PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061821

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061821

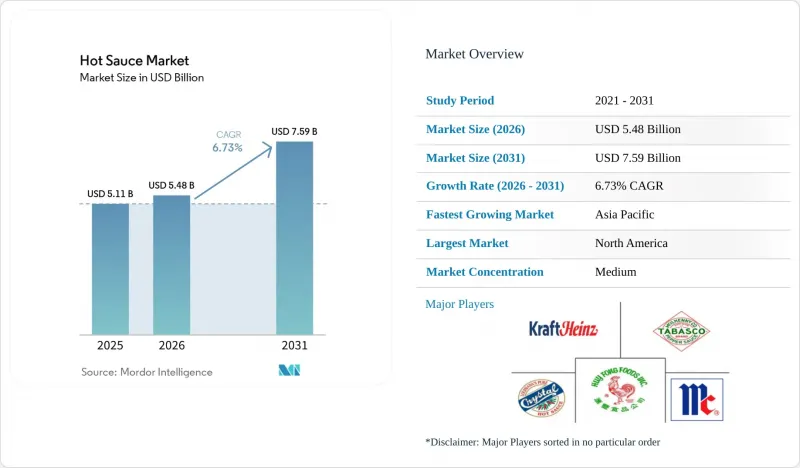

Hot Sauce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hot sauce market size is expected to grow from USD 5.11 billion in 2025 to USD 5.48 billion in 2026 and is forecast to reach USD 7.59 billion by 2031 at a 6.73% CAGR over 2026-2031.

This report is Segmented by Product Type (Red Hot Sauce, Green Hot Sauce, Yellow Hot Sauce, and Others), Flavor (Plain, and Flavored), Packaging (Bottles, Sachets and Pouches, and Others), Distribution Channel (HoReCa/Foodservice, and Retail), and (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Hot Sauce Market Trends and Insights

Growth of foodservice and quick-service restaurants

Quick-service restaurants (QSRs) are now embedding proprietary hot sauces into their core menu items, elevating these condiments from mere optional add-ons to pivotal brand-defining elements. Yum! Brands revealed that sauces evoke 2.4 times more consumer excitement than other menu components. Notably, 71% of KFC's top-performing items now feature these signature sauces in 2025. This integration goes beyond mere flavor differentiation. QSRs are harnessing the power of sauces not only to entice repeat visits but also to command premium pricing. Moreover, limited-time sauce offerings instill a sense of urgency, amplifying transaction frequency. The rise of ghost kitchens and delivery-only concepts further underscores this trend. Sauces, unlike fried items, travel better and retain their flavor integrity during transit. Additionally, the foodservice industry's pivot towards single-serve sachets, witnessing a robust 7.20% CAGR, underscores a quest for operational efficiency. These sachets allow for precise portion control, significantly reducing waste compared to traditional bulk dispensers.

Product innovation and premiumization

Artisan producers are leveraging fermentation, small-batch aging, and single-origin chili sourcing to command price premiums 3 to 5 times higher than their mass-market counterparts. Truff, which secured around USD 79.87 million in funding, rolled out its inaugural mild hot sauce in 2026, catering to consumers who value truffle-infused nuances over mere heat. Frank's RedHot unveiled 10 new SKUs, such as Korean BBQ, Pineapple Hawaiian, and Ghost Pepper Ranch, between April 2025 and January 2026. This move underscores the necessity for even established brands to innovate at an artisan pace to maintain their shelf presence. The "swicy" trend, which melds sweet and spicy flavors, has now transitioned to "swangy," adding tangy notes. This evolution reflects consumers' desires for intricate flavor profiles that complement a variety of cuisines. Moreover, limited-edition releases and partnerships with celebrities are fueling this premiumization trend. Such products frequently sell out within hours, leading to secondary markets and bolstering brand value through their scarcity.

Health concerns over sodium, sugar, and capsaicin

Manufacturers are under pressure to reformulate products, balancing the need to reduce sodium and sugar content with the desire to maintain flavor intensity. Starting in 2026, the FDA's revised definition of "healthy" will enforce stricter sodium limits, pushing brands to cut sodium levels by 10-15% or risk losing the "healthy" label. Peer-reviewed research highlights the dual nature of capsaicin: while it provides cardiovascular and metabolic benefits in moderation, excessive consumption can lead to gastrointestinal issues and worsen conditions like irritable bowel syndrome. This nuanced perception complicates marketing strategies and restricts consumption among health-conscious consumers. Flavored variants, especially those riding the "swicy" trend, are facing criticism over their sugar content. Clean-label proponents advocate for natural sweeteners, but these come at a premium, often 2 to 3 times the cost of traditional options, and can change the product's taste profile.

Other drivers and restraints analyzed in the detailed report include:

- Artificial intelligence-driven flavor personalization

- Growing popularity of home cooking

- Concern over raw material quality

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Red hot sauce maintains its commanding position with 53.59% market share in 2025, reflecting consumer familiarity and established brand loyalty, while green hot sauce emerges as the fastest-growing segment with 7.48% CAGR through 2031. Green hot sauce's acceleration is driven by its milder heat profile and broader culinary applications, particularly in fusion cuisines and health-conscious consumer segments seeking flavorful alternatives to traditional condiments. The competitive dynamics within product types reveal distinct positioning strategies, with red hot sauce manufacturers focusing on heat intensity differentiation and brand heritage, while green hot sauce producers emphasize flavor innovation and culinary versatility. McCormick's expansion of its crushed pepper portfolio with Thai Style Chili and Hatch Chile variants demonstrates the innovation trajectory within traditional red pepper products in May 2025.

Yellow hot sauce and other variants collectively represent the remaining market share, with yellow varieties gaining traction in specific regional markets and specialty applications. Yellow hot sauces, such as Yellowbird Habanero, often use habanero peppers as their main source of heat. These peppers provide a tropical, fruity heat that distinguishes yellow sauces from red or green varieties. The "other" category, including specialty blends and limited-edition variants, represents an emerging battleground for premium positioning and seasonal marketing campaigns that can command higher margins while testing consumer acceptance of new flavor profiles.

In 2025, plain hot sauce captured a dominant 65.69% market share, underscoring a deep-rooted consumer affinity for its pure chili essence, which allows for personal customization. Yet, flavored variants are set to surge at a 7.97% CAGR through 2031, driven by limited-edition launches, celebrity partnerships, and the rising "swicy" trend, which harmoniously melds sweet, spicy, and tangy flavors. Truff debuted its inaugural mild hot sauce in 2026, infusing truffle essence into a chili foundation, catering to upscale consumers who value flavor complexity over mere heat. The "swangy" trend, which introduces tangy nuances to sweet-spicy blends, took shape between 2025 and 2026. Brands began infusing citrus, vinegar, and fermented elements, crafting richer, multi-layered taste experiences.

Frank's RedHot rolled out 10 new SKUs, spanning from Korean BBQ to Ghost Pepper Ranch, between April 2025 and January 2026. This move underscores the rapid pace needed to thrive in the flavored segment, where novelty is key to both initial trials and repeat purchases. In a bold fusion, Jeremiah's Italian Ice teamed up with Hawaiian Hot T's to unveil "Island Fire." This innovative blend marries POG2 (passion fruit, orange, guava) with ghost and scorpion peppers, straddling the line between dessert and condiment. It's a tantalizing offering for the adventurous palate, especially those chasing Instagram-worthy flavor profiles. Beyond traditional uses, brands are reimagining flavored sauces as versatile marinades, salad dressings, and pizza drizzles. This strategy not only broadens their appeal but also boosts per-capita consumption by introducing new usage occasions.

Geography Analysis

North America maintains its market leadership with 37.40% share in 2025, driven by established consumer preferences for hot sauce consumption and the presence of major manufacturers like McCormick and Kraft Heinz. The region's mature market characteristics are reflected in the emphasis on premium positioning and flavor innovation, with companies investing heavily in brand differentiation and product line extensions. Regulatory pressures from FDA sodium reduction initiatives are forcing reformulation strategies that may create competitive advantages for companies that can maintain flavor integrity while meeting health guidelines. The region's foodservice sector strength, particularly in quick-service restaurants, provides stable volume demand while creating opportunities for bulk packaging and customizable flavor systems.

Asia-Pacific emerges as the fastest-growing region with 7.58% CAGR through 2031, reflecting urbanization trends, rising disposable incomes, and expanding middle-class consumption patterns. The region's growth is supported by cultural preferences for spicy foods and the integration of hot sauce into traditional cuisines, creating opportunities for both international brands and local manufacturers. Kikkoman's USD 560 million investment in a new Wisconsin production facility demonstrates the strategic importance of Asian companies in the global hot sauce market in June 2024.

Europe represents a significant growth opportunity driven by increasing consumer interest in international cuisines and spicy flavors. Germany leads European imports, followed by Spain and the United Kingdom, with strong demand for organic products and sustainable packaging solutions. The region's regulatory environment favors natural additives and clean-label products, creating opportunities for manufacturers who can meet these requirements while maintaining competitive pricing. South America and Middle East & Africa represent emerging markets with significant growth potential, driven by urbanization trends and expanding retail infrastructure, though these regions face challenges related to distribution networks and price sensitivity that may require adapted product formulations and packaging strategies.

- McCormick & Company, Inc.

- McIlhenny Company

- Huy Fong Foods, Inc.

- Baumer Foods, Inc.

- The Kraft Heinz Company

- Associated Manufacturers Limited (Walker Wood)

- Melinda's Foods LLC

- Kikkoman Corporation

- Conagra Brands, Inc.

- Goya Foods, Inc.

- MegaMex Foods (Herdez)

- La Costena

- TW Garner Food Company (Texas Pete)

- Tabanero Holdings, LLC.

- Extreme Foods (Blaire's)

- Habanero Foods International Private Limited

- Bushwick Kitchen LLC

- Truff

- Secret Aardvark Trading Co.

- Torchbearer Sauces

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of foodservice and quick-service restaurants

- 4.2.2 Globalization of ethnic and spicy cuisines

- 4.2.3 Product innovation and premiumization

- 4.2.4 Artificial Intelligence-driven flavour personalisation

- 4.2.5 Growing popularity of Home Cooking

- 4.2.6 Influencer-led DTC subscription models

- 4.3 Market Restraints

- 4.3.1 Health concerns over sodium, sugar, and capsaicin

- 4.3.2 Concern over raw material quality

- 4.3.3 Stringent food safety and labeling regulations

- 4.3.4 Supply chain disruptions

- 4.4 Value-Chain Analysis

- 4.5 Consumer Behaviour Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product Type

- 5.1.1 Red Hot Sauce

- 5.1.2 Green Hot Sauce

- 5.1.3 Yellow Hot Sauce

- 5.1.4 Others

- 5.2 Flavor

- 5.2.1 Plain

- 5.2.2 Flavored

- 5.3 Packaging

- 5.3.1 Bottles

- 5.3.2 Sachets and Pouches

- 5.3.3 Others

- 5.4 Distribution Channels

- 5.4.1 HoReCa/Foodservice

- 5.4.2 Retail

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Convenience Stores/Grocery Stores

- 5.4.2.3 Online Retail Stores

- 5.4.2.4 Other Distribution Channels

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Sweden

- 5.5.2.7 Belgium

- 5.5.2.8 Poland

- 5.5.2.9 Netherlands

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Thailand

- 5.5.3.5 Singapore

- 5.5.3.6 Indonesia

- 5.5.3.7 South Korea

- 5.5.3.8 Australia

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Peru

- 5.5.4.5 Chile

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 McCormick & Company, Inc.

- 6.4.2 McIlhenny Company

- 6.4.3 Huy Fong Foods, Inc.

- 6.4.4 Baumer Foods, Inc.

- 6.4.5 The Kraft Heinz Company

- 6.4.6 Associated Manufacturers Limited (Walker Wood)

- 6.4.7 Melinda's Foods LLC

- 6.4.8 Kikkoman Corporation

- 6.4.9 Conagra Brands, Inc.

- 6.4.10 Goya Foods, Inc.

- 6.4.11 MegaMex Foods (Herdez)

- 6.4.12 La Costena

- 6.4.13 TW Garner Food Company (Texas Pete)

- 6.4.14 Tabanero Holdings, LLC.

- 6.4.15 Extreme Foods (Blaire's)

- 6.4.16 Habanero Foods International Private Limited

- 6.4.17 Bushwick Kitchen LLC

- 6.4.18 Truff

- 6.4.19 Secret Aardvark Trading Co.

- 6.4.20 Torchbearer Sauces

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK