PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061654

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061654

Spray Drying Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

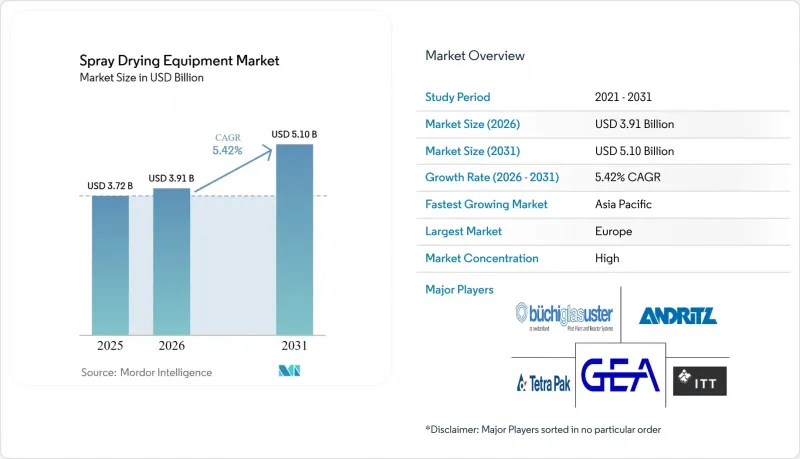

According to Mordor Intelligence, the spray drying equipment market size is expected to grow from USD 3.72 billion in 2025 to USD 3.91 billion in 2026 and is forecast to reach USD 5.1 billion by 2031 at 5.42% CAGR over 2026-2031.

This report is Segmented by Drying Stage (Single-Stage, Two-Stage and Multi-Stage), Process (Rotary Wheel, Centrifugal/Spin Disc and More), Application (Dairy Products, Infant Formula, Pharmaceuticals and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Spray Drying Equipment Market Trends and Insights

Rising demand for processed and instant foods

The global shift toward convenience foods is actively driving a significant transformation in the demand for spray drying equipment. Manufacturers are heavily investing in this technology, with instant coffee and powdered dairy products leading the way due to their widespread consumer demand. Food producers are increasingly adopting spray drying not only to extend the shelf life of their products but also to preserve their nutritional value, particularly for heat-sensitive vitamins and proteins that are essential for maintaining product quality. This technology plays a crucial role in creating free-flowing powders with controlled particle size distribution, which is critical for ensuring consistency and quality in instant beverages and ready-to-eat meal components. Furthermore, the growing preference for clean-label products is accelerating the adoption of spray drying. This method enables the production of additive-free powders, offering a distinct advantage over alternative preservation techniques by meeting consumer demands for healthier and more natural food options.

Mounting demand for high-soluble infant formula powders

Spray drying technology plays a pivotal role in the production of infant formula, ensuring the powders are nutritionally complete and adhere to stringent safety standards set by the WHO and FDA. Under the FDA's 21 CFR Part 106 regulations, infant formula production is subject to rigorous quality control measures . These include validating equipment and thermal processing, both of which increasingly favor advanced spray drying systems. In response, manufacturers are turning to specialized spray dryers. These advanced systems not only uphold protein functionality but also meet the high solubility rates sought after in contemporary infant nutrition formulations. Furthermore, the technology's prowess in encapsulating delicate nutrients, such as DHA and probiotics, without subjecting them to thermal degradation, is propelling a surge in premium equipment sales. This trend is especially pronounced in the Asia-Pacific markets, buoyed by rising birth rates and increasing disposable incomes that bolster formula consumption.

Growing demand for cost effective drying technologies

Economic pressures are driving manufacturers to evaluate alternative drying technologies that offer lower capital and operating costs compared to traditional spray drying systems. Technologies such as freeze-drying and fluidized bed drying are gaining traction as viable alternatives, particularly in applications where manufacturers can prioritize energy efficiency over shorter processing times without significantly compromising product quality. In emerging markets, small and medium-sized manufacturers are actively adopting hybrid drying systems. These systems integrate spray drying with more cost-effective pre-concentration steps, enabling manufacturers to reduce overall equipment investment while still maintaining the desired product quality. The financial constraints are especially pronounced in commodity food applications, where intense margin pressures limit the ability to invest in new equipment. As a result, manufacturers in this segment are extending the operational lifecycles of their existing equipment and delaying the adoption of advanced technologies to manage costs effectively.

Other drivers and restraints analyzed in the detailed report include:

- Growth of plant-based and alternative protein ingredients

- Strong growth in dairy industry

- Stringent Volatile Organic Compound (VOC) and particulate emission norms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, single-stage dryers dominated the spray drying equipment market, accounting for a significant 51.44% market share. These dryers are widely used due to their cost-effectiveness and simpler design, making them suitable for applications where basic drying requirements are sufficient. Industries such as food and beverages, pharmaceuticals, and chemicals frequently utilize single-stage dryers for their efficiency in handling large volumes of material with relatively low operational complexity. Additionally, their lower maintenance requirements compared to multi-stage systems make them a preferred choice for manufacturers aiming to optimize operational costs.

Multi-stage technology is projected to achieve the fastest growth rate, with a CAGR of 6.43% by 2031. This growth is driven by the increasing demand for advanced drying solutions that ensure higher product quality and energy efficiency. Multi-stage dryers are particularly favored in industries requiring precise control over moisture content and particle size, such as specialty chemicals and high-value food products. Furthermore, the integration of advanced automation and control systems in multi-stage dryers enhances their operational efficiency, making them a critical component in meeting the evolving demands of end-user industries.

Geography Analysis

In 2025, Europe leads the spray drying equipment market with a 32.96% global share, supported by a well-established pharmaceutical manufacturing base and stringent regulatory standards that promote the adoption of advanced, FDA-aligned spray drying technologies. Germany plays a pivotal role in this regional dominance, particularly in the dairy sector. The country produces a wide range of dairy products, including skim milk powders, whole milk powders, and other dairy-based powders. According to Eurostat (2024), Germany accounts for approximately 18.8% of Europe's total dairy output, underscoring its strong production capacity and advanced processing infrastructure. This robust dairy industry significantly drives demand for spray drying equipment across the region.

Asia-Pacific is expected to be the fastest-growing region, registering a CAGR of 6.87% through 2031. Growth is largely fueled by the modernization of China's pharmaceutical industry and its alignment with ICH guidelines, which is accelerating the adoption of global manufacturing standards. Investments in advanced API production facilities are significantly boosting demand for spray drying equipment. At the same time, countries like India are expanding the use of spray drying technologies in nutraceuticals and food processing to meet increasing consumer demand.

North America continues to hold a strong position, particularly in specialized and high-value applications such as specialty chemicals and advanced food ingredients. The United States remains a key contributor, with notable adoption in areas like inhalable drugs and controlled-release formulations, supported by ongoing investments in pharmaceutical and food processing research and development. Emerging regions, including South America and the Middle East and Africa, are also gaining momentum, primarily driven by the expansion of their food processing sectors. In South America, Brazil's growing food and beverage industry, especially in dairy processing, is accelerating the uptake of spray drying technologies. Similarly, the Middle East and Africa are experiencing increased demand due to rising production of powdered milk and coffee, highlighting new growth opportunities in these markets.

- GEA Group AG

- ITT Inc (SPX FLOW)

- Antolab Group Co., Ltd.

- ANDRITZ GROUP

- SiccaDania Group

- The Tetra Laval Group

- Changzhou Jinqiao Spray Drying and Engineering Co., Ltd.

- Pulse Drying Systems

- Buchiglas (Buchi AG)

- Moret Industries

- SSP Pvt Limited

- Yamato Scientific Co Ltd

- G. Larsson Starch Technology AB

- THORNICO A/S

- Col-Int Tech

- AKSH Engineering Systems (P) Limited

- DORST Technologies GmbH & Co. KG

- Sinitech Industries d.o.o.

- Mojj Engineering Systems ltd.

- Kerone Engineering Solutions LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for processed and instant foods

- 4.2.2 Mounting demand for high-soluble infant-formula powders

- 4.2.3 Growth of Plant-Based and Alternative Protein Ingredients

- 4.2.4 Rise in the adoption of nano-spray drying for nutraceutical micro-encapsulation

- 4.2.5 Strong Growth in the Dairy Industry

- 4.2.6 Advancements in multi-stage dryers

- 4.3 Market Restraints

- 4.3.1 Growing demand for cost-effective drying technologies

- 4.3.2 Stringent Volatile Organic Compound (VOC) and particulate emission norms

- 4.3.3 Risk of degradation in heat-sensitive ingredients during drying

- 4.3.4 Skill-gap in operating advanced multi-stage dryers in developing markets

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Drying Stage

- 5.1.1 Single-Stage

- 5.1.2 Two-Stage

- 5.1.3 Multi-Stage

- 5.2 By Process

- 5.2.1 Rotary Wheel (Pressure Nozzle)

- 5.2.2 Pneumatic Two-Fluid Nozzle

- 5.2.3 Centrifugal/Spin-Disc

- 5.2.4 Fluidized Spray Dryer

- 5.2.5 Closed-Loop (Inert Gas)

- 5.3 By Application

- 5.3.1 Dairy Products

- 5.3.2 Infant Formula

- 5.3.3 Functional and Plant-based Foods

- 5.3.4 Pharmaceuticals

- 5.3.5 Dietary Supplements

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 Spain

- 5.4.2.4 France

- 5.4.2.5 Italy

- 5.4.2.6 Netherlands

- 5.4.2.7 Sweden

- 5.4.2.8 Poland

- 5.4.2.9 Belgium

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Indonesia

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Colombia

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Morocco

- 5.4.5.6 Egypt

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GEA Group AG

- 6.4.2 ITT Inc (SPX FLOW)

- 6.4.3 Antolab Group Co., Ltd.

- 6.4.4 ANDRITZ GROUP

- 6.4.5 SiccaDania Group

- 6.4.6 The Tetra Laval Group

- 6.4.7 Changzhou Jinqiao Spray Drying and Engineering Co., Ltd.

- 6.4.8 Pulse Drying Systems

- 6.4.9 Buchiglas (Buchi AG)

- 6.4.10 Moret Industries

- 6.4.11 SSP Pvt Limited

- 6.4.12 Yamato Scientific Co Ltd

- 6.4.13 G. Larsson Starch Technology AB

- 6.4.14 THORNICO A/S

- 6.4.15 Col-Int Tech

- 6.4.16 AKSH Engineering Systems (P) Limited

- 6.4.17 DORST Technologies GmbH & Co. KG

- 6.4.18 Sinitech Industries d.o.o.

- 6.4.19 Mojj Engineering Systems ltd.

- 6.4.20 Kerone Engineering Solutions LTD.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK