PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061694

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061694

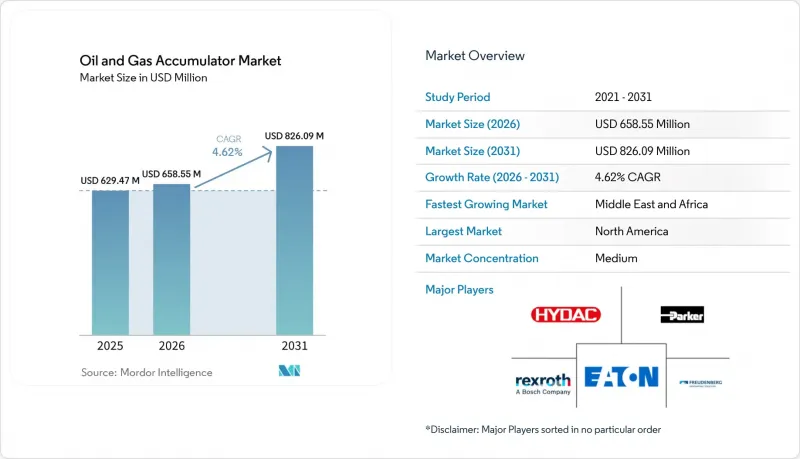

Oil And Gas Accumulator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the oil and gas accumulator market size is expected to grow from USD 629.47 million in 2025 to USD 658.55 million in 2026 and is forecast to reach USD 826.09 million by 2031 at 4.62% CAGR over 2026-2031.

This report is Segmented by Accumulator Type (Bladder, Metal Bellows, and More), Pressure Rating (Below 3, 000 Psi, and More), Capacity (Below 10 Gal, and More), Location of Deployment (Onshore and Offshore), Application (Drilling, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Oil And Gas Accumulator Market Trends and Insights

Up-cycle in Global Offshore Rig Count

Offshore rig utilisation rebounded to 82% in 2024 with 639 active units, stimulating replacement and upgrade cycles for accumulator banks that power high-spec managed-pressure drilling systems. Fleet investment now favours upgrading existing rigs over newbuilds, extending service lifetimes, and raising demand for advanced hydraulic storage capable of faster BOP actuation. Deepwater projects, forecasted to grow at 8% annually from 2025 to 2028, will continue to push the oil & gas accumulator market toward higher pressure and temperature thresholds. Floating rig awards in Latin America and West Africa, scheduled for 2025-2026, further enlarge the addressable opportunity for premium accumulator packages.

Stringent BOP Safety Mandates (API 16D)

API 16D sets minimum accumulator volume, pre-charge, and response time criteria for critical BOP functions, compelling operators to adopt high-capacity units with redundant banks. Regulatory audits now emphasize the readiness of remote-operated vehicle intervention and third-party recertification, prompting specification upgrades that favor metal bellows and piston designs rated for 20,000 psi service. Ongoing compliance cycles generate repeat revenue for OEM service divisions that supply inspection, testing, and recharge programs.

Oil-Price Volatility Curbing Drilling Budgets

Erratic commodity prices encourage operators to stretch equipment life, delaying accumulator renewals and favouring service-life extension kits over full replacements. While activity remains steady, discretionary spend on premium hydraulic upgrades contracts during price dips, tightening near-term revenue growth for suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Surging Shale Well Recompletions

- CAPEX Rebound in MENA Sour-Gas Projects

- High Recertification & ASME Code Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The oil & gas accumulator market size for bladder designs remained the largest in 2025, capturing a 47.25% share due to the strength of a mature supply chain and ease of maintenance. However, metal bellows units are set to record the fastest 5.72% CAGR, thanks to their superior fatigue resistance at 20,000 psi deployments, such as Chevron's Anchor field.

Metal bellows construction also tolerates sour-gas environments without elastomer degradation, positioning the segment for long-term growth in deep-HPHT projects. Piston and diaphragm types retain roles in niche circuits where precise volume control or fluid separation is crucial, while spring accumulators serve legacy rigs with compact space envelopes. The oil & gas accumulator industry increasingly favours modular platforms that allow operators to swap internal elements rather than replacing complete vessels, a cost-saving trend benefiting flexible OEMs.

Systems rated below 3,000 psi held a 54.45% share in 2025, primarily due to the widespread adoption of onshore drilling. Above 5,000 psi models are expected to log a 6.27% CAGR as deepwater and ultra-deepwater wells proliferate across the US Gulf and Brazil.

Higher ratings demand forged alloy shells, stricter welding procedures, and advanced NDT, driving unit prices upward but reducing total vessel count through increased capacity. At the same time, intermediate units with pressures of 3,001-5,000 psi serve proliferating shallow-water redevelopment projects, where operators upgrade aging platforms rather than sanction greenfield builds. The oil & gas accumulator market continues to pivot toward high-pressure variants that can be standardised across multiple rig classes to simplify logistics.

Geography Analysis

North America retained a 37.15% revenue lead in 2025 owing to sustained shale recompletion and a cautious offshore revival. The region's emphasis on capital efficiency and adoption of electric fracturing fleets keeps demand steady for compact, digitally monitored accumulators that integrate with real-time cloud analytics. Upstream developers in Argentina and Brazil are adding incremental growth through subsea tree awards, which require 20,000 psi solutions.

The Middle East & Africa oil & gas accumulator market size is expected to register the highest CAGR of 6.08% through 2031. Massive sour-gas projects such as Jafurah, with compression trains and thousands of kilometres of pipeline, need large-volume vessels rated for H2S service. ADNOC's rig expansion and subsea prospects off Namibia and Angola reinforce the trajectory despite temporary jack-up cancellations. Regional content mandates also motivate OEMs to localise assembly and service hubs, reducing lead times and creating new joint-venture structures.

Europe and the Asia-Pacific exhibit stable replacement-driven demand. European North Sea operators retrofit ageing rigs to meet new environmental regulations, adding sensors and leak-proof bellows to existing skids. Asia-Pacific's upstream capex, led by China and Indonesia, tops USD 300 billion in 2025 and underpins fresh orders for medium-pressure units suited to brownfield life-extension projects. Meanwhile, the growing number of carbon-storage pilots across the North Sea introduces novel accumulator roles in CO2 injection systems, opening a complementary market for corrosion-resistant designs.

- HYDAC International GmbH

- Parker-Hannifin Corp.

- Eaton Corporation plc

- Freudenberg Sealing Technologies (Tobul)

- Bosch Rexroth AG

- Nippon Accumulator Co., Ltd.

- Roth Industries LLC

- Technetics Group

- Continental Hydraulics Inc.

- Olaer Group

- Accumulators Inc.

- Hydrotechnik GmbH

- Blacoh Fluid Control

- Rotec Hydraulics Ltd.

- Eaton Filtration LLC

- Bosch Auto Accumulator Systems

- Kawasaki Hydraulics

- KYB Corporation

- Danfoss Power Solutions

- Hallite Seals International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Up-cycle in global offshore rig count

- 4.2.2 Stringent BOP safety mandates (API 16D)

- 4.2.3 Surging shale well recompletions

- 4.2.4 CAPEX rebound in MENA sour-gas projects

- 4.2.5 Retrofit programmes for low-emission electro-hydraulic units

- 4.2.6 Digital twins enabling predictive accumulator maintenance

- 4.3 Market Restraints

- 4.3.1 Oil-price volatility curbing drilling budgets

- 4.3.2 igh re-certification & ASME code compliance costs

- 4.3.3 Shift toward all-electric subsea BOPs reducing hydraulic scope

- 4.3.4 ESG pressure on hydraulic-fluid spill risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Accumulator Type

- 5.1.1 Bladder

- 5.1.2 Piston

- 5.1.3 Diaphragm

- 5.1.4 Metal Bellows

- 5.1.5 Spring and Others

- 5.2 By Pressure Rating

- 5.2.1 Below 3,000 psi

- 5.2.2 3,001 to 5,000 psi

- 5.2.3 Above 5,000 psi

- 5.3 By Capacity

- 5.3.1 Below 10 gal

- 5.3.2 10 to 50 gal

- 5.3.3 Above 50 gal

- 5.4 By Location of Deployment

- 5.4.1 Onshore

- 5.4.2 Offshore

- 5.5 By Application

- 5.5.1 Drilling

- 5.5.2 Well Workover and Intervention

- 5.5.3 Blowout Preventer Control Units

- 5.5.4 Hydraulic Fracturing Units

- 5.5.5 Other Upstream Operations

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 Norway

- 5.6.2.5 Russia

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Qatar

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Nigeria

- 5.6.5.7 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 HYDAC International GmbH

- 6.4.2 Parker-Hannifin Corp.

- 6.4.3 Eaton Corporation plc

- 6.4.4 Freudenberg Sealing Technologies (Tobul)

- 6.4.5 Bosch Rexroth AG

- 6.4.6 Nippon Accumulator Co., Ltd.

- 6.4.7 Roth Industries LLC

- 6.4.8 Technetics Group

- 6.4.9 Continental Hydraulics Inc.

- 6.4.10 Olaer Group

- 6.4.11 Accumulators Inc.

- 6.4.12 Hydrotechnik GmbH

- 6.4.13 Blacoh Fluid Control

- 6.4.14 Rotec Hydraulics Ltd.

- 6.4.15 Eaton Filtration LLC

- 6.4.16 Bosch Auto Accumulator Systems

- 6.4.17 Kawasaki Hydraulics

- 6.4.18 KYB Corporation

- 6.4.19 Danfoss Power Solutions

- 6.4.20 Hallite Seals International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment