PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061683

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061683

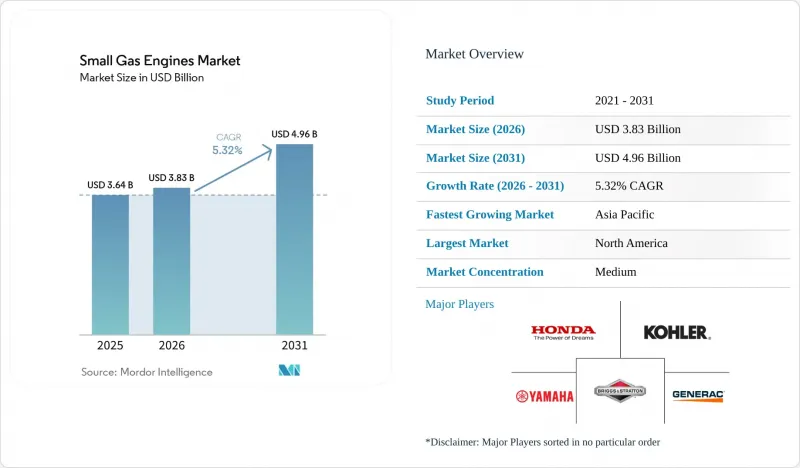

Small Gas Engines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, small gas engines market size in 2026 is estimated at USD 3.83 billion, growing from 2025 value of USD 3.64 billion with 2031 projections showing USD 4.96 billion, growing at 5.32% CAGR over 2026-2031.

This report is Segmented by Engine Displacement (20 To 100cc, 101 To 400cc, and 401 To 650cc), Equipment Type (Lawnmower, Chainsaw/Trimmer/Blower, Portable Generator, and Pressure Washer/Pump/Screed), End-Use Sector (Residential Gardening and OPE, Industrial, and Construction Equipment), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Small Gas Engines Market Trends and Insights

Post-pandemic DIY & Lawn-Care Boom Fuels OPE Engine Demand

The home-improvement enthusiasm that began in 2024 endures as homeowners position lawn maintenance as a recurring hobby and a property value enhancer. Sales of push and ride-on mowers with mid-range 101-400 cc engines remain elevated as suburban consumers replace their ageing fleets sooner than historical norms. Dealer surveys indicate spring stockouts of 14-21 days for key mower models, suggesting a persistent backlog despite the normalization of supply chains. Professional landscaping firms simultaneously report higher equipment turnover because tighter labor markets make reliability critical. Briggs & Stratton's relocation of V-Twin Vanguard production from Japan to Georgia and Alabama underscores confidence that North American demand will remain structurally higher over the medium term.

Extreme-Weather-Driven Rise in Portable-Generator Purchases

Grid disruptions totaled 1.2 billion outage hours during the first nine months of 2024, driving the adoption of portable generators beyond traditional hurricane and wildfire seasons. Consumers now purchase small gas generator sets throughout the calendar year, compressing replenishment cycles for distributors. Generac posted a 28% surge in Q4 2024 residential generator revenue and lifted shipment guidance three times over the year. NOAA's La Nina outlook for the 2024-2025 winter signals further weather-linked demand spikes, strengthening the small gas engine market as households and small businesses prioritize immediate refueling ease over battery runtime limits.

Stage V / CARB Tier-5 Emission Compliance Costs

Upcoming Tier-5 regulations mandate 90% NOx and up to 75% particulate cuts for compact engines beginning in 2029, raising certification expenses and compelling costlier materials such as coated substrates and electronic diagnostics. Smaller brands lacking in-house test cells and software calibration teams confront disproportionate per-unit compliance costs, prompting either exit or strategic licensing. Kohler's USD 6 million settlement with CARB in 2020 over defeat-device allegations signals increasing enforcement scrutiny and underscores the financial exposure associated with non-compliance. These factors consolidate volume around players able to amortize R&D across multi-fuel portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Emerging-Market Construction Rebound (2025-2028)

- Gas Powertrains Replacing Small Diesels in UTV/Compact Equipment

- Rapid Shift to Battery-Powered OPE in Mature Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 101-400 cc bracket retained 46.30% of 2025 revenue as the category underpins walk-behind mowers, portable generators, and compact site equipment where balanced power-to-weight remains essential. This slice of the small gas engine market benefits from mature supply chains that keep per-unit costs low even after adding electronic throttle bodies and oxygen sensors. OEMs prioritize this range for R&D because electrification advances have yet to deliver equivalent torque and refill speed under heavy load profiles spanning five or more hours of continuous operation. Honda's iGX-series fuel-injection roll-out illustrates how combustion refinement extends engine relevance amid tightening standards.

The 20-100 cc tier, while contributing a more modest share, is projected to compound at 6.12% through 2031, the fastest inside the small gas engine market. Growth hinges on heightened demand for light portable inverter generators and emerging-market uptake of micro-tillers and backpack sprayers. This category also feels the strongest battery encroachment, which prompts engine makers to emphasize quick-start systems, ethanol-compatible carburetors, and cost-effective catalyst packages. In contrast, the 401-650 cc range caters to commercial zero-turn mowers and standby generators, where higher ticket prices help offset compliance-system costs, preserving positive margins even under stricter standards.

Geography Analysis

North American demand continues to hinge on property size, emergency preparedness, and entrenched consumer preference for immediate refueling convenience. Small gas engines remain the power source of choice for 70% of new riding-mower sales despite rising cordless adoption in walk-behind categories. Grid instability, evidenced by a cumulative 1.2 billion outage hours logged during the first nine months of 2024, keeps portable-generator shelves thin year-round, prompting retailers to secure additional forward inventory. OEM adherence to EPA Phase III evaporative standards raises component cost but tightens quality, reinforcing domestic brand loyalty. CARB Tier-5 proposals, when finalized, will likely compel additional evaporative-emission canister capacity and durability warranties, favoring larger incumbents that can amortize compliance engineering across multiple power classes.

Asia-Pacific's role as the fastest-growing region intensifies as construction ministries commit to multi-year urban rail, road, and airport modernization plans. Gasoline engines claim share from small diesels in mini excavators and site generators because import duties on after-treatment hardware inflate diesel total cost of ownership. Middle-class yard ownership expands in peri-urban China, India, and Thailand, raising shipments of rotary mowers and trimmers fitted with 125-160 cc engines. Domestic component localization programs, such as India's Production-Linked Incentive scheme for machinery, catalyze crankshaft forging and cylinder-block casting capacity, anchoring regional supply chains and reducing lead times from 90 to 45 days. Generac's Indian joint venture expects to grow assembly output by 35% annually through 2027, underscoring the strategic importance of local presence.

Europe records lower absolute unit volumes yet exerts outsized regulatory influence because Stage V limits have become the template for forthcoming rules elsewhere. STIHL's German battery cell expansion aims to shift one-quarter of handheld tool production to cordless formats by 2027, but high-powered zero-turn mowers and hill-climb forestry winches still rely on gasoline engines. Government subsidies for zero-emission landscaping converge with municipality noise bylaws, accelerating combustion displacement in urban cores. However, rural municipalities and alpine regions continue purchasing gas-powered snowblowers and stump grinders where battery energy density remains inadequate. Currency fluctuations between EUR and USD tighten European OEM margins when sourcing aluminum castings from outside the bloc, prompting more in-region smelter contracts.

- Briggs & Stratton Corp.

- Kohler Co.

- Honda Motor Co. Ltd.

- Yamaha Motor Corp.

- Kawasaki Heavy Industries

- Kubota Corp.

- Generac Holdings Inc.

- Husqvarna Group

- Deere & Company

- Champion Power Equipment

- Cummins Inc. (Onan)

- Loncin Motor Co.

- LCT (Liquid Combustion Technology)

- STIHL Group

- Toro Company

- Atlas Copco AB

- Caterpillar Inc.

- Wacker Neuson SE

- Subaru Industrial Power (Robin)

- MTD Products (Stanley Black & Decker)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-pandemic DIY & lawn-care boom fuels OPE engine demand

- 4.2.2 Extreme-weather-driven rise in portable-generator purchases

- 4.2.3 Emerging-market construction rebound (2025-2028)

- 4.2.4 DIY "repower" kits lengthen equipment life cycles

- 4.2.5 Gas powertrains replacing small diesels in UTV/compact equipment

- 4.2.6 Off-grid recreational power surge (RV & camping)

- 4.3 Market Restraints

- 4.3.1 Stage V / CARB Tier-5 emission compliance costs

- 4.3.2 Rapid shift to battery-powered OPE in mature economies

- 4.3.3 Tariffs on Chinese lawn & garden equipment inflate prices

- 4.3.4 Shortage of certified small-engine technicians globally

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Consumers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Engine Displacement

- 5.1.1 20 to 100 cc

- 5.1.2 101 to 400 cc

- 5.1.3 401 to 650 cc

- 5.2 By Equipment Type

- 5.2.1 Lawnmower

- 5.2.2 Chainsaw/Trimmer/Blower

- 5.2.3 Portable Generator

- 5.2.4 Pressure Washer/Pump/Screed

- 5.3 By End-Use Sector

- 5.3.1 Residential Gardening and OPE

- 5.3.2 Industrial (Portable Power, Pumps, Welding)

- 5.3.3 Construction Equipment

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Briggs & Stratton Corp.

- 6.4.2 Kohler Co.

- 6.4.3 Honda Motor Co. Ltd.

- 6.4.4 Yamaha Motor Corp.

- 6.4.5 Kawasaki Heavy Industries

- 6.4.6 Kubota Corp.

- 6.4.7 Generac Holdings Inc.

- 6.4.8 Husqvarna Group

- 6.4.9 Deere & Company

- 6.4.10 Champion Power Equipment

- 6.4.11 Cummins Inc. (Onan)

- 6.4.12 Loncin Motor Co.

- 6.4.13 LCT (Liquid Combustion Technology)

- 6.4.14 STIHL Group

- 6.4.15 Toro Company

- 6.4.16 Atlas Copco AB

- 6.4.17 Caterpillar Inc.

- 6.4.18 Wacker Neuson SE

- 6.4.19 Subaru Industrial Power (Robin)

- 6.4.20 MTD Products (Stanley Black & Decker)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment