PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061820

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061820

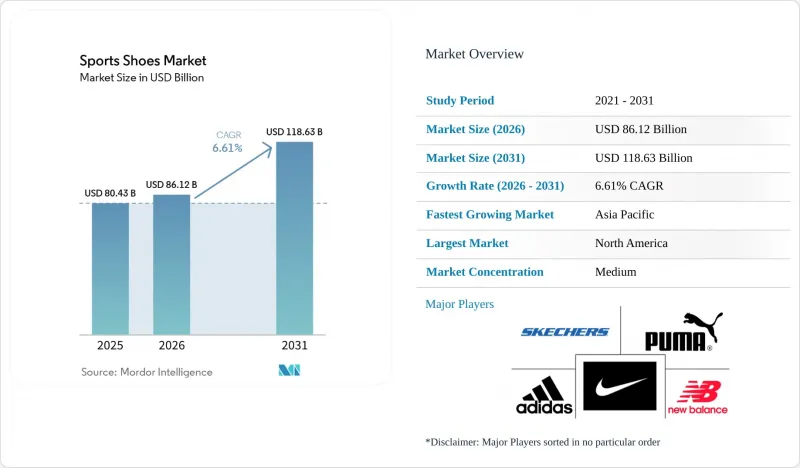

Sports Shoes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sports shoes market size was valued at USD 80.43 billion in 2025 and is estimated to grow from USD 86.12 billion in 2026 to reach USD 118.63 billion by 2031, at a CAGR of 6.61% during the forecast period (2026-2031).

This report is Segmented by Sport Type (Baseball, Basketball, Soccer/Football, Tennis, and Other Sports), End User (Men, Women, and Kids), Price Range (Mass and Premium), Distribution Channel (Sports and Athletic Goods Stores, Supermarkets/Hypermarkets, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Sports Shoes Market Trends and Insights

Rising Health and Fitness Awareness

Post-pandemic, running has solidified its status as a primary fitness activity. This shift has led to a surge in gym memberships among women, spurring innovations in female-specific footwear that seamlessly marry technical performance with style. With governments and health organizations championing active lifestyles, there's a consistent demand for both entry-level and high-performance running shoes. This trend is especially evident in the Asia-Pacific region. Here, urbanization and increasing disposable incomes are broadening the market. ASICS, for instance, anticipates a 35% annual growth in India and is setting its sights on dominating running-shoe sales by 2029, eyeing a market projected to hit USD 4.8 billion by 2033. In response, brands are unveiling models tailored to the region, striking a balance between affordability and advanced features. This ensures that health-conscious consumers, regardless of their income bracket, can access high-performance footwear. Such democratization of technology is not only shortening product cycles but also heightening competition in the mass-market arena.

E-commerce and DTC Channel Expansion

Major brands are increasingly turning to direct-to-consumer (DTC) strategies as their main growth engine. In 2025, Adidas highlighted a 14-16% growth in its DTC segment and is now emphasizing omnichannel integration to boost its profit margins. Projections indicate that online retail stores will grow at a 7.81% CAGR through 2031, surpassing traditional retail channels. This growth is driven by brands pouring investments into their own e-commerce platforms, offering perks like exclusive colorways, early product releases, and subscription services. The economic rationale behind this shift is clear: DTC channels sidestep wholesale markdowns, grant access to direct consumer data, and allow for flexible pricing. Yet, the journey isn't smooth for everyone. In 2025, Nike grappled with DTC hurdles while adjusting its wholesale partnerships, underscoring that strong brand equity doesn't always smooth out distribution challenges. Meanwhile, smaller brands and regional players are seizing the moment. They're collaborating with third-party platforms and harnessing social commerce to connect with consumers under 35. This demographic, which constitutes two-thirds of the adult running shoe market growth, heavily relies on social media for brand discovery.

Counterfeit and Grey-Market Proliferation

Counterfeit sports shoes not only undermine brand equity but also diminish pricing power. Seizures, such as the Philippines' USD 2.69 million haul in 2025, represent just a fraction of the broader illicit trade, as highlighted by the Philippines Counterfeit. Grey-market channels further complicate brand positioning by selling authentic, yet diverted, inventory below authorized prices, thereby eroding margins. This challenge is especially pronounced in the Asia-Pacific region, where fragmented distribution networks and e-commerce marketplaces often shield unauthorized sellers. In response, brands are adopting measures like blockchain-based authentication, serialized product codes, and collaborations with platforms such as StockX, which verify authenticity prior to resale. Despite these efforts, enforcement remains sporadic. With premium shoes retailing between USD 250-500, the economic allure for counterfeiters is undeniable, underscoring the need for coordinated regulatory action to combat the issue effectively.

Other drivers and restraints analyzed in the detailed report include:

- Athleisure Blurring Performance and Lifestyle

- Carbon-Plated Super-Shoes Reach Mass Runners

- Raw-Material Cost Volatility (EVA, Rubber)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, soccer/football footwear commanded a 35.59% market share, with Firm Ground cleats leading the segment at 38%. These cleats reaped rewards from global participation rates and sponsorships in professional leagues. Meanwhile, basketball shoes are set to outpace the competition, projected to grow at a 7.08% CAGR through 2031. This surge is fueled by a blend of performance and lifestyle, allowing signature athlete lines, most notably Nike's Kobe series, which accounted for 37% of signature shoe sales in 2025, to evolve from mere court essentials to coveted streetwear. The segment's growth is bolstered by brands' strategic investments in athlete endorsements, cutting-edge technology platforms like Nike's Zoom Air and Adidas' Boost, and timely colorway releases that spark social media conversations and spur impulse buys.

Tennis footwear carves out a steady niche, with advancements in lateral stability and durability resonating with both recreational and competitive players. Baseball cleats, on the other hand, cater to a focused North American audience, offering metal and molded studs tailored for varying playing surfaces. The "Other Sports Type" category, which includes training, walking, and cross-training shoes, is riding the wave of the athleisure trend. Consumers are increasingly drawn to versatile footwear that seamlessly transitions between activities. Furthermore, the carbon-plated technology, which has already made waves in running, is now being explored in basketball and training. Brands are experimenting with plate geometries aimed at boosting vertical leaps and lateral agility, hinting at a potential new performance benchmark that could command premium pricing across all sports.

In 2025, men's sports shoes dominate the market with a commanding 61.69% share. This stronghold is buoyed by rising average selling prices and a trend of frequent replacements, driven by both athletic pursuits and lifestyle choices. The kids' segment is on a robust trajectory, growing at a 6.97% CAGR. This growth is fueled by parents' dedication to youth sports and a heightened awareness of the significance of quality footwear in child development and injury prevention. Meanwhile, women's sports shoes are emerging as a lucrative frontier. Brands are now tailoring gender-specific technologies and designs to cater to distinct biomechanical needs and aesthetic preferences.

The rapid expansion of the kids' segment is further amplified by the surge in organized youth sports. Parents are increasingly willing to invest in premium sports shoes for their aspiring young athletes. This trend is underscored by New Balance's strategic long-term partnership with the WNBA, highlighting brands' intensified focus on women's sports. Their aim is clear: to capitalize on the rising female participation and viewership. Moreover, the fusion of performance and fashion in women's sports shoes has given rise to new product categories. These cater to both athletic pursuits and lifestyle choices, significantly expanding market opportunities.

Geography Analysis

In 2025, North America commands a dominant 40.40% market share, buoyed by its rich sports culture, affluent consumers, and a penchant for premium sports shoes. The region's established market sees frequent product updates, unwavering brand loyalty, and a retail landscape that adeptly melds traditional and online shopping. Yet, as saturation tightens its grip and economic uncertainties make consumers more price-sensitive, growth has begun to decelerate. In response, brands are honing in on premiumization, innovative footwear technologies, and eco-friendly materials to maintain their edge and pricing authority.

Asia-Pacific is on the fast track, eyeing a robust CAGR of 7.82% up to 2031. This surge is powered by rising incomes, a burgeoning middle class, and an uptick in sports participation, especially in China and India. Bolstered by government initiatives championing sports and infrastructure, the region is laying a solid groundwork for sustained demand. With health consciousness on the rise and digital platforms like social media amplifying the message, the Asia-Pacific region is cementing its status as a pivotal growth hub in the global sports shoes arena.

Europe, while mature, enjoys steady growth, owing to its ingrained sports culture, a heightened focus on sustainability, and a penchant for premium brands. Initiatives like UEFA's Women's Football Development Program are not only broadening participation but also birthing new consumer segments. With a keen eye on sustainability, Europe is pushing boundaries in eco-friendly materials and circular economy practices. Companies like ASICS are at the forefront, unveiling fully recyclable footwear to align with shifting consumer desires and regulatory standards. Meanwhile, South America and the Middle East and Africa, with their burgeoning middle classes, urbanization trends, and a rising sports enthusiasm, are emerging as promising markets. As these regions bolster their retail frameworks and adopt localized brand strategies, they're poised for significant growth in the global sports shoes landscape.

- Nike Inc.

- Adidas AG

- Puma SE

- New Balance Athletics Inc.

- Skechers USA Inc.

- Under Armour Inc.

- ASICS Corporation

- Anta Sports Products Ltd.

- Li-Ning Company Ltd.

- Columbia Sportswear Co.

- Fila Holdings Corp.

- Mizuno Corp.

- VF Corporation

- Decathlon Group

- Xtep International Holdi.

- Amer Sports(Solomon)

- Wolverine World Wide (Merrell, Saucony)

- 361 Degrees International Limited

- On Holding AG (On Running)

- Lotto Sport Italia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising health and fitness awareness

- 4.2.2 E-commerce and DTC channel expansion

- 4.2.3 Athleisure blurring performance and lifestyle

- 4.2.4 Carbon-plated "super-shoes" reach mass runners

- 4.2.5 AI-driven virtual-fit tools are lifting online conversions

- 4.2.6 City-level run clubs triggering premium drop cycles

- 4.3 Market Restraints

- 4.3.1 Counterfeit and grey-market proliferation

- 4.3.2 Raw-material cost volatility (EVA, rubber)

- 4.3.3 Micro-plastic midsole scrutiny and regulation risk

- 4.3.4 The booming resale segment is cannibalizing new-shoe sales

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Sport Type

- 5.1.1 Baseball

- 5.1.2 Basketball

- 5.1.3 Soccer/Football

- 5.1.4 Tennis

- 5.1.5 Other Sports Type

- 5.2 End User

- 5.2.1 Men

- 5.2.2 Women

- 5.2.3 Kids

- 5.3 Price Range

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 Distribution Channels

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Sports and Athletic Good Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution channels

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Sweden

- 5.5.2.7 Belgium

- 5.5.2.8 Poland

- 5.5.2.9 Netherlands

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Thailand

- 5.5.3.5 Singapore

- 5.5.3.6 Indonesia

- 5.5.3.7 South Korea

- 5.5.3.8 Australia

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Peru

- 5.5.4.5 Chile

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Nike Inc.

- 6.4.2 Adidas AG

- 6.4.3 Puma SE

- 6.4.4 New Balance Athletics Inc.

- 6.4.5 Skechers USA Inc.

- 6.4.6 Under Armour Inc.

- 6.4.7 ASICS Corporation

- 6.4.8 Anta Sports Products Ltd.

- 6.4.9 Li-Ning Company Ltd.

- 6.4.10 Columbia Sportswear Co.

- 6.4.11 Fila Holdings Corp.

- 6.4.12 Mizuno Corp.

- 6.4.13 VF Corporation

- 6.4.14 Decathlon Group

- 6.4.15 Xtep International Holdi.

- 6.4.16 Amer Sports(Solomon)

- 6.4.17 Wolverine World Wide (Merrell, Saucony)

- 6.4.18 361 Degrees International Limited

- 6.4.19 On Holding AG (On Running)

- 6.4.20 Lotto Sport Italia

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK