PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061604

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061604

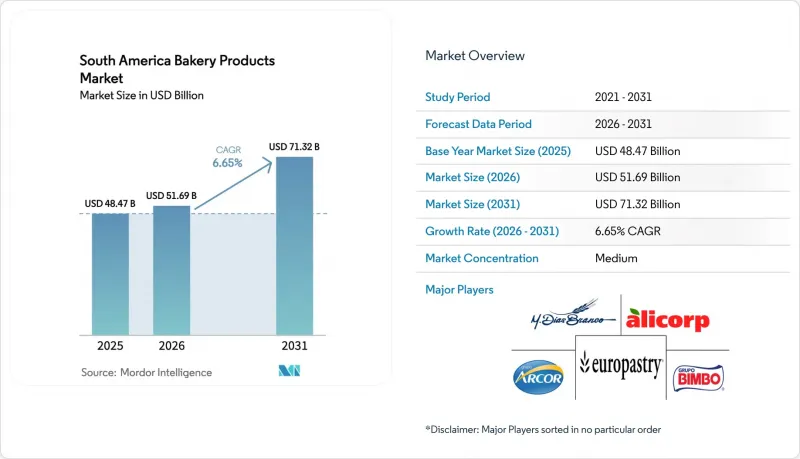

South America Bakery Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america bakery products market size was valued at USD 48.47 billion in 2025 and estimated to grow from USD 51.69 billion in 2026 to reach USD 71.32 billion by 2031, at a CAGR of 6.65% during the forecast period (2026-2031).

This report is Segmented by Product Type (Bread, Cakes and Pastries, Biscuits/Cookies, Morning Goods, Other Product Types), Form (Fresh, Frozen), Category (Conventional, Free-Form), Distribution Channel (On-Trade Channel, Off-Trade Channel), and Geography (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Unit).

South America Bakery Products Market Trends and Insights

Urbanization and Rising Disposable Income

Urbanization and rising disposable incomes are driving the growth of South America's bakery products market. In 2024, the region had approximately 186.6 million urban dwellers, with an overall urbanization rate of 87%, and Argentina reached 93%. This urban concentration has increased the demand for convenient, ready-to-eat bakery products . In Brazil, Grupo Bimbo offers products such as Pullman sliced bread and Plusvita cakes to serve consumers seeking quick meals and snacks. In Colombia, Productos Ramo provides Chocoramo and Gala pastries, while in Argentina, Bagley's Chocolinas and Criollitas cookies and crackers meet consumer snacking needs. The increase in disposable income has strengthened the demand for premium and artisanal baked goods in major metropolitan areas like Sao Paulo, Buenos Aires, and Bogota. Local establishments, such as Padaria Bella Paulista in Sao Paulo, offer specialized breads and pastries. Consumer preferences are shifting toward bakery products that combine health benefits with convenience, as demonstrated by Wickbold's whole-grain breads in Brazil and Ramo's portion-controlled snack cakes in Colombia. Companies are adapting their packaging and formats to facilitate consumption at home, work, or during commutes. The bakery products market continues to expand as it adapts to the changing preferences of South American urban consumers.

Demand for Artisanal and Premium Bakery Products

In South America, particularly in Brazil and Argentina, urbanization and rising disposable incomes are fueling a growing appetite for artisanal and premium bakery products. In Brazil, Grupo Bimbo's acquisition of Wickbold, a bakery in Sao Paulo known for its whole-grain and specialty breads, highlights the nation's shift towards high-quality, artisanal offerings. In 2024, Brazilian households averaged nearly BRL 1,180 in spending on grocery and bakery items, underscoring their increased disposable income and a readiness to invest in quality . This acquisition not only bolsters Grupo Bimbo's portfolio with brands like Wickbold and Seven Boys but also resonates with the evolving preferences of Brazilian consumers, who are gravitating towards sophisticated and health-oriented bakery choices. Meanwhile, Argentina's urban centers are witnessing a surge in gourmet bakeries, signaling a broader trend towards premium products. "La Panaderia de Pablo" in Buenos Aires, for instance, is carving a niche by providing artisanal breads and pastries crafted with traditional methods and natural ingredients, appealing to a consumer base that values authenticity and quality. These trends underscore a significant shift in consumer behavior, with artisanal and premium bakery products taking center stage in South America's market evolution.

Regulatory Challenges for Clean Labeling

Regulatory hurdles surrounding clean labeling are stifling the growth of South America's bakery products market, introducing uncertainty and escalating compliance costs for producers. In Brazil, newly instituted front-of-pack warning labels for sugar, sodium, and saturated fats have compelled major brands, like Wickbold and Bauducco, to reformulate their popular sliced breads and cookies. However, inconsistent enforcement and disputes over deadlines have deterred smaller bakeries from venturing into clean-label innovations. These challenges have also slowed the adoption of healthier product lines, impacting the overall market growth. Furthermore, Brazil's 2023 regulation concerning "whole grain" claims faced backlash. It allowed certain packaged breads and biscuits, containing only a hint of wholemeal flour, to be marketed as whole grain. This not only muddied the waters for discerning consumers but also jeopardized trust in genuinely healthier options, such as Jasmine Alimentos' gluten-free breads. Meanwhile, in Argentina, stringent front-of-pack labeling mandates, including black octagon warnings, have impacted products like Havanna's alfajores and Fargo's cakes. These regulations limit marketing to children and prohibit sales in schools. Although these measures aim to promote healthier consumer choices, industry lobbying and postponed enforcement have led to uncertainty, inflating costs associated with reformulation and packaging.

Other drivers and restraints analyzed in the detailed report include:

- Health and Wellness: Clean Label and Free-From Trends

- Strategic Marketing and Promotional Campaigns

- Competition from Freshly Baked Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, bread commands a dominant 60.48% market share, underscoring its status as a household staple throughout South America. Brands such as Brazil's Wickbold and Grupo Bimbo's diverse offerings play a pivotal role in this supremacy, presenting everything from traditional loaves to specialty whole-grain options. Bread's ubiquitous presence, found in both urban supermarkets and local neighborhood stores, solidifies its status as the cornerstone of the bakery market.

Morning goods are set to be the fastest-growing segment, with projections indicating a 9.12% CAGR through 2031. This surge is largely attributed to urbanization and evolving breakfast preferences leaning towards convenience. Grupo Bimbo is at the forefront, promoting packaged croissants and their "Little Bites" muffin-style snacks for those on the move. In Colombia, Productos Ramo taps into this trend with their snack cakes, Gala and Chocoramo, which double as popular breakfast alternatives. While cakes and pastries thrive on a culture of premiumization and celebration, biscuits and cookies from Argentina's Bagley capitalize on snacking moments, benefiting from their extended shelf life in warmer climates.

In 2025, fresh products command a dominant 81.85% market share, buoyed by consumer preferences for softness, freshness, and local sourcing. In Brazil, top brands such as Bauducco, Wickbold, and Pullman cultivate robust consumer loyalty, offering a diverse range of packaged breads that span from classic white loaves to unique specialty varieties. Grupo Bimbo fortifies its market stance with its Ana Maria brand, which caters to health-conscious consumers with its reduced-sugar breads. Meanwhile, Crocantissimo and Panco diversify the market with their innovative formats and flavor extensions. Collectively, these brands anchor fresh packaged bakery items as staples in South American households.

On the other hand, frozen products are on an upswing, charting a 7.6% CAGR through 2031. This growth is largely attributed to advancements in cold chain logistics and a burgeoning demand from the foodservice sector. In Brazil, Pao & Arte has broadened its horizons, introducing artisanal-style breads to its frozen bakery lineup. Concurrently, Brico Bread has rolled out ready-to-bake frozen offerings, merging convenience with unwavering quality. These developments underscore the transition of frozen bakery items from a niche market to a mainstream staple. They not only present operational advantages for eateries but also deliver traditional flavors to consumers, albeit with an extended shelf life. The interplay of fresh and frozen segments underscores the delicate balance of tradition and innovation that defines South America's bakery landscape.

List of Companies Covered in this Report:

- Grupo Bimbo SAB de CV

- PepsiCo Inc.

- Wickbold & Nosso Pao S.A.

- Europastry S.A.

- Mondelez International Inc.

- General Mills Inc.

- Associated British Foods plc

- M Dias Branco S.A.

- Grupo Arcor S.A.I.C.

- Nestle S.A.

- Puratos Group

- Dawn Food Products Inc.

- Alicorp S.A.A.

- Pan Pa' Ya S.A.S.

- La Casa Alfajores

- Bagley Argentina S.A.

- BredenMaster Chile S.A.

- Pagnifique Uruguay S.A.

- Los Castanos Chile

- Bakers Delight Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanization and rising disposable income

- 4.2.2 Demand for artisanal and premium bakery products

- 4.2.3 Health and wellness: clean label and free-from trends

- 4.2.4 Expansion of cafes and quick-service outlets

- 4.2.5 Strategic marketing and promotional campaigns

- 4.2.6 Innovations in packaging and flavors

- 4.3 Market Restraints

- 4.3.1 Supply chain disruptions

- 4.3.2 Regulatory challenges for clean labeling

- 4.3.3 Competition from freshly baked products

- 4.3.4 Shift to healthier snack alternatives

- 4.4 Consumer Behavior Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Bread

- 5.1.2 Cakes and Pastries

- 5.1.3 Biscuits/Cookies

- 5.1.4 Morning Goods

- 5.1.5 Other Product Types

- 5.2 By Form

- 5.2.1 Fresh

- 5.2.2 Frozen

- 5.3 By Category

- 5.3.1 Conventional

- 5.3.2 Free-Form

- 5.4 By Distribution Channel

- 5.4.1 On- Trade Channel

- 5.4.2 Off- Trade Channel

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Convenience/Grocery Stores

- 5.4.2.3 Specialist Bakery Shops

- 5.4.2.4 Online Retail Stores

- 5.4.2.5 Other Distribution Channel

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Grupo Bimbo SAB de CV

- 6.4.2 PepsiCo Inc.

- 6.4.3 Wickbold & Nosso Pao S.A.

- 6.4.4 Europastry S.A.

- 6.4.5 Mondelez International Inc.

- 6.4.6 General Mills Inc.

- 6.4.7 Associated British Foods plc

- 6.4.8 M Dias Branco S.A.

- 6.4.9 Grupo Arcor S.A.I.C.

- 6.4.10 Nestle S.A.

- 6.4.11 Puratos Group

- 6.4.12 Dawn Food Products Inc.

- 6.4.13 Alicorp S.A.A.

- 6.4.14 Pan Pa' Ya S.A.S.

- 6.4.15 La Casa Alfajores

- 6.4.16 Bagley Argentina S.A.

- 6.4.17 BredenMaster Chile S.A.

- 6.4.18 Pagnifique Uruguay S.A.

- 6.4.19 Los Castanos Chile

- 6.4.20 Bakers Delight Holdings Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK