PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062314

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062314

Tennis Shoes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

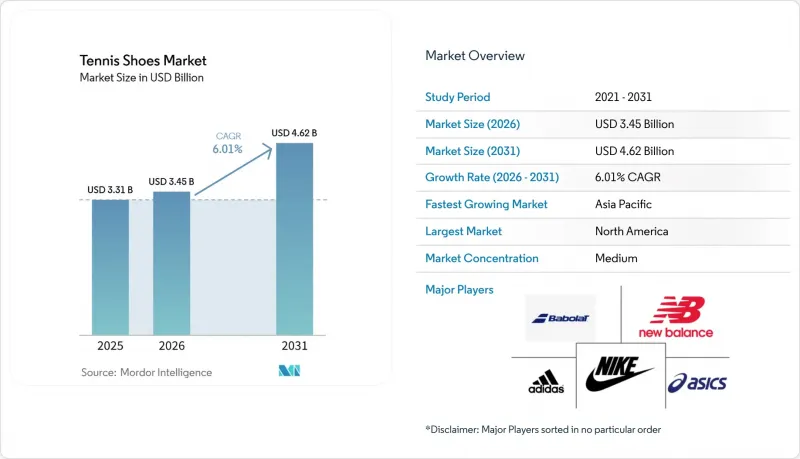

According to Mordor Intelligence, the global tennis shoes market size is expected to grow from USD 3.31 billion in 2025 to USD 3.45 billion in 2026 and is forecast to reach USD 4.62 billion by 2031 at a 6.01% CAGR over 2026-2031.

This report is Segmented by Product Type (Hard Court, Clay Court, Grass Court), End-User (Men, Women, Kids), Category (Mass, Premium), Distribution Channel (Offline Retail Stores, Online Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Tennis Shoes Market Trends and Insights

Growing participation in tennis and racquet sports

The surge in tennis participation globally is a significant driver for the tennis shoes market. In the United States, participation increased by 54% between 2019 and 2025, reaching 27.3 million players, fueling sustained demand for specialized footwear across recreational and competitive segments, according to the U.S. Tennis Association. Asia contributed 35.3 million players during this period, driven by government investments in public courts and school programs in countries like China and India. In North America, growth was influenced by post-pandemic lifestyle changes, with a shift toward outdoor and socially distanced activities that persisted into 2025. In the United States, women's participation rose by 10%, while youth enrollment in tennis programs expanded as parents prioritized skill development and college scholarship opportunities. Furthermore, the diversification of the player base, particularly among Hispanic and Asian-American communities, has prompted brands to tailor their marketing strategies and product sizing to meet the needs of these previously underserved groups, further boosting the demand for tennis shoes.

Technological advancements in footwear design

Technological advancements in footwear design are driving the growth of the global tennis shoes market, as manufacturers focus on innovations to improve performance, comfort, and durability. Modern tennis shoes feature advanced cushioning systems, responsive midsoles, and shock-absorbing materials to minimize impact stress during rapid lateral movements and intense play. The use of lightweight yet durable materials, such as engineered mesh and synthetic composites, enhances breathability while ensuring structural support. Furthermore, advancements in outsole design, including optimized tread patterns and high-abrasion rubber compounds, deliver improved traction on various court surfaces, enhancing player agility and confidence. Brands are increasingly utilizing data-driven design and biomechanical research to create shoes tailored to specific playing styles, further raising performance standards. These ongoing innovations attract not only professional athletes but also recreational players seeking high-performance footwear, contributing to market growth.

Counterfeit and low-quality products

The prevalence of counterfeit and low-quality products serves as a significant restraint on the global tennis shoes market by undermining brand integrity and diminishing consumer trust. These imitation products, often sold at considerably lower prices through unauthorized online and offline channels, appeal to price-sensitive consumers but fail to meet the performance, durability, and safety standards of authentic footwear. This negatively affects the revenue and reputation of established brands such as Nike and Adidas, while also leading to poor user experiences that may deter repeat purchases within the category. Furthermore, counterfeit goods hinder fair competition by diluting brand differentiation and reducing incentives for innovation, as companies face difficulties in protecting intellectual property and maintaining premium market positioning. The widespread availability of these products, particularly on e-commerce platforms with limited regulatory oversight, remains a significant obstacle to sustainable growth in the tennis shoes market.

Other drivers and restraints analyzed in the detailed report include:

- Rising influence of professional athletes and sponsorships

- Expansion of athleisure and sportswear culture

- Intense competition from multi-sport footwear

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard court tennis shoes accounted for 49.37% of the market share in 2025. The demand for these shoes in the global tennis shoes market is primarily driven by the widespread use of hard courts, which are the most common playing surface across professional tournaments, clubs, and recreational facilities worldwide. Hard courts, known for their abrasive nature, require footwear with superior durability, reinforced outsoles, and advanced cushioning systems to endure intense wear and reduce the impact on players' joints during fast-paced rallies. As a result, manufacturers such as Nike, Adidas, and ASICS have heavily invested in technologies that enhance shock absorption, lateral stability, and outsole resilience. These features make hard court tennis shoes highly appealing to both professional and amateur players. Furthermore, the global popularity of major tournaments played on hard courts strengthens consumer preference for this segment, as players often choose footwear suited to the most frequently used playing conditions.

Grass court tennis shoes, though a niche segment, are projected to grow at a CAGR of 6.59% through 2031. The growth of this segment is driven by the demand for specialized footwear designed to provide optimal traction and stability on slippery, low-friction natural grass surfaces. Unlike hard courts, grass courts require outsoles with nubbed or pimpled patterns to prevent slipping while allowing smooth movement, making surface-specific design a key factor influencing demand. Although grass courts are less prevalent globally, their association with prestigious tournaments and traditional tennis culture sustains consistent demand for this segment. Brands such as Nike and Adidas address this niche by offering performance-oriented designs that combine lightweight construction with enhanced grip and flexibility. Additionally, the influence of professional players competing on grass surfaces motivates enthusiasts to invest in dedicated footwear, supporting steady growth despite the segment's relatively limited geographic presence.

Men accounted for 52.41% of end-user demand in 2025, driven by high participation rates in both professional and recreational tennis. This demand is further influenced by major tournaments and athlete endorsements, which significantly shape purchasing behavior. Male players often prioritize performance-oriented features such as durability, stability, and impact protection, particularly for high-intensity and competitive play. As a result, brands continue to innovate with advanced cushioning systems and reinforced designs. Additionally, the widespread presence of men's leagues, clubs, and training programs across regions sustains consistent demand. The influence of sports culture and fitness-focused lifestyles further encourages investment in specialized tennis footwear among male consumers.

The women's tennis shoe segment is expanding at a 6.22% CAGR through 2031, driven by increasing female participation in sports, empowerment initiatives, and the rising visibility of women's tennis at global events. As more women engage in both competitive and recreational tennis, there is a growing demand for footwear that combines performance with comfort, fit, and aesthetic appeal. Leading brands such as Nike and Adidas are addressing this demand by developing gender-specific designs that consider anatomical differences, offering improved support, flexibility, and style variations. Furthermore, the expanding influence of female athletes, social media trends, and the popularity of athleisure fashion are encouraging women to adopt tennis shoes not only for sports but also for casual wear. This trend is broadening the consumer base and driving segment growth.

Geography Analysis

North America accounted for 34.53% of the market share in 2025, driven by a well-established sports culture, high participation in tennis at both professional and recreational levels, and robust consumer spending on premium athletic footwear. The presence of major tournaments, extensive club networks, and school-level sports programs sustains consistent demand for specialized tennis shoes. Additionally, consumers in the region exhibit a strong preference for technologically advanced and performance-oriented products, prompting brands such as Nike and Under Armour to focus on continuous innovation. The widespread adoption of athleisure and fitness-focused lifestyles, along with the dominance of organized retail and e-commerce channels, further supports market growth in the region.

Asia-Pacific is the fastest-growing region, with a CAGR of 6.27% through 2031, driven by increasing sports participation, rising urbanization, and growing awareness of fitness and active lifestyles among a large and diverse population. Emerging economies such as China and India are experiencing an expanding middle class and improved access to sports infrastructure, encouraging greater adoption of tennis and related equipment. International tournaments, government initiatives promoting sports, and the influence of global brands like Adidas and ASICS are enhancing market visibility and demand. Additionally, the rapid growth of digital commerce platforms and increasing brand penetration into tier-2 and tier-3 cities are improving product accessibility, accelerating regional market expansion.

The tennis shoes market in Europe, South America, and the Middle East and Africa is influenced by a combination of established sports traditions, emerging consumer markets, and growing interest in fitness and recreational activities. Europe benefits from a strong tennis heritage, widespread participation, and a high concentration of professional events, which support steady demand for premium and performance footwear. In South America and the Middle East and Africa, rising urbanization, improving sports infrastructure, and increasing exposure to international sports are driving participation and product adoption. Brands such as Nike, Adidas, and Puma are expanding their presence through retail partnerships and digital platforms to capitalize on these growing markets. Furthermore, the influence of global sports culture and the increasing preference for casual sportswear in daily life are contributing to demand across these regions.

- Nike Inc.

- Adidas AG

- ASICS Corporation

- New Balance Athletics Inc.

- Wilson Sporting Goods

- Babolat VS SAS

- Yonex Co. Ltd.

- Head Sport GmbH

- K-Swiss Inc.

- Prince Global Sports LLC

- Lotto Sport Italia

- Mizuno Corporation

- Diadora S.p.A.

- Li-Ning Company Ltd.

- Under Armour Inc.

- FILA Holdings Corp.

- Skechers USA Inc.

- Salming Sports

- Tecnifibre SAS

- Dunlop International Europe Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing participation in tennis and racquet sports

- 4.2.2 Technological advancements in footwear design

- 4.2.3 Rising influence of professional athletes and sponsorships

- 4.2.4 Growth of women's and youth participation in sports

- 4.2.5 Expansion of athleisure and sportswear culture

- 4.2.6 Product customization and personalization trends

- 4.3 Market Restraints

- 4.3.1 Counterfeit and low-quality products

- 4.3.2 Intense competition from multi-sport footwear

- 4.3.3 Performance limitations across court types

- 4.3.4 Regulatory and compliance challenges

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Hard Court

- 5.1.2 Clay Court

- 5.1.3 Grass Court

- 5.2 By End User

- 5.2.1 Men

- 5.2.2 Women

- 5.2.3 Kids

- 5.3 By Category

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail Stores

- 5.4.2 Online Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Netherlands

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Indonesia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Share, Products, Recent Developments)

- 6.4.1 Nike Inc.

- 6.4.2 Adidas AG

- 6.4.3 ASICS Corporation

- 6.4.4 New Balance Athletics Inc.

- 6.4.5 Wilson Sporting Goods

- 6.4.6 Babolat VS SAS

- 6.4.7 Yonex Co. Ltd.

- 6.4.8 Head Sport GmbH

- 6.4.9 K-Swiss Inc.

- 6.4.10 Prince Global Sports LLC

- 6.4.11 Lotto Sport Italia

- 6.4.12 Mizuno Corporation

- 6.4.13 Diadora S.p.A.

- 6.4.14 Li-Ning Company Ltd.

- 6.4.15 Under Armour Inc.

- 6.4.16 FILA Holdings Corp.

- 6.4.17 Skechers USA Inc.

- 6.4.18 Salming Sports

- 6.4.19 Tecnifibre SAS

- 6.4.20 Dunlop International Europe Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK