PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061759

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061759

Smart Air Purifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

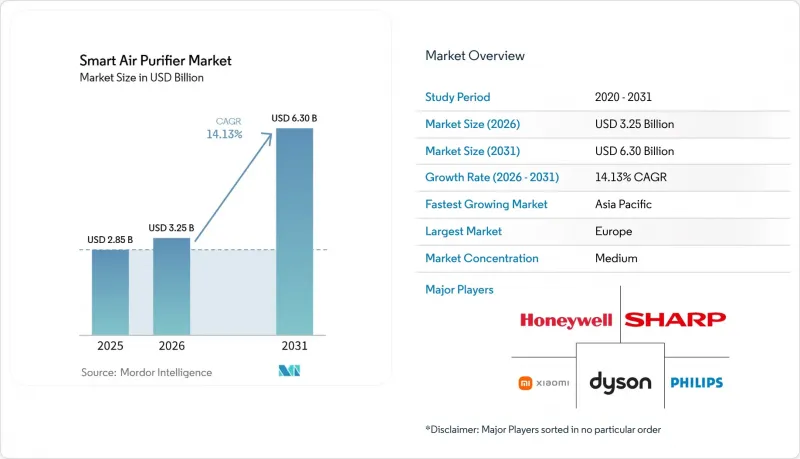

According to Mordor Intelligence, the smart air purifier market size is projected to be USD 2.85 billion in 2025, USD 3.25 billion in 2026, and reach USD 6.30 billion by 2031, growing at a CAGR of 14.13% from 2026 to 2031.

This report is Segmented by Product Type (Dust Collectors, Fume & Smoke Collectors, and Others), Technology (HEPA, Ionic Filter, and More), Installation Type (Stand-Alone / Portable and In-Duct / Central HVAC), Application (Residential, Commercial, and Industrial), Distribution Channel (B2C and B2B), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Air Purifier Market Trends and Insights

Rising Urban PM2.5 & VOC Awareness

Urban air quality deterioration has reached crisis levels in major metropolitan areas, and severe smog episodes in Ho Chi Minh City and Delhi, India, turned inland air pollution into front-page news in 2025. Real-time particulate sensors inside connected purifiers translate invisible hazards into easy-to-read dashboards, raising purchase urgency among city dwellers. Users also link pollutant spikes to specific cooking or cleaning activities, creating behaviour change that further underscores device value. Manufacturers now promote 0.3-micron detection and VOC correlation as proof points rather than optional add-ons. As a result, the smart air purifier market benefits from health-driven demand that is less price-sensitive than previous discretionary gadget cycles.

Integration With Smart-Home Ecosystems & Voice Assistants

Partnerships between HVAC controllers and air purifiers allow automated airflow boosts during peak outdoor pollution periods, improving comfort without user intervention. Voice assistants trigger "clean air" routines that raise fan speeds and switch on UV-C modules before occupants arrive home, embedding purifiers into daily habits. Cloud dashboards consolidate air-quality, occupancy, and energy data, giving building managers actionable insights. This interoperability makes standalone models less attractive, pushing brands toward open APIs and Matter-ready firmware. The dynamic lifts repeat sales because firmware upgrades and accessory sensors extend product relevance.

High Device & Filter-Replacement Costs

Annual HEPA cartridge spend of USD 50-150 per unit deters lower-income households even in cities with hazardous smog . Manufacturers respond with electrostatic or washable filters, but convincing buyers of comparable efficacy requires third-party validation and marketing outlays. In regions where disposable income lags pollution intensity, subsidies or pay-as-you-clean models could unlock latent demand. Until cost barriers ease, price elasticity will curb penetration, especially in multi-device scenarios such as large apartments or classrooms.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Indoor-Air-Quality Regulations in Key Economies

- Falling Sensor Costs Enabling Embedded IAQ Modules

- Consumer Scepticism Over Performance Claims

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dust collectors generated 44.35% of the market air purifier revenue in 2025, highlighting their broad appeal for PM2.5 and allergen capture in homes and small offices. Their dominance rests on mature HEPA media and competitive pricing that suits first-time buyers. Fume and smoke collectors, however, are climbing at a 14.92% CAGR as restaurants, commercial kitchens, and light-manufacturing sites target VOCs and grease vapors. Multi-stage designs now blend particulate, activated-carbon, and catalytic layers, reducing the need for separate units. This convergence signals that future models will unify dust and fume control to streamline maintenance. The "Others" niche-pathogen detection pods and biofiltration towers-remains small but influential by pushing sensor innovation that later filters into mainstream lines. Combined, these trends keep the smart air purifier market in a state of product-type evolution responsive to emerging pollutant profiles.

Second-generation dust collectors pair 0.3-micron sensors with smartphone alerts that prompt pre-emptive fan speed increases. Fume and smoke units integrate temperature-resistant housings and grease-collection trays to suit cooking environments. Early adopters validate ROI through lower odor complaints and regulatory compliance certificates, encouraging wider industry uptake. As PM2.5 and VOC standards tighten, the total addressable smart air purifier market size for mixed-use devices will broaden further, stimulating cross-category R&D investment.

In the smart air purifier market, HEPA systems captured 59.35% of 2025 revenue thanks to proven 99.97% removal efficiency and strong alignment with regulatory test methods. Manufacturers now encase HEPA filters within fully sealed housings to prevent bypass and market the upgrade as "true" or "medical-grade." Ionic filters, recording a 16.32% CAGR through 2031, address consumer desire for lower energy draw and filter-free operation. Their trajectory is strongest in markets where electricity tariffs are high. UV-C, activated-carbon, and plasma modules round out the technology mix, often combined in hybrid stacks to attack pathogens and odors.

Ionic solutions must manage ozone output below regional limits; firms advertise compliance certificates to reassure buyers. UV-C add-ons ride post-pandemic interest in germicidal capabilities, yet lamp-replacement cycles add cost. Start-ups explore photocatalytic oxidation and cold-plasma arrays that promise broad-spectrum pollutant breakdown with minimal consumables. This experimentation underscores a wider shift in the smart air purifier market toward modular platforms, letting users swap or layer technologies as pollutant profiles change.

Geography Analysis

Europe generated 31.75% of 2025 revenue as ecodesign directives and consumer eco-labels spurred early adoption of energy-efficient purifiers. The region's retailers position indoor-air quality alongside wellness categories, making upselling easier. Growth continues as commercial landlords invest in air-quality upgrades to meet green-lease clauses. Manufacturers with multilingual firmware and GDPR-compliant data policies gain trust and repeat sales.

Asia-Pacific is the fastest-growing region in the smart air purifier market, with a forecast 14.18% CAGR, underpinned by urbanization and high ambient smog. China's national indoor-air monitoring expansion widens public awareness, while Indian consumers view clean-air devices as status symbols. Rising disposable income supports premium purchases, and local brands compete on localized UI and after-sales networks. Government subsidies for IoT air-quality nodes in South Korea and Japan further boost uptake.

North America shows steady, regulation-driven demand in the smart air purifier market. The tightened PM2.5 limit accelerates the replacement of legacy units unable to meet new benchmarks. Smart-home penetration also favors connected purifiers that sync with existing hubs.

The Middle East and Africa present nascent yet promising opportunities in the smart air purifier market. Dubai's USD 500 million Air Quality Strategy positions clean-air appliances as part of national climate-tech portfolios. Saudi Arabia's monitoring push across 7,000 plants indicates future compliance-led demand. South America remains early stage, but worsening urban smog in Sao Paulo and Bogota hints at long-term potential once income levels rise. Overall, regulatory progress and economic development together shape the smart air purifier market's geographic rollout path.

- Dyson Ltd.

- Sharp Corporation

- Xiaomi Corporation

- Honeywell International Inc.

- Koninklijke Philips N.V.

- LG Electronics Inc.

- Coway Co., Ltd.

- Levoit (Vesync Co., Ltd.)

- Winix Inc.

- Havells India Ltd.

- Unilever PLC (Blueair AB)

- Smart Air Filters Pvt Ltd.

- Daikin Industries Ltd.

- Samsung Electronics Co., Ltd.

- IQAir AG

- Panasonic Corporation

- Molekule Inc.

- Rabbit Air

- Airversa

- GermGuardian (Guardian Technologies)

- SharkNinja

- Alen Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Urban PM2.5 & VOC Awareness

- 4.2.2 Integration With Smart-Home Ecosystems & Voice Assistants

- 4.2.3 Stricter Indoor-Air-Quality Regulations in Key Economies

- 4.2.4 Post-Pandemic Consumer Spend on Residential Wellness

- 4.2.5 Falling Sensor Costs Enabling Embedded IAQ Modules

- 4.2.6 Insurance Premium Discounts Tied to IAQ Data

- 4.3 Market Restraints

- 4.3.1 High Device & Filter-Replacement Costs

- 4.3.2 Consumer Skepticism Over Performance Claims

- 4.3.3 Data-Privacy & Cyber-Security Risks in Connected Units

- 4.3.4 Regulatory Crack-Downs on Ozone-Emitting Devices

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Dust Collectors

- 5.1.2 Fume & Smoke Collectors

- 5.1.3 Others

- 5.2 By Technology

- 5.2.1 HEPA

- 5.2.2 Activated Carbon Filtration

- 5.2.3 Ionic Filter

- 5.2.4 Ultra-Violet Technology

- 5.2.5 Others

- 5.3 By Installation Type

- 5.3.1 Stand-alone / Portable

- 5.3.2 In-duct / Central HVAC

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Multi-brand Stores

- 5.5.1.2 Exclusive Brand Outlets

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B/Directly from the Manufacturers

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East And Africa

- 5.6.5.1 United Arab of Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Dyson Ltd.

- 6.4.2 Sharp Corporation

- 6.4.3 Xiaomi Corporation

- 6.4.4 Honeywell International Inc.

- 6.4.5 Koninklijke Philips N.V.

- 6.4.6 LG Electronics Inc.

- 6.4.7 Coway Co., Ltd.

- 6.4.8 Levoit (Vesync Co., Ltd.)

- 6.4.9 Winix Inc.

- 6.4.10 Havells India Ltd.

- 6.4.11 Unilever PLC (Blueair AB)

- 6.4.12 Smart Air Filters Pvt Ltd.

- 6.4.13 Daikin Industries Ltd.

- 6.4.14 Samsung Electronics Co., Ltd.

- 6.4.15 IQAir AG

- 6.4.16 Panasonic Corporation

- 6.4.17 Molekule Inc.

- 6.4.18 Rabbit Air

- 6.4.19 Airversa

- 6.4.20 GermGuardian (Guardian Technologies)

- 6.4.21 SharkNinja

- 6.4.22 Alen Corporation

7 Market Opportunities & Future Outlook

- 7.1 Integration with Smart Home Ecosystems & Data Monetization