PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061649

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061649

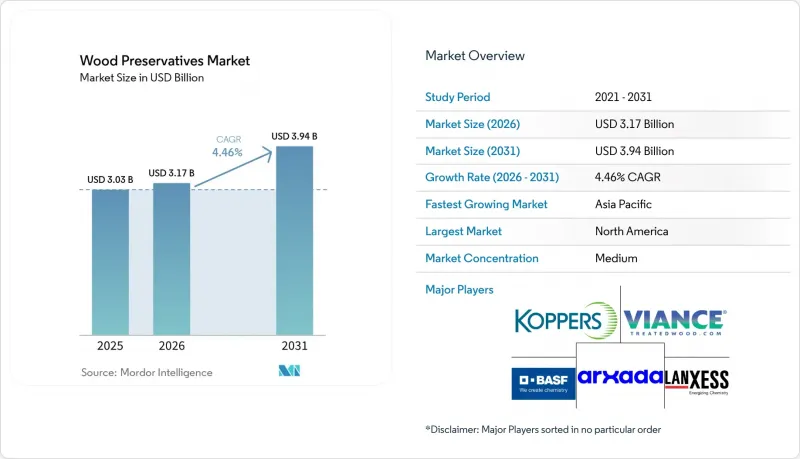

Wood Preservatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the wood preservatives market size is expected to grow from USD 3.03 billion in 2025 to USD 3.17 billion in 2026 and is forecast to reach USD 3.94 billion by 2031 at a 4.46% CAGR over 2026-2031.

This report is Segmented by Technology (Water-Based Technologies, Oil-Based Technologies, and Other Emerging Technologies), End-User Industry (Residential Construction, Commercial and Institutional Buildings, Infrastructure, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Wood Preservatives Market Trends and Insights

Construction Boom in Residential and Infrastructure Projects

Governments continue to channel sizable budgets into road, rail, and public works pipelines, and that spending dovetails with a rebound in single-family housing starts to lift preservative consumption across framing lumber, decking, and heavy timbers. India's National Infrastructure Pipeline has earmarked USD 1.4 trillion through 2025, much of which specifies treated sleepers and bridge components. China sustains legacy railway upgrades that draw on creosote and copper-chrome formulations even as property-sector headwinds persist. In the United States, completions for detached housing improved in 2025, while renovation spending on patios, pergolas, and privacy fences pushed demand for copper-azole and micronized-copper lumber. The driver adds 1.8 percentage points to the overall CAGR, with influence peaking in the medium term as infrastructure projects move from planning to execution.

Shift Toward Eco-Friendly Water-Based and Copper-Based Systems

Regulatory bans on pentachlorophenol and usage caps on chromated copper arsenate have accelerated the transition toward water-dispersible copper compounds. The US Environmental Protection Agency's 2022 order ends pentachlorophenol by February 2027, forcing utility companies to certify copper naphthenate and micronized-copper poles. Micronized particles below 1 micron exhibit measurably lower leaching than dissolved copper salts, reducing aquatic toxicity without sacrificing fungicidal power. Arxada's Preserve range achieves 96.1% recycled-copper content in CA-C and CA-B products, aligning preservative selection with circular-economy credits in green-building programs. As European regulators classify copper with an aquatic M-factor of 10, innovators respond with encapsulated-release platforms that trim effective loading rates. The driver supplies a 1.2 percentage-point uplift to growth over the long run as standards in Asia-Pacific and Latin America converge on EU and U.S. norms.

Stringent Bans or Restrictions on CCA, PCP, Creosote, and VOC Limits

The U.S. Environmental Protection Agency finalized pentachlorophenol's cancellation in 2022, eliminating inventory by February 2027 and ending a seven-decade utility-pole standard. Chromated copper arsenate remains confined to restricted industrial uses under exacting disposal rules, while creosote faces parallel limits in the European Union's Persistent Organic Pollutants Regulation. VOC caps in coatings push formulators toward water carriers that demand fresh R&D outlays. The EU Biocidal Products Regulation now screens out carcinogens, mutagens, endocrine disruptors, and very persistent, very mobile substances, extending timeframes and raising costs for every new active. Collectively, these actions shave 1.1 percentage points off the CAGR in the near term as phase-out dates collide with field-trial bottlenecks.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Outdoor Living (Decking, Fencing, and Landscaping)

- Durability Needs for Utility Poles, Rail Sleepers, and Marine Piles

- Volatility in Copper and Commodity Biocide Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-based systems accounted for a commanding 79.05% share of the wood preservatives market in 2025 and are forecast to rise at a 4.31% CAGR through 2031. This leadership springs from micronized-copper particles that leach 30% to 50% less active ingredient than dissolved salts, thereby meeting tougher aquatic-toxicity thresholds. In 2025, the water-based portion represented the largest single component of the wood preservatives market size at USD 2.5 billion, and ongoing substitution away from oil-borne actives cements its trajectory. The residual share belongs to oil-borne chemistries, chiefly creosote and vegetable-oil blends, which face volume pressure as phase-out deadlines arrive in North America and the European Union. Yet creosote still claims relevance for rail sleepers and marine structures where high-retention, heavy-duty protection justifies elevated toxicity management.

Second-generation water-based offerings now integrate recycled-copper feedstocks that hedge price swings and burnish green-building credentials. Arxada's Wolman E line leverages BARamine technology to stabilize copper azole and slow volatilization. Borate diffusions flourish in interior framing where low mammalian toxicity and adhesive compatibility trump weather durability. Bio-derived terpenes and nano-copper dispersions hover in pilot scale, their path impeded by multi-jurisdictional approvals. Over the forecast horizon, the water-based segment is expected to secure more share of wood preservatives market size, reflecting a decisive tilt toward chemistries that reconcile efficacy with environmental stewardship.

Geography Analysis

North America generated 36.14% of global sales in 2025, underpinned by a mature installed base of utility poles and a housing stock that embraces pressure-treated lumber for exterior applications. US utilities continued field verification of copper naphthenate and micronized-copper poles ahead of the February 2027 pentachlorophenol sunset EPA.GOV. Canada's forestry sector provides a reliable supply of preservative-grade lumber, while Mexico's growing middle class sustains fencing and decking activity. Europe remains defined by stringent Biocidal Products Regulation scrutiny, which both inflates compliance costs and fosters innovation. Germany, France, and the United Kingdom account for the majority of European demand, and Arxada's 2023 GB BPR authorization for Tanasote underscores the pathway for new copper-oil hybrids.

Asia-Pacific is on a faster track, poised to grow at a 5.72% CAGR as China and India concentrate infrastructure spending on rail and bridge programs that specify treated sleepers and load-bearing timbers. India's National Infrastructure Pipeline draws heavily on treated wood to stretch budgets and accelerate project timelines. China's coastal port expansions likewise depend on marine-grade pilings. Japan's aging grid and rail infrastructure create steady replacement cycles even as the nation pioneers mass-timber mid-rise apartments. ASEAN economies favor cost-effective oil-borne preservatives, but environmental codes are tightening and will gradually channel demand toward water-based systems. South America's outlook hinges on Brazil's Minha Casa Minha Vida housing program and Argentina's farm infrastructure expansion, while fiscal constraints moderate upside in the Middle East and Africa.

The combined dynamics yield a diversified demand map: North America and Europe present high-regulation, high-value environments; Asia-Pacific offers the strongest volume growth; Latin America, the Middle East, and Africa supply option value that hinges on macroeconomic stability.

- Advance Agrisearch Limited

- Arch Wood Protection (Arxada)

- Artemis Biotech

- BASF

- BERKEM

- Changchun New Sunlight Wood Products Co., Ltd.

- Copper Care Wood Preservatives, Inc.

- Dolphin Bay

- Impra Wood Protection Ltd.

- Jubilant Ingrevia Limited

- Koppers Performance Chemicals

- Kurt Obermeier GmbH & Co. KG

- LANXESS

- Nisus Corporation

- Remmers International

- Timber Treat

- TIMBERLIFE (Pty) Ltd.

- Viance

- Wolman Wood & Fire Protection GmbH

- Wuhan Hombo Industrial Co.,Ltd

- Wykamol Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction boom in residential and infrastructure projects

- 4.2.2 Shift toward eco-friendly water-based and copper-based systems

- 4.2.3 Growth in outdoor living (decking, fencing, and landscaping)

- 4.2.4 Durability needs for utility poles, rail sleepers, and marine piles

- 4.2.5 Emergence of carbon-negative mass-timber buildings needing advanced protection

- 4.3 Market Restraints

- 4.3.1 Stringent bans/restrictions on CCA, PCP, Creosote, and VOC limits

- 4.3.2 Volatility in copper and commodity biocide feedstock prices

- 4.3.3 Fire-retardant CLT coatings reducing demand for deep-soak treatments

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape (REACH, EPA, BPR, CPCB, GB/T)

- 4.6 Technological Outlook (nano-copper, bio-borates, encapsulated actives)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-based Technologies

- 5.1.1.1 Micronized Copper Systems

- 5.1.1.2 Chromated Copper Arsenate (legacy/phase-out markets)

- 5.1.1.3 Borates (indoor use)

- 5.1.1.4 Other Technologies (Bio-based and Nano-formulated Preservatives)

- 5.1.2 Oil-based Technologies

- 5.1.2.1 Pentachlorophenol

- 5.1.2.2 Creosote

- 5.1.2.3 Other Oil Based Technologies (Vegetable-oil Carriers and Hybrid Oils)

- 5.1.3 Other Emerging Technologies

- 5.1.1 Water-based Technologies

- 5.2 By End-user Industry

- 5.2.1 Residential Construction

- 5.2.2 Commercial and Institutional Buildings

- 5.2.3 Infrastructure (utility poles, rail, bridges, and ports)

- 5.2.4 Industrial Facilities

- 5.3 By Geography (Value)

- 5.3.1 Asia-Pacifc

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacifc

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Advance Agrisearch Limited

- 6.4.2 Arch Wood Protection (Arxada)

- 6.4.3 Artemis Biotech

- 6.4.4 BASF

- 6.4.5 BERKEM

- 6.4.6 Changchun New Sunlight Wood Products Co., Ltd.

- 6.4.7 Copper Care Wood Preservatives, Inc.

- 6.4.8 Dolphin Bay

- 6.4.9 Impra Wood Protection Ltd.

- 6.4.10 Jubilant Ingrevia Limited

- 6.4.11 Koppers Performance Chemicals

- 6.4.12 Kurt Obermeier GmbH & Co. KG

- 6.4.13 LANXESS

- 6.4.14 Nisus Corporation

- 6.4.15 Remmers International

- 6.4.16 Timber Treat

- 6.4.17 TIMBERLIFE (Pty) Ltd.

- 6.4.18 Viance

- 6.4.19 Wolman Wood & Fire Protection GmbH

- 6.4.20 Wuhan Hombo Industrial Co.,Ltd

- 6.4.21 Wykamol Group Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Fiscal incentives for bio-derived preservatives in EU & selected U.S. states