PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061690

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061690

Asia-Pacific Aircraft Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

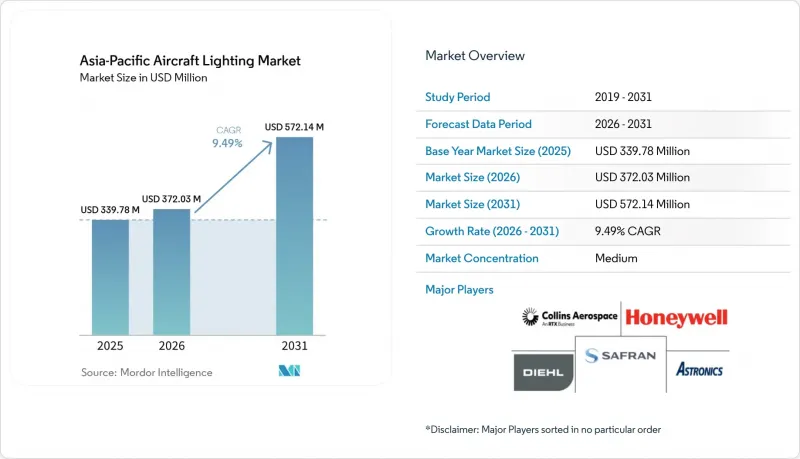

According to Mordor Intelligence, the asia-Pacific aircraft lighting market size is expected to grow from USD 339.78 million in 2025 to USD 372.03 million in 2026, and is forecasted to reach USD 572.14 million by 2031 at a 9.49% CAGR over 2026-2031.

This report is Segmented by Lighting Type (Interior Lighting and Exterior Lighting), Aircraft Type (Narrowbody Aircraft, Widebody Aircraft, Regional Jets, Business Jets, and More), Fit (Linefit and Retrofit), Technology (LED, Fluorescent, and More), and Geography (China, India, Japan, South Korea, Australia, Singapore, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Aircraft Lighting Market Trends and Insights

Sustained LED-retrofit wave across APAC commercial fleets

Airlines across the region accelerated LED upgrades to cut power draw, extend maintenance intervals, and refresh cabin ambiance, with several operators standardizing on pre-certified kits to minimize aircraft downtime. Astronics reported 18.5% year-over-year growth in commercial transport sales in Q4 2025, underscoring strong demand for lighting and safety products tied to retrofit pipelines. Plug-and-play installation has proven central, with STG Aerospace indicating that liTeMood kits for major Airbus platforms can be installed in under six hours, enabling carriers to align upgrades with scheduled maintenance windows. Operators cite the long service life and controllability of LED solutions as additional drivers, as tunable lighting supports brand scenes and reduces unscheduled replacements compared with legacy technologies. Air India introduced chakra-inspired mood lighting on its first linefit B787-9 in January 2026. The airline is committed to retrofitting 26 B787-8 aircraft by mid-2027, signaling a broad shift toward wellness-aligned lighting across its mixed fleet. Singapore Airlines' multi-year A350 retrofit program, budgeted at SGD 1.1 billion (USD 869.20 million), illustrates the scale at which Asia-Pacific full-service carriers (FSCs) are refreshing cabins, with lighting upgrades embedded in larger interior programs.

OEM push for lighter, energy-efficient cabin and exterior systems

Airframers and Tier-1 suppliers are embedding lighter, power-efficient lighting into new-build programs, thereby setting a new standard that operators seek to mirror across the in-service fleet. Airbus is preparing an A350 retrofit wave as aircraft age toward key thresholds, with upgrade options such as mood-lighting software that aligns with cabin refreshes and helps standardize the passenger experience across deliveries. Collins and other Tier-1s provide linefit-ready LED solutions across Airbus, Boeing, and regional platforms, complementing digital power and control architectures that support predictive maintenance. As Chinese programs gain share in regional narrowbody demand, suppliers embedded at the linefit level, including through local partnerships, anchor multi-year spares-and-services revenue for LED components.

Up-front retrofit cost and grounding time for operators

The initial cash outlay for LED kits, installation labor, and lost revenue hours remains a headwind for carriers that run high daily utilization. LCCs are particularly sensitive to grounding time, which is why under-six-hour installation options are gaining traction on narrowbodies. Financing and balance-sheet constraints also shape timing for cabin investments when macro conditions tighten or when engine and component backlogs push up maintenance reserves. Airlines try to mitigate these costs by aligning retrofits with planned checks and by using supplemental type certificate packages that streamline engineering and regulatory steps. Even so, smaller operators may defer lighting retrofits to conserve cash, which slows adoption compared with FSCs that monetize premium cabins. Over time, fuel and maintenance savings improve the payback case, supporting broader uptake once aircraft have scheduled downtime.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory mandates on emergency/exit lighting performance

- Record aircraft production backlogs at Airbus and COMAC

- Complex DO-160/EASA CS-25 certification hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Interior lighting systems held 61.55% share in 2025, reflecting strong use of mood lighting, ambient washes, reading lights, and emergency pathfinding that support wellness and branding. Airlines in the Asia-Pacific aircraft lighting market are standardizing tunable cabin lighting to improve sleep cycles and align service touchpoints with time-of-day scenes on long-haul flights. Emergency and exit lighting remains a regulated niche, led by photoluminescent and LED solutions, supported by established approvals and an extensive global installed base. The Asia-Pacific aircraft lighting market also includes lavatory and galley task-lighting upgrades, where small changes improve crew workflow and customer satisfaction as part of broader refurbishments. Cockpit lighting remains smaller in revenue but critical in reliability and human factors, where precise beam control and longevity are key selection criteria.

Exterior systems are expected to post the fastest growth, with a 9.89% CAGR through 2031, as authorities enforce visibility and anti-collision thresholds and power-efficient LEDs replace xenon and halogen units. Suppliers offer navigation, position, landing, taxi, and strobe solutions with stable photometrics and long life to cut unscheduled removals and keep aircraft in service. Branding-oriented logo lighting and wing inspection lights gain attention for reliability and color accuracy, especially for carriers with high night operations. Combined with digital cabin power and monitoring, exterior LED packages simplify line maintenance and reduce the variety of spares within mixed fleets. Asia-Pacific carriers link these changes to safety and sustainability goals, building a strong pipeline for both linefit and retrofit over the forecast horizon.

Narrowbodies captured 56.76% of 2025 revenues as short-haul frequency, route density, and fleet standardization make cabin and exterior LED upgrades a high-ROI priority. kits that improve energy efficiency and reduce maintenance touchpoints are particularly attractive for high-cycle single-aisle aircraft in the Asia-Pacific aircraft lighting market. Twin-aisle aircraft serve premium long-haul routes, where mood lighting creates measurable brand value and supports wellness positioning, leading to higher per-aircraft spend for interior systems. The Asia-Pacific aircraft lighting market is further reinforced by widebody refreshes that align legacy cabins with new deliveries, including reading lights and long-lasting accent lighting.

Regional jets are poised for the highest growth, with a 10.95% CAGR through 2031, as secondary-city links expand and governments promote connectivity, which benefits compact LED solutions tailored to smaller cabins and lower power budgets. Business jets remain a smaller but premium segment where bespoke lighting and fast tech adoption push spend above commercial averages. Helicopter operations require ruggedized exterior lights for demanding environments, while UAVs draw interest for lightweight anti-collision beacons that meet evolving rules. As delivery delays persist, operators across these categories are leaning on retrofits to improve efficiency and preserve the passenger experience, keeping lighting demand steady across platforms.

List of Companies Covered in this Report:

- Honeywell International Inc.

- Collins Aerospace (RTX Corporation)

- Safran S.A.

- Diehl Stiftung & Co. KG

- Astronics Corporation

- KOITO MANUFACTURING CO., LTD.

- Oxley Group

- Bruce Aerospace Inc.

- Madelec Aero SAS

- S.E.L.A. Lighting Systems

- Luminator Technology Group

- Cobalt Aerospace Group Limited

- Lufthansa Technik AG

- Aveo Engineering Group, s.r.o.

- Precise Flight, Inc.

- PWI, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustained LED-retrofit wave across Asia-Pacific commercial fleets

- 4.2.2 OEM push for lighter, energy-efficient cabin and exterior systems

- 4.2.3 Regulatory mandates on emergency/exit lighting performance

- 4.2.4 Record aircraft production backlogs at Airbus and COMAC

- 4.2.5 Smart human-centric mood lighting to boost passenger wellness

- 4.2.6 Refurbishment cycles among low-cost carriers (LCCs) after COVID-19

- 4.3 Market Restraints

- 4.3.1 Up-front retrofit cost and grounding time for operators

- 4.3.2 Complex DO-160/EASA CS-25 certification hurdles

- 4.3.3 Semiconductor and specialty-LED supply-chain volatility

- 4.3.4 EMI/EMC compliance issues in high-density cabins

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Lighting Type

- 5.1.1 Interior Lighting

- 5.1.1.1 Cabin Lighting

- 5.1.1.2 Cockpit Lighting

- 5.1.1.3 Emergency and Exit Lighting

- 5.1.1.4 Cargo/Baggage Lighting

- 5.1.2 Exterior Lighting

- 5.1.2.1 Navigation and Position Lights

- 5.1.2.2 Landing and Taxi Lights

- 5.1.2.3 Anti-Collision and Strobe Lights

- 5.1.2.4 Logo and Wing Inspection Lights

- 5.1.1 Interior Lighting

- 5.2 By Aircraft Type

- 5.2.1 Narrowbody Aircraft

- 5.2.2 Widebody Aircraft

- 5.2.3 Regional Jets

- 5.2.4 Business Jets

- 5.2.5 Helicopters

- 5.2.6 Unmanned Aerial Vehicles (UAVs)

- 5.3 By Fit

- 5.3.1 Linefit

- 5.3.2 Retrofit

- 5.4 By Technology

- 5.4.1 Light-Emitting Diode (LED)

- 5.4.2 Fluorescent

- 5.4.3 Incandescent/Halogen

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Australia

- 5.5.6 Singapore

- 5.5.7 Vietnam

- 5.5.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Collins Aerospace (RTX Corporation)

- 6.4.3 Safran S.A.

- 6.4.4 Diehl Stiftung & Co. KG

- 6.4.5 Astronics Corporation

- 6.4.6 KOITO MANUFACTURING CO., LTD.

- 6.4.7 Oxley Group

- 6.4.8 Bruce Aerospace Inc.

- 6.4.9 Madelec Aero SAS

- 6.4.10 S.E.L.A. Lighting Systems

- 6.4.11 Luminator Technology Group

- 6.4.12 Cobalt Aerospace Group Limited

- 6.4.13 Lufthansa Technik AG

- 6.4.14 Aveo Engineering Group, s.r.o.

- 6.4.15 Precise Flight, Inc.

- 6.4.16 PWI, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment