PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061635

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061635

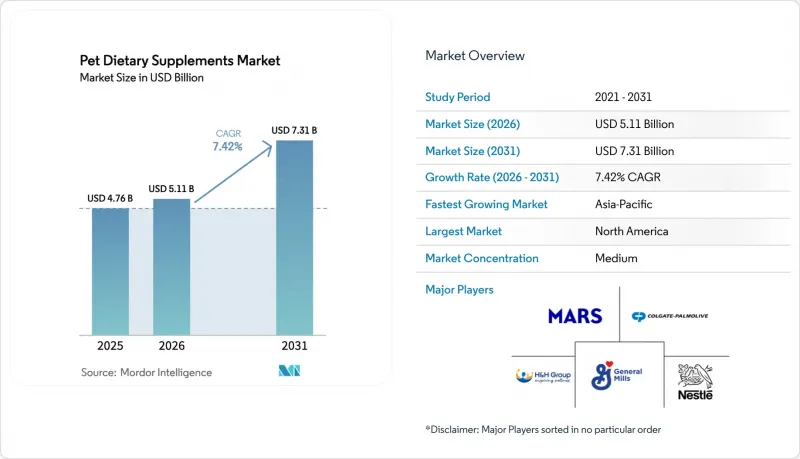

Pet Dietary Supplements - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pet dietary supplements market is projected to expand from USD 4.76 billion in 2025 and USD 5.11 billion in 2026 to USD 7.31 billion by 2031, registering a CAGR of 7.42% between 2026 to 2031.

This report is Segmented by Product Form (Tablets and Capsules, Chewables and Soft Chews, and More), by Supplement Type (Multivitamins, Antioxidants, and More), by Function (Urinary Tract Health, and More), by Pet Type (Dogs, and More), by Distribution Channel (Convenience Stores, and More), and by Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Pet Dietary Supplements Market Trends and Insights

Rising Demand for Multivitamin Soft-Chews

Palatability drives compliance in daily supplement regimens, and soft-chews have emerged as the dominant delivery format because they mimic treats rather than medication. Pet owners report higher adherence rates with chewable formats compared to tablets or capsules, a behavioral insight that has prompted manufacturers to invest in flavor-masking technologies and texture optimization. Zesty Paws, a subsidiary of H&H Group, is expanding its distribution network by increasing the number of retail stores. The company is focusing on bacon-flavored and peanut-butter soft chews formulated for voluntary consumption by dogs . The format's success has also attracted private-label entrants, as retailers recognize that soft-chews command premium shelf prices while generating repeat purchases. Manufacturers are responding by exploring pectin-based vegan alternatives, though these formulations require additional stabilizers to match the chewability of animal-derived gelatin.

Veterinary Endorsement of Probiotic Formulas

Veterinarians function as gatekeepers in the pet supplement market, and their willingness to recommend specific products directly influences retail adoption rates. Clinical evidence supporting the use of probiotics for gastrointestinal health has reached a tipping point, with peer-reviewed studies demonstrating that strains such as Enterococcus faecium and Bifidobacterium animalis reduce the duration of diarrhea and improve fecal consistency in dogs. A 2024 study published in the Journal of Veterinary Internal Medicine found that dogs receiving Visbiome Vet experienced a 42% reduction in acute diarrhea episodes compared to dogs in the placebo group. Purina's FortiFlora, which holds the largest share of the veterinary probiotic segment, benefits from decades of clinical trials and a sales force that educates practitioners on microbiome science.

Price Sensitivity Among First-Time Buyers

Pet supplements occupy an ambiguous position in household budgets, perceived as beneficial but not essential, which makes them vulnerable to discretionary spending cuts during economic downturns. First-time buyers, who often enter the category through veterinary recommendations or social media advertising, exhibit high price elasticity, with conversion rates dropping 40% when products exceed USD 30 per month, according to internal data from digital-native brands. This sensitivity is most pronounced in emerging markets, where per-capita pet spending remains a fraction of the levels in North America. Brands have responded by introducing starter packs and trial sizes priced below USD 15, though these formats erode gross margins and complicate inventory management. The challenge for premium brands lies in communicating value propositions beyond price, such as clinical validation, veterinary endorsements, and transparent supply chains, to justify higher price points.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Personalized Microbiome Blends

- Algae-Derived Omega-3 Cost Parity with Fish Oil

- Counterfeit Products on Cross-Border Marketplaces

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chewable and soft chews captured 48% of the pet dietary supplements market size in 2025, a dominance rooted in behavioral psychology rather than nutritional superiority. Pet owners struggle with pill administration, and chewable formats eliminate the friction of forcing tablets down reluctant pets' throats. Regulatory influence remains minimal in product-form selection, as the Food and Drug Administration (FDA) focuses on ingredient safety rather than delivery mechanisms. The European Food Safety Authority has raised concerns about certain gelling agents used in soft chews, prompting manufacturers to reformulate with European Food Safety Authority (EFSA)-approved alternatives, such as carrageenan and agar. The shift toward soft-chews reflects broader humanization trends, as pet owners increasingly demand products that mirror their own supplement routines in format and flavor.

Powders are forecasted to grow at an 11.2% CAGR through 2031, driven by their compatibility with personalized dosing algorithms and lower per-unit manufacturing costs, which enable competitive pricing. Powders benefit from the rise of personalized nutrition platforms that ship custom-blended sachets, although they require pet owners to mix supplements into their pet's food, adding a compliance hurdle. Other forms, including topical sprays and transdermal patches, occupy niche segments but are gaining traction for joint-pain relief where oral bioavailability is suboptimal.

Multivitamins accounted for 36% of the pet dietary supplements market size in 2025, benefiting from their broad appeal and veterinary recommendations for general wellness. Cannabidiol (CBD) regulatory uncertainty hinders mainstream adoption, as manufacturers opt to avoid interstate commerce to circumvent federal enforcement, thereby limiting distribution to state-licensed dispensaries and online direct-to-consumer channels. Herbal extracts, such as turmeric and ashwagandha, are marketed for their anti-inflammatory and calming benefits, although the Food and Drug Administration (FDA) has issued warning letters to companies making disease-treatment claims without substantiation.

Probiotics and prebiotics are projected to expand at a 10.5% CAGR to 2031, as clinical evidence mounts for their role in digestive and immune health. The probiotic surge reflects a convergence of scientific validation and veterinary advocacy. A 2024 meta-analysis published in Frontiers in Veterinary Science reviewed 28 randomized controlled trials and concluded that multi-strain probiotic formulations reduced gastrointestinal symptoms in 67% of dogs with chronic enteropathies . Prebiotics, which nourish beneficial gut bacteria, are increasingly bundled with probiotics in synbiotic formulations that enhance colonization rates.

Geography Analysis

North America accounted for 48.4% of global revenue in 2025, driven by high disposable incomes, mature veterinary infrastructure, and cultural norms that treat pets as family members. The United States dominates regional revenue, with California, Texas, and Florida accounting for 42% of national sales due to high pet ownership rates and the concentration of digital-native brands. Canada's bilingual labeling requirements and stricter import regulations add complexity for cross-border distribution, though the market's affluence and veterinary channel strength support premium pricing. Mexico represents an emerging opportunity, with urbanization and rising middle-class incomes driving the adoption of pet supplements, although counterfeit products and unregulated distribution channels constrain growth.

The Asia-Pacific region is projected to grow at a CAGR of 7.4% through 2031, the fastest regional growth rate, fueled by urbanization, nuclear family structures, and e-commerce penetration in China, Japan, and South Korea. China's pet supplement market is concentrated in tier-1 cities such as Beijing, Shanghai, and Shenzhen, where disposable incomes exceed USD 15,000 per capita, and pet ownership is viewed as a status symbol. Tmall and JD.com dominate online distribution, leveraging livestream commerce and influencer partnerships to drive supplement sales. Japan's aging pet population mirrors its human demographic trends, with 40% of dogs over 10 years old, creating demand for senior-specific formulations targeting joint health and cognitive function. India represents a nascent market with high growth potential, though price sensitivity and limited veterinary infrastructure constrain premium segment adoption.

Europe is projected to grow with Germany, the United Kingdom, and France leading regional revenue. The European Food Safety Authority's rigorous novel-ingredient approval process delays product launches but enhances consumer trust in supplement safety and efficacy. Germany's preference for natural and organic products has driven demand for herbal supplements and algae-based omega-3, while the United Kingdom veterinary channel strength supports prescription-grade formulations. France's regulatory environment mandates veterinary oversight for certain supplement categories, limiting direct-to-consumer distribution but ensuring professional guidance. Southern Europe, including Italy and Spain, exhibits lower supplement penetration due to cultural norms that prioritize fresh-food diets over processed supplements.

- Nestle (Purina)

- Mars Incorporated (Mars Petcare)

- Colgate-Palmolive Company (Hills Pet Nutrition)

- General Mills Inc. (Blue Buffalo)

- H&H Group (Zesty Paws)

- Nutramax Laboratories, Inc.

- Elanco

- Zoetis Services LLC

- Virbac

- Kemin Industries, Inc.

- Nordic Naturals

- Healthy Pets (PetAlive)

- Schell & Kampeter, Inc. (Diamond Pet Foods)

- Wellness Pet, LLC

- Affinity Petcare S.A. (A Subsidiary of Agrolimen SA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for multivitamin soft-chews

- 4.2.2 Veterinary endorsement of probiotic formulas

- 4.2.3 Subscription-based Direct-To-Consumer (DTC) e-commerce expands Average Order Value (AOV)

- 4.2.4 AI-driven personalized microbiome blends

- 4.2.5 Algae-derived omega-3 cost parity with fish oil

- 4.2.6 Postbiotic stability enables ambient logistics

- 4.3 Market Restraints

- 4.3.1 Stringent Food and Drug Administration (FDA) and Association of American Feed Control Officials (AAFCO) claim regulations

- 4.3.2 Price sensitivity among first-time buyers

- 4.3.3 Volatile krill-oil supply chain

- 4.3.4 Counterfeit products on cross-border marketplaces

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Form

- 5.1.1 Tablets and Capsules

- 5.1.2 Chewable and Soft Chews

- 5.1.3 Powders

- 5.1.4 Liquids and Gels

- 5.1.5 Capsules

- 5.1.6 Other Forms

- 5.2 By Supplement Type

- 5.2.1 Multivitamins

- 5.2.2 Probiotics and Prebiotics

- 5.2.3 Omega-3 and Essential Fatty Acids

- 5.2.4 Glucosamine and Chondroitin

- 5.2.5 CBD and Hemp Derivatives

- 5.2.6 Antioxidants

- 5.2.7 Herbal and Botanical Extracts

- 5.2.8 Other Supplement Type

- 5.3 By Function

- 5.3.1 Urinary Tract Health

- 5.3.2 Hip and Joint Health

- 5.3.3 Diabetes Management

- 5.3.4 Heart and Renal Health

- 5.3.5 Skin and Coat Health

- 5.3.6 Immune System Support

- 5.3.7 Digestive Health

- 5.3.8 Calming and Anxiety Relief

- 5.3.9 Dental and Oral Care

- 5.3.10 Metabolic/ Weight Management

- 5.3.11 Senior/Cognitive Support

- 5.3.12 Other Specialty Needs

- 5.4 By Pet Type

- 5.4.1 Dogs

- 5.4.2 Cats

- 5.4.3 Other Pets

- 5.5 By Distribution Channel

- 5.5.1 Convenience Stores

- 5.5.2 Online Channel

- 5.5.3 Specialty Stores

- 5.5.4 Supermarkets/Hypermarkets

- 5.5.5 Other Channels

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Israel

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Nestle (Purina)

- 6.3.2 Mars Incorporated (Mars Petcare)

- 6.3.3 Colgate-Palmolive Company (Hills Pet Nutrition)

- 6.3.4 General Mills Inc. (Blue Buffalo)

- 6.3.5 H&H Group (Zesty Paws)

- 6.3.6 Nutramax Laboratories, Inc.

- 6.3.7 Elanco

- 6.3.8 Zoetis Services LLC

- 6.3.9 Virbac

- 6.3.10 Kemin Industries, Inc.

- 6.3.11 Nordic Naturals

- 6.3.12 Healthy Pets (PetAlive)

- 6.3.13 Schell & Kampeter, Inc. (Diamond Pet Foods)

- 6.3.14 Wellness Pet, LLC

- 6.3.15 Affinity Petcare S.A. (A Subsidiary of Agrolimen SA)

7 Market Opportunities and Future Outlook