PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063391

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063391

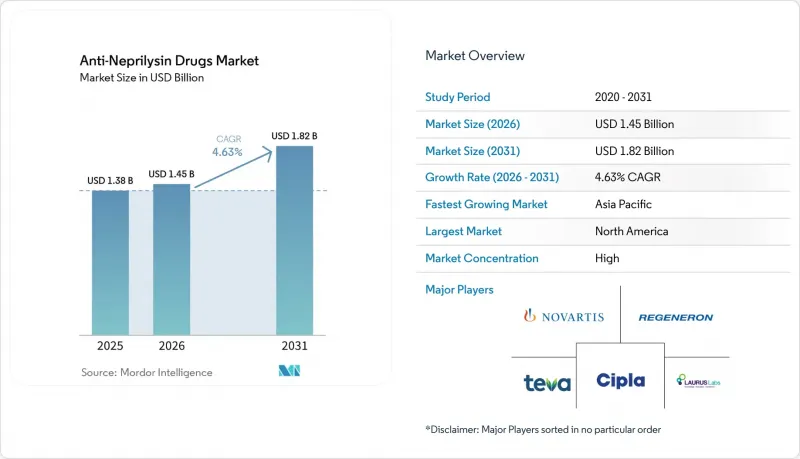

Anti-Neprilysin Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the anti-Neprilysin drugs market size is expected to increase from USD 1.38 billion in 2025 to USD 1.45 billion in 2026 and reach USD 1.82 billion by 2031, growing at a CAGR of 4.63% over 2026-2031.

This report is Segmented by Drug Type (Small-Molecule Inhibitors, Biologic Antibodies & Peptides, Dual-Target Candidates), Indication (HFrEF, HFpEF/HFmrEF, Hypertension, Pain & CNS, Alzheimer's), Dosage Form (Tablets, Suspension, Injectables), Distribution Channel (Hospital, Retail, Online & Specialty), and Geography (North America, and More). Market Forecasts Provided in Value (USD).

Global Anti-Neprilysin Drugs Market Trends and Insights

Rising Prevalence of Chronic Heart Failure & Hypertension

Worldwide heart-failure prevalence touched 64 million people in 2024 and continues to climb, largely because populations are aging and hypertension control remains inconsistent.The American Heart Association counted 6.9 million U.S. adults living with the condition in 2024, estimating that one in five Americans will develop heart failure during their lifetime. Direct medical spending in the United States reached USD 30.7 billion in 2024, a burden that elevates payers' interest in drug classes shown to curb hospitalization. Asia-Pacific is experiencing the fastest case-count expansion as urban diets high in sodium collide with limited blood-pressure screening, yet reimbursement gaps slow uptake. The persistence of high mortality, projected to reach 8 million global deaths by 2030, keeps attention fixed on therapies with proven survival benefit.

Guideline Inclusion of Sacubitril/Valsartan (ARNI)

In 2024 the American College of Cardiology designated ARNI as preferred first-line treatment for HFrEF, replacing long-standing ACE inhibitor and ARB standards. European guidelines mirrored that upgrade, although payer rules differ across member states, slowing uniform rollout. U.S. hospital formularies responded by making ARNI the default heart-failure therapy, yet insurers still enforce prior-authorization hurdles that delay initiation. In single-payer systems such as Ireland and the United Kingdom, budget caps create local restrictions, demonstrating how clinical endorsement alone does not guarantee access. Even so, guideline elevation supports steady prescription growth and strengthens the class in negotiations with health plans.

Patent Expiry & Generic Erosion of Entresto

A Delaware court decision in July 2025 cleared Alembic, MSN, Laurus, and Lupin to launch generic sacubitril/valsartan, ending Novartis's bid for exclusivity through 2026. Branded cardiovascular drugs typically lose 30-50% price inside the first year of multi-source competition, and European approvals such as Teva's Irish listing in September 2025 set the stage for wider erosion. Novartis still holds method-of-use patents into the 2030s, but they cannot block generic marketing for on-label indications, so volume share is likely to slide toward 20-30% by 2028 unless a next-generation product emerges.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Expansion into HFpEF & Pediatrics

- Once-Daily Next-Gen Small-Molecule NEP Inhibitors

- High Therapy Cost & Reimbursement Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Small-molecule inhibitors retained 76.23% of 2025 revenue because sacubitril/valsartan lacks a differentiated competitor. Biologic antibodies and peptides, however, are tracking the fastest 8.46% CAGR and could erode this dominance from 2029 onward. The anti-neprilysin drugs market size for biologics is expected to grow meaningfully once the first late-phase candidates read out pivotal data. Manufacturing cost remains a hurdle, yet expanded peptide and antibody capacity in the United States and Europe is lowering barriers.

The anti-neprilysin drugs market has room for next-generation classes that avoid angioedema and cognitive-safety debates. Regeneron's natriuretic peptide receptor agonist shows early promise, but material commercial impact lies beyond the forecast window. Without near-term replacements, generics will seize share from branded small molecules first, followed by eventual disruption as biologics prove value.

HFrEF delivered 61.53% of 2025 sales thanks to unequivocal survival data and class-I guideline placement. HFpEF/HFmrEF, however, is the fastest-growing indication, rising at 7.34% and expected to narrow the gap by 2031. The anti-neprilysin drugs market share for HFpEF could jump once ongoing real-world studies validate outcomes in higher-ejection-fraction patients. Pediatric approvals widen the total treated pool further, albeit from a smaller base.

Systemic hypertension remains a niche, and pain or CNS disorders are still exploratory. Nevertheless, label expansions broaden payers' willingness to reimburse, creating incremental volume even if per-patient profit compresses under generic pricing.

Geography Analysis

North America's leadership rests on robust diagnosis rates, guideline adherence, and higher disposable income, yet the Inflation Reduction Act will negotiate Medicare prices from 2026, trimming topline by 10-15% for branded therapies. Canada's provincial formularies offer generally favorable coverage, although Quebec caps annual growth in public-drug spending, nudging Novartis toward risk-sharing deals.

Europe transitions into a value-driven phase. While Germany maintains unrestricted access, Southern and Eastern member states apply tighter budget controls. Ireland's early generic listing showcases the speed with which competitive entry can reshape drug spending. Expect further price compression once pan-European tenders gain momentum.

Asia-Pacific is the undisputed growth engine. Japan's pediatric clearance and China's expanded National Reimbursement Drug List reinforce volume, but average selling price is lower because of local procurement rules. The Philippines' 2024 approval signals Southeast Asia's widening access, though affordability remains a sticking point in Vietnam and Indonesia.

Middle East and Africa are nascent. The United Arab Emirates' National Succinct Statement in 2024 points to gradual uptake, but the region's heart-failure infrastructure is still developing. South America offers selective pockets of strength-Brazil's public procurement and private insurance uptake-yet macroeconomic volatility in Argentina and other markets curbs visibility.

- Abbvie

- Amgen

- AstraZeneca

- Bayer

- Bristol-Myers Squibb

- Cipla

- Daiichi Sankyo

- Eli Lilly & Co

- GlaxoSmithKline (GSK)

- Johnson & Johnson

- Laurus Labs

- Merck

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Takeda Pharma

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Heart Failure & Hypertension

- 4.2.2 Guideline Inclusion of Sacubitril/Valsartan (ARNI)

- 4.2.3 Regulatory Expansion into HFpEF & Pediatrics

- 4.2.4 Once-Daily Next-Gen Small-Molecule NEP Inhibitors

- 4.2.5 Low-Cost Biomanufacturing of Anti-Neprilysin Antibodies

- 4.2.6 Expansion of Digital Titration & Remote-Monitoring Platforms

- 4.3 Market Restraints

- 4.3.1 Patent Expiry & Generic Erosion of Entresto

- 4.3.2 High Therapy Cost & Reimbursement Barriers

- 4.3.3 Rising Adoption of Alternative HF Drug Classes

- 4.3.4 Long-Term Cognitive-Safety Concerns

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Drug Type

- 5.1.1 Small-Molecule Inhibitors

- 5.1.2 Biologic Antibodies & Peptides

- 5.1.3 Dual-Target (ACE/NEP, ECE/NEP) Candidates

- 5.2 By Indication

- 5.2.1 Heart Failure - Reduced EF (HFrEF)

- 5.2.2 Heart Failure - Preserved/Borderline EF (HFpEF/HFmrEF)

- 5.2.3 Systemic Hypertension

- 5.2.4 Pain & CNS Disorders

- 5.2.5 Alzheimer's & Cognitive Disorders

- 5.3 Dosage form

- 5.3.1 Tablets

- 5.3.2 Suspension

- 5.3.3 Injectables

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online & Specialty Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AbbVie Inc

- 6.3.2 Amgen Inc

- 6.3.3 AstraZeneca plc

- 6.3.4 Bayer AG

- 6.3.5 Bristol Myers Squibb

- 6.3.6 Cipla Ltd

- 6.3.7 Daiichi Sankyo

- 6.3.8 Eli Lilly & Co

- 6.3.9 GlaxoSmithKline (GSK)

- 6.3.10 Johnson & Johnson

- 6.3.11 Laurus Labs

- 6.3.12 Merck & Co.

- 6.3.13 Novartis International AG

- 6.3.14 Pfizer Inc

- 6.3.15 Regeneron Pharmaceuticals

- 6.3.16 Sanofi SA

- 6.3.17 Takeda Pharma

- 6.3.18 Teva Pharmaceutical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment