PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061691

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061691

Pad-Mounted Switchgear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

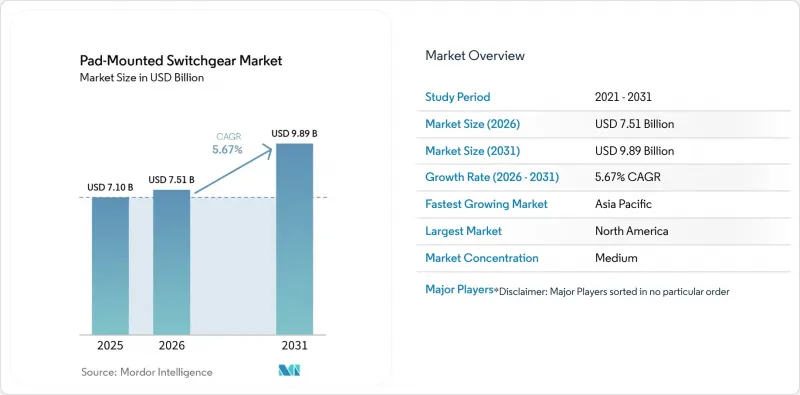

According to Mordor Intelligence, the pad-Mounted switchgear market size was valued at USD 7.10 billion in 2025 and estimated to grow from USD 7.51 billion in 2026 to reach USD 9.89 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031).

This report is Segmented by Insulating Medium (Air, Gas, Fluids, and Solid Materials), Application (Industrial, Commercial, and Residential), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Pad-Mounted Switchgear Market Trends and Insights

Grid-modernization undergrounding

Underground distribution now commands sizable utility capex as overhead systems struggle to survive extreme weather events. The U.S. Department of Energy allocated USD 34 million to the GOPHURRS program, signifying federal endorsement of below-grade distribution that reduces storm-related outages. Underground line costs range from USD 1.1 million to USD 62 million per kilometer, creating a substantial addressable market for pad-mounted switchgear. U.S. underground line share rose from 18% in 2009 to roughly 20% in 2023, and Pacific Gas & Electric plans to bury 10,000 miles of circuits, each mile requiring several pad-mounted units for sectionalizing and protection. These projects translate into multi-year procurement pipelines that insulate the pad-mounted switchgear market from cyclical downturns.

SF6-free technology shift

Climate policy now bans SF6 in new medium-voltage gear across the EU from January 2026 and across California by 2033. Because SF6 has a 25,200X CO2 warming potential, utilities must rapidly switch to vacuum, clean-air, or fluoronitrile insulation that lowers emissions up to 99%. Manufacturers that commercialize SF6-free pads win early replacement contracts and earn premium margins, while laggards face stranded portfolios. Hitachi Energy shipped the world's first SF6-free 550 kV GIS in May 2025, proving the scalability of the alternative technologies. Early adopters in Europe and California shorten testing cycles, accelerating global diffusion and bolstering the pad-mounted switchgear market.

High capital costs

Underground feeders can cost 3.5 to 8 times more than their overhead equivalents, straining utility budgets and sparking public opposition to rate hikes. In Ontario, developers pay up to USD 12,400 per all-electric home for distribution hookups, an expense that dampens green-field adoption. Municipal utilities with small rate bases often defer undergrounding, postponing pad-mounted switchgear purchases. Consequently, the pad-mounted switchgear market faces adoption gaps in lower-income regions until cost-sharing mechanisms mature.

Other drivers and restraints analyzed in the detailed report include:

- Renewable & DER interconnections

- Urban space constraints

- MV component lead-time spikes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-insulated switchgear retained 41.60% of the pad-mounted switchgear market size in 2025, thanks to established supply chains and cost advantages. Solid-dielectric variants, however, are tipped to progress at a 7.68% CAGR through 2031 as SF6 bans drive technology conversions. Gas-insulated units occupy a middle ground, benefiting from fast installation yet facing environmental scrutiny. Fluid-insulated models-using synthetic esters or natural oils-address niche fire-safe applications in dense cities.

Solid-dielectric platforms eliminate gas leakage concerns and reduce routine maintenance, making them appealing to utilities transitioning large feeder sections below grade. Operators report safer fault clearing and lower lifecycle costs compared to legacy gas units. As SF6 deadlines approach, training initiatives intensify to equip technicians with new diagnostic protocols. GIS remains attractive where land prices justify compact footprints, cutting site area up to 75% and shaving project schedules by 45%. Overall, the escalating need for environmental compliance propels solid-dielectric technology to the forefront of the pad-mounted switchgear market.

Geography Analysis

North America commands the largest revenue share at 36.10% in 2025, driven by expansive grid-hardening programs and wildfire mitigation mandates. Pacific Gas & Electric's 10,000-mile undergrounding plan, coupled with the DOE's GOPHURRS grants, sustains high single-digit annual equipment outlays. The United States alone is projected to show a 10.5% CAGR for medium-voltage switchgear through 2030, resulting in more than USD 2 billion in additions to the pad-mounted switchgear market size. Canada estimates USD 1.4 trillion in electricity investments by 2050, with half earmarked for transmission and distribution (T&D), signaling robust medium-term spending.

Asia-Pacific records the quickest advance, posting a 7.08% CAGR from 2026-2031. India plans INR 9.1 lakh crore (USD 109 billion) for transmission and distribution by 2032, a figure that incorporates significant underground feeder deployment. China leads in technology scale-up, as evidenced by State Grid's first-in-class 550 kV SF6-free GIS rollout, underscoring its regional leadership in alternative insulation adoption. Japan and South Korea utilize advanced manufacturing to export solid-dielectric units across Southeast Asia, where economic corridors, such as the Eastern Economic Corridor in Thailand, require resilient underground networks. The pad-mounted switchgear market, therefore, enjoys a broad pull in the Asia-Pacific region, rooted in the integration of renewable energy and urban electrification.

Europe experiences steady but regulation-intensive growth. The EU SF6 prohibition, effective January 2026, requires wide-scale retrofit and replacement budgets that favor domestic OEMs. Norway's six-year SF6-free framework with Siemens signals the growing appetite for green switchgear in North Europe. The UK, France, and Germany are mirroring this trend, prioritizing low-carbon equipment in their post-Brexit and post-pandemic recovery plans. In South America, transmission projects for renewable exports drive incremental demand, although financing obstacles temper volumes. The Middle East & Africa benefit from industrial diversification agendas, yet skilled labor gaps and CAPEX hurdles slow project flow. Collectively, these regional patterns reinforce diversification benefits for global suppliers to the pad-mounted switchgear market.

- ABB Ltd

- Eaton Corporation plc

- S&C Electric Company

- G&W Electric Co.

- Hubbell Power Systems Inc.

- Federal Pacific (Electro-Mechanical Corp.)

- The International Electrical Products Co. (TIEPCO)

- Powell Industries Inc.

- Schneider Electric SE

- Siemens AG

- GE Vernova Grid Solutions

- Hitachi Energy Ltd.

- CHINT Group Co. Ltd.

- Myers Power Products Inc.

- LS Electric Co. Ltd.

- Rockwill Electric Group

- Tamco Switchgear Malaysia Sdn Bhd

- NOJA Power Switchgear Pty Ltd

- Resa Power LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-modernization undergrounding

- 4.2.2 Renewable & DER interconnections

- 4.2.3 Urban space constraints

- 4.2.4 SF6-free technology shift

- 4.2.5 Microgrid build-outs

- 4.2.6 Hyperscale data-center demand

- 4.3 Market Restraints

- 4.3.1 High capital costs

- 4.3.2 MV component lead-time spikes

- 4.3.3 Safety concerns around eco-fluids

- 4.3.4 Skills gap for solid-dielectric OM

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Insulating Medium

- 5.1.1 Air

- 5.1.2 Gas (SF6 / SF6-free)

- 5.1.3 Fluids (E200, FR3)

- 5.1.4 Solid Materials

- 5.2 By Application

- 5.2.1 Industrial

- 5.2.2 Commercial

- 5.2.3 Residential

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Eaton Corporation plc

- 6.4.3 S&C Electric Company

- 6.4.4 G&W Electric Co.

- 6.4.5 Hubbell Power Systems Inc.

- 6.4.6 Federal Pacific (Electro-Mechanical Corp.)

- 6.4.7 The International Electrical Products Co. (TIEPCO)

- 6.4.8 Powell Industries Inc.

- 6.4.9 Schneider Electric SE

- 6.4.10 Siemens AG

- 6.4.11 GE Vernova Grid Solutions

- 6.4.12 Hitachi Energy Ltd.

- 6.4.13 CHINT Group Co. Ltd.

- 6.4.14 Myers Power Products Inc.

- 6.4.15 LS Electric Co. Ltd.

- 6.4.16 Rockwill Electric Group

- 6.4.17 Tamco Switchgear Malaysia Sdn Bhd

- 6.4.18 NOJA Power Switchgear Pty Ltd

- 6.4.19 Resa Power LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment