PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061756

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061756

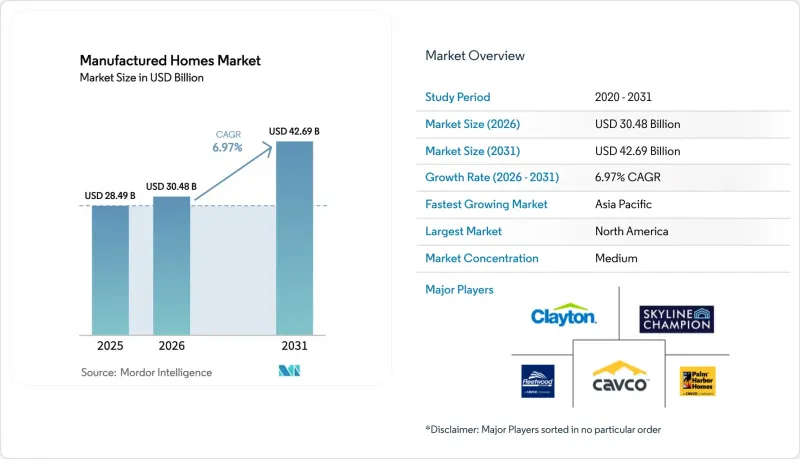

Manufactured Homes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the manufactured homes market size is projected to expand from USD 28.49 billion in 2025 and USD 30.48 billion in 2026 to USD 42.69 billion by 2031, registering a CAGR of 6.97% between 2026 to 2031.

This report is Segmented by Structure Type (Single-Section Homes, Multi-Section Homes, and Other Types), by Application (Single Family and Multi Family), by Material (Timber, Metal, Concrete, and Others), and by Geography (North America, South America, Europe, Middle East and Africa, and Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Global Manufactured Homes Market Trends and Insights

Worsening Housing Affordability Pushing Demand for Lower-Cost, Factory-Built Dwellings

Median site-built home prices topped USD 300,000 in 2024, while manufactured models averaged only USD 123,000 before land, preserving a 60% cost gap that continues to widen as labour and material inflation erode traditional affordability. The FHFA price index for manufactured homes rose 7.9% between Q2 2023 and Q2 2024, still below the 11.4% jump for site-built comparables, reinforcing the value proposition for households earning 80-120% of the area median income. In India, a 10-million-unit affordable-housing deficit is pushing state agencies and private developers toward modular builds that deliver units 40% faster, while Australia's 106,000-home shortage is fueling double-digit growth for factory-built options. Household budgets strained by rising mortgage rates and stagnant real-wage growth are therefore redirecting demand toward the manufactured homes market. With affordability challenges expected to persist through 2031, the driver provides a structural uplift rather than a cyclical spike.

Faster Delivery and Predictable Quality/Schedule Versus Site-Built Construction

Factory-controlled production eliminates weather delays and reduces skilled-labor requirements, enabling 30-50% shorter build cycles compared with site-built housing. Daiwa House, Sekisui House, and leading U.S. suppliers report 60% completion inside the factory, shrinking on-site assembly to mere weeks, which allows developers to meet tight lease-up schedules for build-to-rent portfolios. China's "Made in China 2025" program mandates 30% prefabrication for urban projects by 2026, with subsidies tied to modular adoption that trims construction time by nearly 40%. Predictable schedules also de-risk cost overruns; factory builds see only 5-10% budget variance versus the 20-30% typical of site projects, strengthening lender confidence. The time-saving advantage feeds directly into net present value calculations for institutional investors, making schedule certainty a meaningful catalyst for market growth.

Zoning/Exclusionary Ordinances and NIMBY Resistance Limiting Sites and Park Expansions

Texas had to legislate city-level zoning access via SB 785 because many municipalities still bar HUD-code homes, a reminder that land-use power remains highly localised in the United States. Even progressive California imposes setback, design review, and utility-connection rules that add USD 15,000-25,000 to placements, eroding the cost advantage of factory-built ADUs. In Europe, Ilke Homes collapsed in 2024 after protracted planning delays, illustrating that modular providers can be derailed even with ample equity. Community pushback also surfaces when private-equity owners lift lot rents, prompting U.S. lawmakers to study rent-control measures, which could dampen investor appetite. Until uniform zoning reform gains momentum, siting friction will cap the manufactured homes market's ability to recapture historical shipment peaks.

Other drivers and restraints analyzed in the detailed report include:

- Institutional Interest in Land-Lease Communities and Build-to-Rent (BTR) Creating Scalable Pipelines

- Policy Tailwinds Expanding Placement Options

- Financing Frictions-Chattel Loans with Higher Rates and Limited Mortgage Access

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-section homes captured 57.8% of the manufactured homes market share in 2025, propelled by family demand for 1,200-2,000 square-foot layouts priced near USD 125,000, a sharp discount to site-built equivalents. Manufacturers such as Skyline Champion and Clayton Homes optimised 48 and 40 facilities, respectively, for multi-section output, achieving learning-curve cost advantages and strengthening distributor networks that shorten order-to-delivery windows. Financing access is also more favourable: multi-section units on permanent foundations often qualify for MH Advantage or CHOICEHome, delivering conventional rates that expand the buyer pool. Meanwhile, single-section homes priced at USD 85,000 or less remain popular among retirees and entry-level households but face mortgage barriers that restrict volume potential.

Tiny homes, grouped under "other types," represent the fastest-growing niche with a 7.71% CAGR forecast to 2031 as remote work, minimalism, and sustainability reshape consumer preferences. Units between 200-400 square feet, often set on wheels, appeal to millennials seeking mobility and low carbon footprints. California's AB 2782 and Oregon's pioneering tiny-home definition give this category a clearer regulatory runway, while ADU-friendly municipalities encourage backyard placements at a cost of USD 30,000-100,000. Builders such as Tumbleweed and Escape Traveller leverage social-media marketing to tap lifestyle demand, but zoning ambiguity and insurance hurdles limit mass-market scale. Over the forecast period, multi-section dominance will persist, yet tiny homes will secure incremental share in urban infill and vacation-property subsegments.

Geography Analysis

North America generated 40.8% of 2025 revenue in the manufactured homes market, powered by the United States' 103,000 unit shipments in 2024, a 16% annual jump that nonetheless leaves ample headroom versus historical peaks. Fannie Mae's USD 70 billion duty-to-serve commitment through 2027 and private-equity inflows exceeding USD 10 billion have professionalised park operations and delivered broader financing options. Texas's SB 785 and California's ADU streamlining have improved zoning access, yet suburban NIMBYism and chattel-loan interest rates still hamper penetration into high-income enclaves. Canada's colder climate raises insulation requirements, adding USD 8,000-10,000 per unit, while Mexico's nascent mortgage infrastructure restricts throughput despite a growing urban housing deficit.

Asia-Pacific is the fastest-growing arena in the manufactured homes market, expected to advance at an 8.77% CAGR to 2031 on the back of China's 30% prefabrication mandate for urban projects and India's 10-million-unit affordable-housing shortfall under PM Awas Yojana. Japanese majors Sekisui House and Daiwa House have parlayed earthquake-resistant designs into a combined USD 52 billion in 2024 revenue, with Sekisui targeting net-zero energy for all Australian deliveries by 2030. Australia's 106,000-home shortage is prompting state governments to offer modular incentives, while Indonesia and Vietnam experiment with prefab models to meet surging urban demand. Financing ecosystems remain uneven, yet governmental subsidies and rapid urbanisation underpin long-run potential.

Europe holds a smaller yet strategically significant share in the manufactured homes market. The United Kingdom's goal of 300,000 new dwellings per year relies heavily on modular factories like Legal & General's 550-unit Leeds plant, though Ilke Homes' 2024 failure highlighted lingering planning bottlenecks. Germany, Scandinavia, and Austria, already accustomed to timber-frame culture, integrate factory-built systems into nearly 20% of new starts, spurred by the EU's zero-emission mandate for 2030. Eastern Europe remains fragmented, yet rising labour costs and EU recovery-fund allocations could accelerate adoption. Outside the tri-regional core, Saudi Arabia and the UAE apply modular methods for megaprojects but lack frameworks for mass-market housing, whereas South America and Africa stay nascent due to financing hurdles and political volatility.

- Clayton Homes

- Skyline Champion Corporation

- Cavco Industries Inc.

- Fleetwood Homes

- Palm Harbor Homes

- Commodore Homes

- Champion Home Builders

- Deer Valley Homebuilders

- Nobility Homes

- Kit Custom Homebuilders

- Sunshine Homes

- TruMH

- Sekisui House Ltd.

- Daiwa House Industry Co.

- Ilke Homes

- Legal & General Modular Homes

- Honkarakenne Oyj

- Willerby Ltd.

- Tingdene Homes Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Worsening housing affordability pushing demand for lower-cost, factory-built dwellings.

- 4.2.2 Faster delivery and predictable quality/schedule versus site-built construction.

- 4.2.3 Institutional interest in land-lease communities and BTR creating scalable pipelines.

- 4.2.4 Energy-efficient designs and green certifications lowering lifetime operating costs.

- 4.2.5 Policy tailwinds (zoning reform, ADUs, HUD-code updates) expanding placement options.

- 4.3 Market Restraints

- 4.3.1 Zoning/exclusionary ordinances and NIMBY resistance limiting sites and park expansions.

- 4.3.2 Financing frictions-chattel loans with higher rates and limited mortgage access.

- 4.3.3 Perception and appraisal gaps versus site-built homes affecting resale values and uptake.

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Pricing & Cost-Structure Analysis

- 4.8 Housing Shortage & Demographic Outlook

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value USD Billion)

- 5.1 By Structure Type

- 5.1.1 Single-Section Homes

- 5.1.2 Multi-Section Homes

- 5.1.3 Other Types

- 5.2 By Application

- 5.2.1 Single Family

- 5.2.2 Multi Family

- 5.3 By Material

- 5.3.1 Timber

- 5.3.2 Metal

- 5.3.3 Concrete

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Netherlands

- 5.4.3.7 Rest of Europe

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 South Africa

- 5.4.4.4 Nigeria

- 5.4.4.5 Rest of Middle East and Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 Indonesia

- 5.4.5.7 Rest of Asia-Pacific

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Clayton Homes

- 6.4.2 Skyline Champion Corporation

- 6.4.3 Cavco Industries Inc.

- 6.4.4 Fleetwood Homes

- 6.4.5 Palm Harbor Homes

- 6.4.6 Commodore Homes

- 6.4.7 Champion Home Builders

- 6.4.8 Deer Valley Homebuilders

- 6.4.9 Nobility Homes

- 6.4.10 Kit Custom Homebuilders

- 6.4.11 Sunshine Homes

- 6.4.12 TruMH

- 6.4.13 Sekisui House Ltd.

- 6.4.14 Daiwa House Industry Co.

- 6.4.15 Ilke Homes

- 6.4.16 Legal & General Modular Homes

- 6.4.17 Honkarakenne Oyj

- 6.4.18 Willerby Ltd.

- 6.4.19 Tingdene Homes Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment