PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061684

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061684

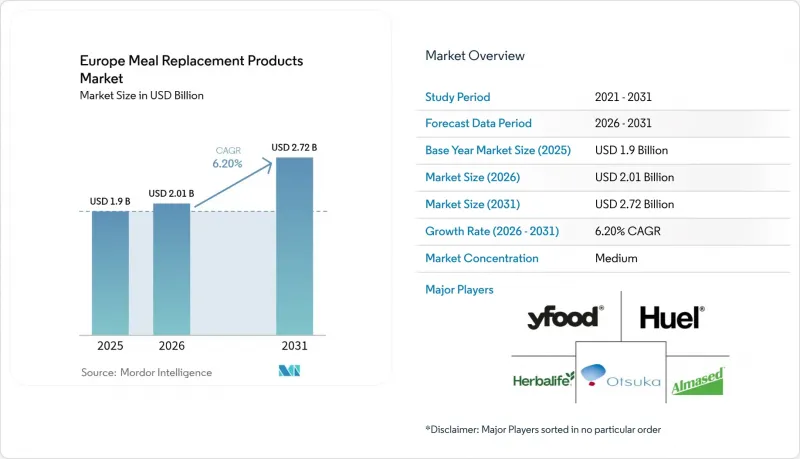

Europe Meal Replacement Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe meal replacement products market size is projected to be USD 1.90 billion in 2025, USD 2.01 billion in 2026, and reach USD 2.72 billion by 2031, growing at a CAGR of 6.20% from 2026 to 2031.

This report is Segmented by Product Type (Powdered Products, Ready-To-Drink Products, Nutritional Bars, and More), Packaging Format (Bottles/Jars, Pouches, Tetra Packs and Cartons, and Others), Nature (Conventional and Organic), Distribution Channel (Supermarkets/Hypermarkets, and More), and Geography (Germany, United Kingdom, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Meal Replacement Products Market Trends and Insights

Health-Conscious Consumers Embrace Protein-Rich Alternatives

European consumers increasingly prioritize protein-rich nutrition solutions, with 45% of health-focused individuals specifically citing increased protein consumption as a dietary goal. This trend extends beyond traditional fitness enthusiasts to encompass mainstream consumers seeking satiety, weight management, and muscle support benefits. The protein fortification movement now spans categories previously untouched by nutritional enhancement, including ice cream, cakes, and breakfast cereals, indicating market maturation beyond conventional shake formats. Novel protein sources gain regulatory acceptance, with the European Commission authorizing UV-treated yellow mealworm powder in January 2025 for use in bread, pasta, and processed foods, expanding ingredient options for manufacturers . The convergence of flexitarian dietary patterns with protein consciousness creates sustained demand for plant-based and hybrid protein formulations that deliver both nutritional density and environmental sustainability credentials.

Convenient Product Formats Drive Adoption of Meal Replacement Solutions

Format innovation accelerates adoption as consumers demand nutrition solutions that integrate seamlessly with mobile lifestyles and hybrid work patterns. Ready-to-drink formats capture market momentum by eliminating preparation barriers, particularly appealing to time-constrained professionals and urban commuters who prioritize immediate consumption capability. The shift toward convenience extends beyond liquid formats to include portion-controlled bars, single-serve packets, and ambient-stable formulations that require no refrigeration or mixing equipment. Tetra Pak's Industrial Protein Mixer addresses foaming challenges during liquid production, enabling manufacturers to reduce product loss by over EUR 250,000 annually while extending shelf life and improving operational efficiency. This technological advancement directly supports the scalability of convenient liquid formats that drive category growth across European markets.

Raw Material Shortages Disrupt Supply Chain

Supply chain vulnerabilities intensify as geopolitical tensions and climate events disrupt critical ingredient flows, with sunflower lecithin shortages exemplifying systemic risks facing European manufacturers. The Russia-Ukraine conflict eliminated over 50% of global sunflower seed production, causing lecithin prices to increase 3-4x and forcing widespread reformulation efforts across the industry. European protein ingredient supply faces additional pressure from import dependency, with EU self-sufficiency at only 3% for high-protein crops like soybean meal, exposing manufacturers to price volatility and trade disruptions . China's dominance in vitamin and amino acid supply chains creates concentration risk, supplying over 70% of vitamins and 75% of lysine globally, making European meal replacement manufacturers vulnerable to supply disruptions and regulatory changes. The European Commission's protein strategy initiatives aim to boost domestic production through CAP support measures, but structural constraints including land availability and competitiveness challenges limit near-term supply security improvements.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Wellness Programs Support Meal Replacements

- Technology Advances Enhance Product Quality

- Regulations Constrain Product Development and Marketing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soup products emerge as the fastest-growing segment with 10.02% CAGR through 2031, despite powdered products maintaining market leadership at 39.59% share in 2025. This growth differential reflects a culturally significant segment in markets with strong soup traditions like Germany and Eastern Europe. Nutritional Bars capture a steady market position by addressing portion control and portability needs, while the ready-to-drink format preference evolves toward immediate consumption convenience, particularly among urban professionals and mobile consumers who prioritize grab-and-go nutrition solutions.

The segment dynamics reveal a fundamental shift in consumption patterns as European lifestyles increasingly favor convenience over preparation time. Tetra Pak's development of specialized protein mixing technology addresses foaming challenges in liquid production, enabling manufacturers to scale RTD formats while maintaining product quality and extending shelf life. Other Product Types, including emerging formats like protein-enriched snacks and functional beverages, gain traction as manufacturers expand beyond traditional meal replacement categories to capture broader nutrition occasions throughout the day.

Tetra Packs and Cartons demonstrate the highest growth trajectory at 7.49% CAGR through 2031, challenging the dominance of bottles/jars, which hold 32.33% market share in 2025. This shift reflects mounting sustainability pressures and technological breakthroughs in paper-based packaging that maintain product integrity while reducing environmental impact. Tetra Pak's paper-based barrier technology, validated through large-scale trials with Lactogal in Portugal, achieves up to 33% carbon footprint reduction while increasing renewable content to 90%.

Pouches maintain steady growth by offering lightweight, flexible packaging solutions that optimize logistics costs and shelf space efficiency. The packaging evolution extends beyond environmental considerations to encompass e-commerce optimization, with formats designed for shipping durability and consumer unboxing experience becoming increasingly important as online retail channels expand. The other category includes emerging packaging innovations such as recyclable single-serve sachets and biodegradable containers that address specific market niches and regulatory requirements across different European jurisdictions.

List of Companies Covered in this Report:

- Abbott Laboratories

- Almased GmbH

- YFood Labs GmbH

- Glanbia Plc

- Fresenius Kabi Deutschland GmbH

- Mars Inc.

- Nestle S.A.

- Danone S.A.

- Herbalife Nutrition Ltd.

- Enervit S.p.A.

- Heaven Labs (Mana)

- Amway Corporation

- Jimmy Joy

- LighterLife

- Huel Ltd

- Orkla Group (Nutrilett)

- Certmedica International GmbH (Farmoline)

- Naturhouse Health, S.A.

- Otsuka Holdings Co Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Health-Conscious Consumers Embrace Protein-Rich Alternatives

- 4.2.2 Convenient Product Formats Drive Adoption of Meal Replacement Solutions

- 4.2.3 Corporate Wellness Programs Support Meal Replacements

- 4.2.4 Portion Control Awareness Increases Product Adoption

- 4.2.5 Technology Advances Enhance Product Quality

- 4.2.6 E-Commerce Enhances Global Market Distribution

- 4.3 Market Restraints

- 4.3.1 Raw Material Shortages Disrupt Supply Chain

- 4.3.2 Regulations Constrain Product Development and Marketing

- 4.3.3 Consumer Concerns Over Food Additives Impact Sales

- 4.3.4 Balancing Product Freshness with Quality Standards

- 4.4 Consumer Demand Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Advancement

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Powdered Products

- 5.1.2 Ready-to-Drink Products

- 5.1.3 Nutritional Bars

- 5.1.4 Soups

- 5.1.5 Other Product Types

- 5.2 By Packaging Format

- 5.2.1 Bottles/Jars

- 5.2.2 Pouches

- 5.2.3 Tetra Packs and Cartons

- 5.2.4 Others

- 5.3 By Nature

- 5.3.1 Conventional

- 5.3.2 Organic

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Pharmacies and Health Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Other Channels

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 Italy

- 5.5.4 France

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Poland

- 5.5.8 Belgium

- 5.5.9 Sweden

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Abbott Laboratories

- 6.4.2 Almased GmbH

- 6.4.3 YFood Labs GmbH

- 6.4.4 Glanbia Plc

- 6.4.5 Fresenius Kabi Deutschland GmbH

- 6.4.6 Mars Inc.

- 6.4.7 Nestle S.A.

- 6.4.8 Danone S.A.

- 6.4.9 Herbalife Nutrition Ltd.

- 6.4.10 Enervit S.p.A.

- 6.4.11 Heaven Labs (Mana)

- 6.4.12 Amway Corporation

- 6.4.13 Jimmy Joy

- 6.4.14 LighterLife

- 6.4.15 Huel Ltd

- 6.4.16 Orkla Group (Nutrilett)

- 6.4.17 Certmedica International GmbH (Farmoline)

- 6.4.18 Naturhouse Health, S.A.

- 6.4.19 Otsuka Holdings Co Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK