

- 5.5.10 Vietnam

- 5.5.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Britannia Industries Ltd.

- 6.4.2 Mondelez International Inc.

- 6.4.3 Parle Products Pvt. Ltd.

- 6.4.4 Wilmar Intl. Ltd. (Goodman Fielder)

- 6.4.5 QAF Ltd. (Gardenia)

- 6.4.6 Meiji Holdings Co. Ltd.

- 6.4.7 President Bakery PLC

- 6.4.8 Grupo Bimbo SAB de CV

- 6.4.9 ITC Ltd.

- 6.4.10 Bonn Group

- 6.4.11 Yamazaki Baking Co. Ltd.

- 6.4.12 Shikishima Baking Co. Ltd.

- 6.4.13 Aryzta AG

- 6.4.14 Lotte Confectionery (Co-Pang)

- 6.4.15 Finsbury Food Group Plc

- 6.4.16 Garden Pia Co. Ltd.

- 6.4.17 Mankattan Food Co. Ltd.

- 6.4.18 Yamazaki Nippon Food

- 6.4.19 BreadTalk Group Ltd.

- 6.4.20 SPC Samlip Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK