PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061658

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061658

Optical Coherence Tomography (OCT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

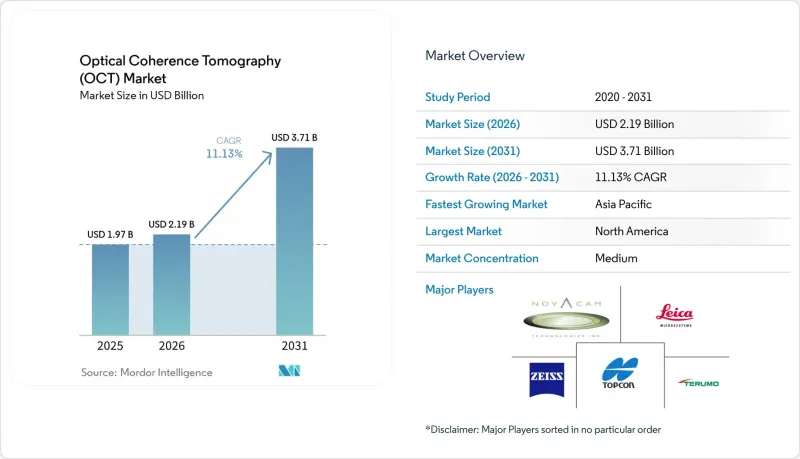

According to Mordor Intelligence, the optical coherence tomography (OCT) market size was valued at USD 1.97 billion in 2025 and is estimated to grow from USD 2.19 billion in 2026 to reach USD 3.71 billion by 2031, at a CAGR of 11.13% during the forecast period (2026-2031).

This report is Segmented by Device Type (Hand-Held OCT Devices, Table-Top OCT Devices, and More), by Technology (Time-Domain OCT, Spectral-Domain OCT, and More), by Modality (Structural OCT, OCT-Angiography (OCT-A), and More), by End-User (Hospitals & Tertiary Care Centers, and More), by Sales Channel (Direct Sales, and More), by Geography (North America, Europe, Asia-Pacific, and More).

Global Optical Coherence Tomography (OCT) Market Trends and Insights

AI-enabled quantitative biomarkers unlock new clinical indications

AI transforms OCT from descriptive imaging to predictive diagnostics. More than 1,000 AI-enabled medical devices have received FDA clearance, including the Notal Vision Home OCT platform. Zeiss launched its Research Data Platform in 2025 to automate data capture and analytics, supporting rapid research cycles. Recent Nature studies show retinal microvascular metrics derived from OCT-angiography can stratify cardiovascular risk with high accuracy. Oncology research demonstrates virtual biopsies with micro-registered OCT reduce invasive excisions while maintaining 95.5% accuracy in basal cell carcinoma detection. Collectively, these advances expand the OCT market by opening new reimbursement pathways and specialty demand.

Miniaturized, point-of-care OCT broadens primary-care and ER use

Handheld devices shrink form-factors without sacrificing image quality. Optomed's Aurora AEYE camera, cleared by the FDA in 2024, enables non-dilated diabetic-retinopathy screening in family clinics with 92-93% sensitivity. AI Optics' Sentinel scanner ships with embedded analytics and EHR connectivity to streamline referrals. Research teams at the University of Southern California prototype portable OCT otoscopes delivering 38-µm resolution of the middle ear. A USD 20 million ARPA-H grant to Washington University funds photonic-integrated-circuit OCT systems targeting 50-fold speed gains, signalling sustained innovation investment. These solutions mitigate specialist shortages in rural settings and reinforce long-term volume growth for the OCT market.

High capital cost and steep learning curve

Acquisition prices remain substantial, limiting uptake in lower-income regions. Zeiss reported a 3% revenue decline in China during fiscal 2024 as hospitals deferred big-ticket imaging purchases. Operator training needs add friction: interventionalists cite skill deficits as a barrier to routine OCT-guided PCI despite proven outcomes. Health-spending disparities are stark; OECD data show lower-middle-income Asia-Pacific countries invest USD 285 per capita compared to USD 3,891 in high-income peers. These economic and educational gaps temper near-term growth even as longer-term benefits remain clear.

Other drivers and restraints analyzed in the detailed report include:

- Geriatric eye-disease burden (AMD, glaucoma, DR)

- Rapid adoption of SS-OCT in cardiology & oncology

- Supply-chain dependence on swept-source lasers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Table-top systems retained 61.62% revenue share in 2025 because retina specialists and tertiary hospitals rely on high-resolution imaging to guide therapy. In contrast, handheld units are growing at 13.02% CAGR through 2031 as primary-care adoption widens and emergency rooms seek rapid triage capability. Handheld devices provide clinicians with sub-10-second acquisition and AI-guided interpretation, eliminating the need for dilation in diabetic-eye screening. Catheter-based intravascular OCT remains small yet essential; Abbott's Dragonfly OpStar catheter improved deliverability in tortuous coronary anatomy while sharpening image fidelity. The OCT market continues to bifurcate between full-feature consoles and ultralight probes that fit tight budgets or portable workflows.

The transition toward miniaturization mirrors broader telehealth trends. Research prototypes that integrate photonic-integrated circuits promise to slash component counts and cost, encouraging mass-volume production. AI-embedded handhelds reduce operator dependency by automating segmentation and diagnosis, which lowers training barriers for family physicians. This accessibility builds incremental procedure volume that directly enlarges the OCT market, especially in regions with sparse specialist coverage.

Spectral-domain systems dominated with 66.75% market share in 2025, supported by mature reimbursement codes and established clinical guidelines. Swept-source platforms, however, are pacing at a 12.31% CAGR to 2031 thanks to deeper tissue penetration, higher scan speeds, and artifact reduction. The OCT market size derived from swept-source revenue is anticipated to expand to USD 1.59 billion by 2031, reflecting rapid cath-lab and oncology deployment. Component innovation from Thorlabs, which released MEMS-VCSEL lasers sweeping up to 1 MHz, underpins this growth. Superluminescent diodes are gaining favor as low-coherence sources for dermatology, reducing speckle without costly tunable lasers.

Photonic-integrated-circuit advances may eventually democratize swept-source performance within compact footprints. Coherent reported double-digit growth in health-care optics on the back of AI server demand, suggesting cross-sector economies of scale will lower OCT bill-of-materials over time. Vendors retrofit spectral-domain consoles with speed-boosting upgrades to defend installedbases; Heidelberg Engineering's SHIFT firmware halves scan acquisition time, illustrating how incumbents extend product lifecycles without hardware swaps. These combined dynamics keep spectral-domain units relevant while redirecting new capital expenditure toward swept-source innovations that future-proof clinical workflows.

Geography Analysis

North America held 42.33% revenue share in 2025 thanks to advanced infrastructure, robust private insurance, and a clear FDA AI policy roadmap. Nevertheless, reimbursement headwinds persist: Medicare's 2025 Physician Fee Schedule cut ophthalmology payments by 2%, and the conversion factor fell to USD 32.35, squeezing margins for small practices. New CPT codes for OCT-angiography partially offset cuts, yet relative-value downgrades for structural imaging heighten cost-containment pressure. Canada and Mexico represent white-space opportunities where handheld devices mitigate rural-care gaps, and cross-border teleophthalmology programs capture incremental volume.

Europe maintains steady growth powered by coordinated health systems and accelerated AI adoption. EssilorLuxottica's 80% stake in Heidelberg Engineering integrates diagnostic platforms with eyewear retail channels, enhancing access in Germany, the United Kingdom, France, Italy, and Spain. Olympus secured CE approval for three cloud-based AI endoscopy systems, underscoring regulatory openness to software-driven innovation. Central and Eastern European governments are investing in hospital-modernization schemes that favor mid-range OCT consoles, sustaining baseline demand even as western markets mature.

Asia-Pacific is the fastest-growing region, advancing at a 15.06% CAGR between 2026 and 2031. China remains the largest single market but experienced capital-spending delays amid macroeconomic uncertainty, causing a 3% revenue dip for Zeiss in 2024. Japan's urban-rural physician imbalance constrains rural OCT installations despite otherwise modern infrastructure. India, Australia, and South Korea exhibit strong double-digit unit growth driven by public-health initiatives and telemedicine expansion. Singapore's SG$200 million AI-healthcare fund and Australia's 2023-2028 digital strategy further validate the region's technology-friendly policy environment. These drivers collectively boost the OCT market through rapid capacity build-out, especially for point-of-care formats.

- Abbott / LightLab Imaging

- Agfa HealthCare

- Bausch + Lomb

- Canon

- Carl Zeiss

- Gentuity

- Heidelberg Engineering

- Intalight

- Danaher

- Nidek

- Novacam Technologies

- Optovue (Visionix)

- OPTOPOL Technology

- Philophos

- SpectraWAVE

- Santec Corp.

- Terumo

- Thorlabs

- Topcon

- Wasatch Photonics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-enabled quantitative biomarkers unlock new clinical indications

- 4.2.2 Miniaturized, point-of-care OCT broadens primary-care & ER use

- 4.2.3 Geriatric eye-disease burden (AMD, glaucoma, DR)

- 4.2.4 Rapid adoption of SS-OCT in cardiology & oncology

- 4.2.5 Reimbursement expansion for ophthalmic imaging

- 4.2.6 Integration with robotic & image-guided surgery suites

- 4.3 Market Restraints

- 4.3.1 High capital cost & steep learning curve

- 4.3.2 Patchy reimbursement in dermatology & dentistry

- 4.3.3 Supply-chain dependence on swept-source lasers

- 4.3.4 Regulatory hurdles for AI-driven algorithms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Hand-held OCT Devices

- 5.1.2 Table-top OCT Devices

- 5.1.3 Catheter-based Intravascular OCT

- 5.2 By Technology

- 5.2.1 Time-Domain OCT

- 5.2.2 Spectral-Domain OCT

- 5.2.3 Swept-Source OCT

- 5.2.4 Full-Field / Line-Field OCT

- 5.3 By Modality

- 5.3.1 Structural OCT

- 5.3.2 OCT-Angiography (OCT-A)

- 5.3.3 Polarization-Sensitive OCT

- 5.3.4 Doppler / Functional OCT

- 5.4 By End-user

- 5.4.1 Hospitals & Tertiary Care Centers

- 5.4.2 Specialty Ophthalmic Clinics

- 5.4.3 Ambulatory Surgical / Cardiac Cath Labs

- 5.4.4 Dermatology & Aesthetic Clinics

- 5.4.5 Research & Academic Institutes

- 5.5 By Sales Channel

- 5.5.1 Direct Sales

- 5.5.2 Distributor / VAR Sales

- 5.5.3 Others

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott / LightLab Imaging

- 6.3.2 Agfa HealthCare

- 6.3.3 Bausch + Lomb

- 6.3.4 Canon Medical Systems

- 6.3.5 Carl Zeiss Meditec AG

- 6.3.6 Gentuity

- 6.3.7 Heidelberg Engineering

- 6.3.8 Intalight

- 6.3.9 Leica Microsystems (Danaher)

- 6.3.10 NIDEK Co., Ltd.

- 6.3.11 Novacam Technologies

- 6.3.12 Optovue (Visionix)

- 6.3.13 OPTOPOL Technology

- 6.3.14 Philophos

- 6.3.15 SpectraWAVE

- 6.3.16 Santec Corp.

- 6.3.17 Terumo Medical

- 6.3.18 Thorlabs

- 6.3.19 Topcon Corporation

- 6.3.20 Wasatch Photonics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment