PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061653

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061653

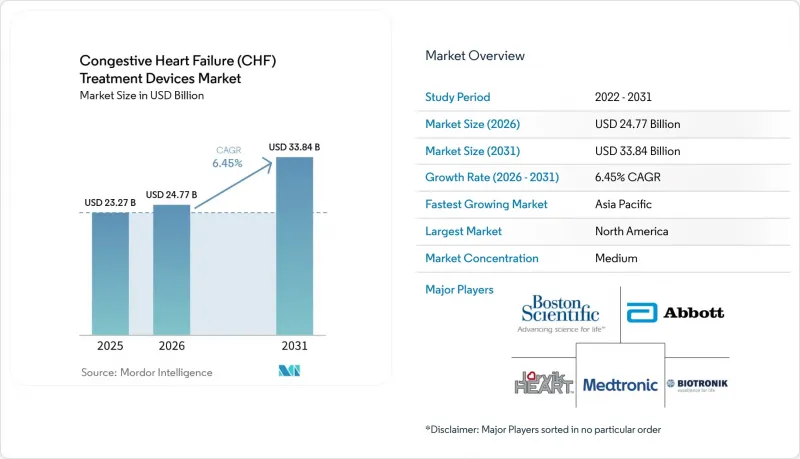

Congestive Heart Failure (CHF) Treatment Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the congestive heart failure (CHF) treatment devices market size is expected to grow from USD 23.27 billion in 2025 to USD 24.77 billion in 2026 and is forecast to reach USD 33.84 billion by 2031 at 6.45% CAGR over 2026-2031.

This report is Segmented by Product (Ventricular Assist Devices, Counter-Pulsation Devices, Implantable Cardioverter-Defibrillators, Pacemakers, Cardiac Resynchronization Therapy), End-User (Hospitals, Specialty Cardiac Centers, Ambulatory Surgical Centers), & Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Congestive Heart Failure (CHF) Treatment Devices Market Trends and Insights

Prevalence Escalation of CHF & Co-Morbid CVDs

Rising incidence of chronic heart failure is redefining baseline demand for device therapy. U.S. cases are expected to climb to 11.4 million by 2050, up from 6.7 million patients in 2025. Asia mirrors this trajectory; age-standardized prevalence surpassed 722.45 per 100,000 population by 2022. Comorbidity clusters involving diabetes, hypertension, and coronary artery disease are boosting utilization of multi-component solutions such as combined CRT-defibrillator systems. Expanded clinical criteria now allow CRT for ejection fractions up to 45%, enlarging the candidate pool. Payers are responding with value-based pathways that reward reductions in rehospitalization, reinforcing device adoption.

Aging Population Fueling Device-Eligible Patients

Nearly one-quarter of U.S. citizens will be 65 or older by 2060. Geriatric cohorts exhibit higher severity heart failure and lower medical therapy tolerance, prompting earlier consideration of mechanical circulatory support. Destination therapy now represents 73% of VAD implants, a reversal from bridge-to-transplant dominance a decade earlier . Miniaturized LVAD pumps and fully percutaneous leadless pacemakers are facilitating procedures in frail patients. Hospitals have started dedicated geriatric cardiac programs to manage peri-operative risks and support post-implant rehabilitation.

High Upfront Device & Procedure Costs

LVAD systems list between USD 150,000-200,000, exclusive of surgery and long-term anticoagulation, pricing out many centers in low-income regions. India's drug market shows branded-to-generic cost spreads of 3.27 times, implying similar disparities for devices. Payers in developed nations cover implants but balk at funding the specialized staffing models required for continuous ambulatory support. Adoption of bundled payments is slow, leaving hospitals to shoulder capital budgeting risk.

Other drivers and restraints analyzed in the detailed report include:

- Third-Generation Continuous-Flow LVAD Innovations

- Regulatory Fast-Track for Leadless CRT & CCM Implants

- AI-Based Remote Monitoring Platforms for Implanted Devices

- Additive-Manufactured Pump Components Lowering Custom-Build Time

- Device-Related Infection & Thrombosis Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The ventricular assist device segment retained a 38.02% revenue share in 2025, underscoring its pivotal place in advanced therapy. Continuous-flow systems like HeartMate 3 coupled with total artificial heart concepts are lifting survival rates and widening indication boundaries. Intra-aortic balloon pumps, once ubiquitous, are encountering diminished utility after randomized studies questioned routine deployment in cardiogenic shock.

Cardiac resynchronization therapy is the quickest climber at a 7.15% CAGR to 2031. Regulatory expansion to higher ejection fractions and leadless form factors is propelling penetration. Subcutaneous implantable cardioverter-defibrillators and leadless pacemakers are eroding leads-based device segments through fewer pocket infections and simpler procedures. Artificial intelligence features for automatic vector optimization are further differentiating new CRT models.

Geography Analysis

North America's 43.02% congestive heart failure (CHF) treatment devices market share in 2025 stems from Medicare coverage, abundant fellowship-trained surgeons, and 1,041 FDA breakthrough device designations fostering rapid tech turnover. Canada's single-payer model ensures equitable access, while Mexico's private insurers target affluent urban populations with CRT and ICD offerings.

Europe follows as a mature adopter anchored by Germany's high procedural volumes and the EU's Medical Device Regulation establishing uniform conformity protocols. The United Kingdom's National Health Service secures population-wide coverage even as post-Brexit supply chains recalibrate. France, Italy, and Spain supplement growth with robust investigator-initiated trials that provide real-world evidence for CRT efficacy.

Asia-Pacific records the fastest 7.99% CAGR to 2031. Japan, facing rapid demographic aging, is a lead adopter of dual-chamber leadless pacemakers. India's medical device sector targets USD 50 billion size by 2025, and government initiatives are streamlining local manufacturing . South Korea's national health insurance now reimburses LVAD implants, while Australia offers a developed market entry point for U.S. and European manufacturers.

- Abbott Laboratories

- Medtronic

- Boston Scientific

- Abiomed (J&J)

- Berlin Heart

- BIOTRONIK

- Jarvik Heart

- Lepu Medical Tech.

- Magenta Medical Ltd.

- MicroPort

- EBR Systems

- LivaNova

- Terumo Corp.

- Syncardia Systems LLC

- Shree Pacetronix

- MEDICO S.r.l.

- Oscor

- OSYPKA Medical GmbH

- Calon Cardio-Technology

- CoreWave SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Prevalence Escalation Of CHF & Co-Morbid CVDs

- 4.2.2 Aging Population Fueling Device-Eligible Patients

- 4.2.3 Third-Generation Continuous-Flow LVAD Innovations

- 4.2.4 Regulatory Fast-Track For Leadless CRT & CCM Implants

- 4.2.5 AI-Based Remote Monitoring Platforms For Implanted Devices

- 4.2.6 Additive-Manufactured Pump Components Lowering Custom-Build Time

- 4.3 Market Restraints

- 4.3.1 High Upfront Device & Procedure Costs

- 4.3.2 Reimbursement Gaps In Emerging Markets

- 4.3.3 Device-Related Infection & Thrombosis Risk

- 4.3.4 Shortage Of Advanced HF Surgeons & Vad Coordinators

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value; USD million)

- 5.1 By Product

- 5.1.1 Ventricular Assist Devices (VADs)

- 5.1.1.1 LVAD

- 5.1.1.2 RVAD

- 5.1.1.3 BiVAD

- 5.1.2 Counter-Pulsation Devices

- 5.1.3 Implantable Cardioverter-Defibrillators (ICD)

- 5.1.3.1 Transvenous ICD

- 5.1.3.2 Subcutaneous ICD

- 5.1.4 Pacemakers

- 5.1.4.1 Implantable

- 5.1.4.2 External

- 5.1.5 Cardiac Resynchronization Therapy (CRT)

- 5.1.5.1 CRT-D

- 5.1.5.2 CRT-P

- 5.1.1 Ventricular Assist Devices (VADs)

- 5.2 By End-user

- 5.2.1 Hospitals

- 5.2.2 Specialty Cardiac Centers

- 5.2.3 Ambulatory Surgical Centers

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Medtronic PLC

- 6.3.3 Boston Scientific Corp.

- 6.3.4 Abiomed (J&J)

- 6.3.5 Berlin Heart GmbH

- 6.3.6 Biotronik SE & Co. KG

- 6.3.7 Jarvik Heart Inc.

- 6.3.8 Lepu Medical Tech.

- 6.3.9 Magenta Medical Ltd.

- 6.3.10 MicroPort Scientific

- 6.3.11 EBR Systems Inc.

- 6.3.12 LivaNova PLC

- 6.3.13 Terumo Corp.

- 6.3.14 Syncardia Systems LLC

- 6.3.15 Shree Pacetronix Ltd.

- 6.3.16 MEDICO S.r.l.

- 6.3.17 Oscor Inc.

- 6.3.18 OSYPKA Medical GmbH

- 6.3.19 Calon Cardio-Technology

- 6.3.20 CoreWave SA

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment