PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061700

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061700

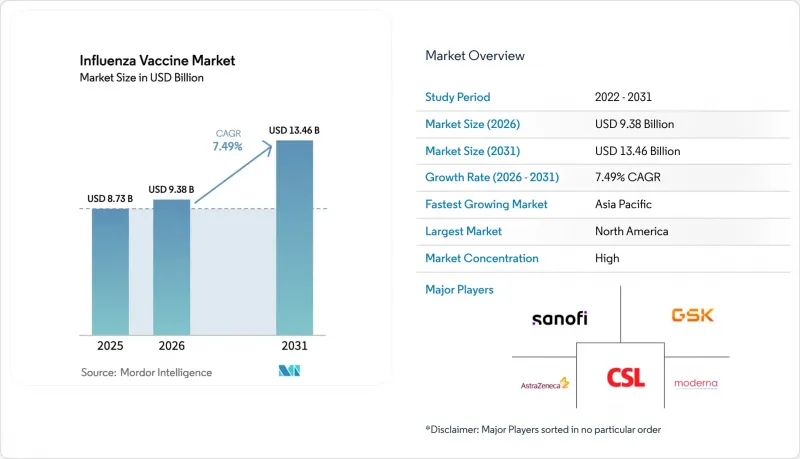

Influenza Vaccine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the influenza vaccine market size was valued at USD 8.73 billion in 2025 and is estimated to grow from USD 9.38 billion in 2026 to reach USD 13.46 billion by 2031, at a CAGR of 7.49% during the forecast period (2026-2031).

This report is Segmented by Vaccine Type (Quadrivalent, Trivalent, and More), Form (Inactivated, Live Attenuated, and More), Age Group (Pediatric, Adults), Route of Administration (Injection, Nasal Spray), Distribution Channel (Hospitals & Clinics, Pharmacies, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Influenza Vaccine Market Trends and Insights

Escalating Government-Funded Immunization Targets & Procurement

National procurement programs have moved beyond routine seasonal ordering toward strategic stockpiling for pandemic readiness in the influenza vaccine market. Washington's USD 176 million award to Moderna for an mRNA pandemic-influenza candidate underscores this shift, while London's purchase of more than 5 million H5N1 doses from CSL Seqirus signals a similar stance in the United Kingdom. Ottawa followed suit by securing 500,000 doses of GSK's Arepanrix H5N1, aligning North American preparedness strategies. Governments now frame influenza vaccines as security assets rather than basic public-health inputs. The World Health Organization's Global Action Plan expanded collective pandemic capacity to 1.3 billion doses a year by 2016, laying the groundwork for today's larger procurement ambitions.

Rapid Adoption of Cell- and Recombinant-Based Production Platforms

Manufacturers are diversifying beyond egg-based methods to improve supply security and vaccine performance across the influenza vaccine market. Data from CSL Seqirus show cell-based products outperformed egg-derived comparators across several age groups during the 2022-23 season [SEQIRUS.COM]. Moderna's new Australian plant, the Southern Hemisphere's only dedicated mRNA facility for respiratory vaccines, will be able to supply 100 million doses annually, broadening geographic reach for advanced platforms. The WHO's mRNA Technology Transfer Program further signals institutional support for non-traditional production. Even so, more than 80% of global output still originates from chicken eggs, underscoring the scale of change now under way.

High Clinical & Manufacturing Investment for Next-Gen Vaccines

Switching to advanced platforms demands capital-intensive trials and facility upgrades influenza vaccines market. Novavax's Phase 3 COVID-influ combo study alone carries a USD 500 million clinical bill for fiscal 2025. Converting egg-based plants to cell-based or mRNA systems can cost multiple billions, while CSL's USD 11.7 billion Vifor deal illustrates the scale of corporate outlays aimed at diversifying beyond legacy models. Complex regulatory pathways stretch timelines; mRNA flu candidates remain in Phase 3 despite the technology's COVID-19 success. Smaller firms often struggle to raise such sums, which may accelerate consolidation among cash-rich incumbents.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Geriatric High-Risk Population Base

- Heightened Pandemic-Preparedness Stockpiling Budgets

- Persistent Vaccine Hesitancy & Misinformation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Trivalent products captured 28.32% of sales in 2025 but now post the segment's quickest expansion at 7.81% CAGR after regulatory alignment removed B/Yamagata. Quadrivalents still dominate revenue yet face gradual erosion as payers question the necessity of an inactive lineage. Manufacturers accelerated validation runs to meet the 2024-25 season, demonstrating flexible bulk-antigen capacities that safeguard supply continuity. The influenza vaccines market size for trivalent doses is expected to widen as emerging economies prefer lower-cost three-strain presentations for public tenders. High-dose and adjuvanted trivalent versions aimed at seniors will further boost value. In contrast, quadrivalent offerings will pivot to combination formats, bundling respiratory syncytial virus or COVID-19 antigens to maintain premium positioning.

Volume swings affect raw-material procurement, notably embryonated eggs, potentially stabilizing prices as trivalent output requires fewer eggs. The transition also reduces fill-finish complexity, freeing line time for other biologics during off-peak months. While providers may face short-term confusion, clear CDC guidance has minimized substitution errors. Global health agencies anticipate improved strain match rates, lowering breakthrough infection risk and reinforcing trust in vaccination. As these benefits materialize, the influenza vaccines market will likely recalibrate pricing tiers to reflect simplified compositions and differential effectiveness evidence.

Inactivated vaccines represented 90.95% of 2025 sales yet also record a 7.71% CAGR as proprietary cell-based and recombinant versions enter tender lists. Their broad regulatory familiarity and cold-chain compatibility sustain hospital ordering preferences. Within this class, cell-derived antigens circumvent egg-adaptation mutations, lifting effectiveness and supporting premium bids. Recombinant HA constructs, such as Flublok, shorten lead times and reduce contamination risk, offering strategic value for pandemic pivoting.

Live attenuated solutions lag in adult uptake due to contraindications but gain new life via at-home nasal sprays. Meanwhile, pipeline mRNA candidates target licensure from 2026 onward. Early readouts show parity with licensed comparators on A-strains but weaker responses against B lineages, prompting formulation fine-tuning. If successful, mRNA could compress manufacturing to weeks, slash changeover costs, and enable bespoke regional compositions. Stakeholders therefore weigh capex now to avoid obsolescence later, a calculus that influences capital allocation across the influenza vaccines market.

Geography Analysis

North America held 47.10% of revenue in 2025 owing to universal CDC recommendations, insurance mandates, and corporate clinics. The U.S. couples large-scale purchasing with rapid distribution; Canada supplements domestic output with GSK contracts, securing 500,000 pandemic doses while aligning regulatory reviews through the Canada-U.S. Regulatory Cooperation Council. Mexico leverages USMCA to streamline cross-border antigen shipments, supporting joint North American preparedness.

Asia-Pacific is expanding at 7.92% CAGR. All 11 WHO South-East Asia Region countries now maintain National Influenza Centers, improving surveillance and strain selection. China's atypical late 2024 season revealed timing gaps that manufacturers addressed by staggering release lots, highlighting adaptive supply chains. Japan, after decades of subcutaneous preference, endorsed intramuscular administration, improving dose efficacy and standardizing global protocols. Australia's mRNA factory de-risks hemispheric supply and could export to Southeast Asia, making the region less reliant on Northern Hemisphere production.

Europe possesses mature coverage yet faces demographic stagnation. EMA centralized approvals facilitate cross-border trade, and the U.K. continues deep stockpiling despite Brexit through early tenders for 5 million H5N1 doses. Middle East and Africa trail but benefit from Gavi's manufacturing accelerator, which will underwrite capacity for both seasonal and pandemic needs. South America builds readiness via PAHO simulation drills that test deployment plans for respiratory pandemics. Collectively, these dynamics diversify demand, making the influenza vaccines market less dependent on any single geography.

- Sanofi

- GlaxoSmithKline

- CSL Seqirus

- AstraZeneca

- Pfizer

- Merck

- Moderna

- Novavax

- Bharat Biotech

- Sinovac Biotech

- Serum Institute of India

- Daiichi Sankyo Co. Ltd.

- Emergent Bio Solutions

- BIKEN

- Abbott Laboratories

- Viatris

- SK bioscience

- Green Cross Corp. (GC Flu)

- Valneva

- Mitsubishi Tanabe Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Government-funded Immunization Targets & Procurement

- 4.2.2 Rapid Adoption of Cell- and Recombinant-based Production Platforms

- 4.2.3 Expanding Geriatric High-risk Population Base

- 4.2.4 Heightened Pandemic-preparedness Stockpiling Budgets

- 4.2.5 Regulatory Shift Back to Trivalent Formulations Lowers Mismatch Risk

- 4.2.6 Approval of at-home Nasal Spray Vaccines Unlocks D2C Channel

- 4.3 Market Restraints

- 4.3.1 High Clinical & Manufacturing Investment for Next-gen Vaccines

- 4.3.2 Persistent Vaccine Hesitancy & Misinformation

- 4.3.3 Fragile Global Egg Supply Chain Vulnerable to Avian-flu Shocks

- 4.3.4 Capital Burden of Re-tooling to mRNA/cell Facilities

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value-USD)

- 5.1 By Vaccine Type

- 5.1.1 Quadrivalent

- 5.1.2 Trivalent

- 5.1.3 High-dose / Adjuvanted

- 5.2 By Form

- 5.2.1 Inactivated

- 5.2.2 Live Attenuated

- 5.2.3 mRNA / Recombinant

- 5.3 By Age Group

- 5.3.1 Pediatric

- 5.3.2 Adults

- 5.4 By Route of Administration

- 5.4.1 Injection

- 5.4.2 Nasal Spray

- 5.5 By Distribution Channel

- 5.5.1 Hospitals & Clinics

- 5.5.2 Pharmacies & Retail Chains

- 5.5.3 Government & NGO Procurement

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Sanofi SA

- 6.3.2 GlaxoSmithKline plc

- 6.3.3 CSL Seqirus

- 6.3.4 AstraZeneca plc

- 6.3.5 Pfizer Inc.

- 6.3.6 Merck & Co. Inc.

- 6.3.7 Moderna Inc.

- 6.3.8 Novavax Inc.

- 6.3.9 Bharat Biotech

- 6.3.10 Sinovac Biotech Ltd.

- 6.3.11 Serum Institute of India

- 6.3.12 Daiichi Sankyo Co. Ltd.

- 6.3.13 Emergent BioSolutions

- 6.3.14 BIKEN

- 6.3.15 Abbott Laboratories

- 6.3.16 Viatris Inc.

- 6.3.17 SK bioscience

- 6.3.18 Green Cross Corp. (GC Flu)

- 6.3.19 Valneva SE

- 6.3.20 Mitsubishi Tanabe Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment