PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061838

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061838

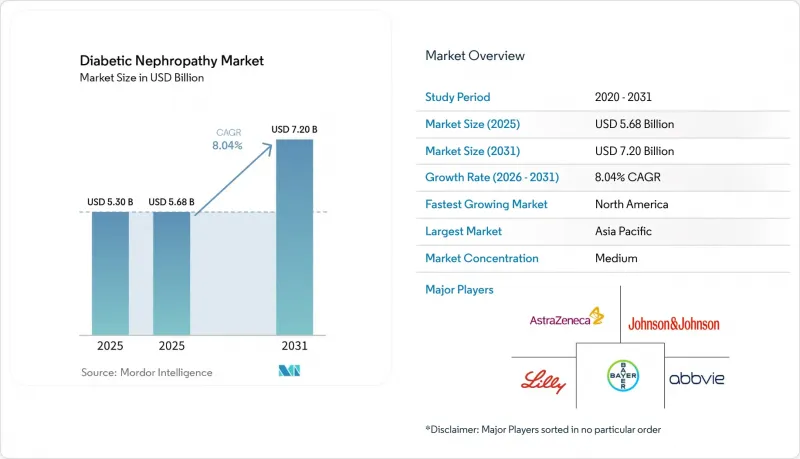

Diabetic Nephropathy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the diabetic nephropathy market size is expected to increase from USD 5.30 billion in 2025 to USD 5.68 billion in 2025 and reach USD 7.20 billion by 2031, growing at a CAGR of 8.04% over 2025-2031.

This report is Segmented by Product Type (Therapeutics, Diagnostics), Stage of Disease (Hyperfiltration, Micro-Albuminuria, Macro-Albuminuria, CKD Stage 3-4, ESRD), End User (Hospitals, Specialty Clinics, Dialysis Centres, Diagnostic Laboratories, Academic Institutes), Route of Administration (Oral, Injectable), and Geography (North America, Europe, Asia-Pacific, and More). Market Forecasts are in Value (USD).

Global Diabetic Nephropathy Market Trends and Insights

Escalating Global Diabetes Prevalence

In 2024, the global diabetic population reached 589 million adults, marking a 16% increase compared to 2021. Type 2 diabetes represents 90% of these cases, with 20-40% of patients developing diabetic nephropathy within a decade of diagnosis. This growth is concentrated in specific regions, with China and India collectively accounting for 241 million diabetics. However, rural areas in these countries report less than 30% screening penetration for albuminuria, highlighting a significant unmet demand that is expected to grow as national health insurance expands coverage for UACR testing and SGLT-2 inhibitors. In the Middle East and North Africa, diabetes prevalence exceeds 20% in Gulf Cooperation Council nations, driven by factors such as obesity and sedentary lifestyles. However, healthcare systems in these regions face challenges in biomarker testing, often relying on serum creatinine, which is insufficient for detecting early-stage kidney damage. Growth in these markets is primarily driven by epidemiological trends rather than regulatory interventions.

Ageing Population Accelerating CKD Burden

The global population aged 65 and older is expected to grow from 771 million in 2024 to 1.6 billion by 2050. Countries such as Japan, Italy, and Germany already report median ages above 47 years. Age-related nephron loss compounds the impact of diabetes, with non-diabetic individuals losing approximately 10% of glomeruli per decade after age 40. Diabetics with hypertension experience even greater nephron loss, reducing functional capacity by 30-50% over the same period. This demographic trend is particularly evident in North America and Europe, where healthcare systems have integrated early detection into routine care through annual eGFR monitoring for older diabetic patients. In contrast, Asia-Pacific nations face challenges as rapidly aging populations in countries like South Korea and Thailand coincide with underdeveloped chronic disease management systems. This has created demand for point-of-care UACR devices that bypass centralized laboratory delays. Compliance frameworks such as ISO 15189 are gaining traction in the region, ensuring quality standards for diagnostics.

Pay-for-Performance Nephrology Care Models

In 2024, CMS introduced the Comprehensive Kidney Care Contracting (CKCC) initiative, engaging 4,200 nephrologists who accepted financial risk. Providers face penalties of up to 5% of capitated payments if dialysis rates exceed benchmarks, while outperformers gain shared savings. Early 2024 data shows CKCC participants increased SGLT-2 inhibitor prescriptions by 31% and UACR testing by 18% compared to fee-for-service models, driven by incentives to delay ESRD progression. In Australia, Kidney Health Australia is advocating for comparable reforms, though fragmented state-level funding has delayed implementation. Pay-for-performance models favor oral therapeutics like SGLT-2 and GLP-1 due to simpler adherence monitoring and lower costs, disadvantaging IV-administered drugs like endothelin antagonists that require intensive safety oversight. Compliance with value-based care is becoming a competitive edge, with companies embedding real-world evidence teams to align with CKCC outcomes.

Other drivers and restraints analyzed in the detailed report include:

- Guideline-Mandated Annual Microalbumin Testing

- Rise of Urinary Multi-Omics Biomarker Panels

- Low Physician Awareness in Primary Care

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, therapeutics captured 66.90% of the market share, driven by the adoption of oral SGLT-2 inhibitors and GLP-1 receptor agonists in fixed-dose combinations. These combinations aim to enhance eGFR preservation while reducing the pill burden. Diagnostics, with a 33.10% share, are growing at an 8.15% CAGR through 2031, supported by the commercialization of biomarker panels like Cystatin-C, NGAL, and KIM-1, transitioning from research tools to clinical-grade assays. Within therapeutics, SGLT-2 inhibitors dominate, led by products like Farxiga and Jardiance, which gained FDA approval for CKD indications in 2021 and 2023, respectively. GLP-1 receptor agonists are the fastest-growing segment, with a 9.5% CAGR, fueled by the approval of semaglutide for diabetic kidney disease in 2025. Endothelin receptor antagonists and calcium-channel blockers serve niche roles, while ACE inhibitors and ARBs are losing prominence due to the superior outcomes of SGLT-2 inhibitors, though they remain prevalent in cost-sensitive markets.

Chronic Kidney Disease Stages 3-4 accounted for 42.35% of the market share in 2025, reflecting the trend of diagnoses occurring after eGFR drops below 60 mL/min/1.73m2, when symptoms prompt medical evaluation. The hyperfiltration segment is the fastest-growing, with a 9.40% CAGR, driven by early intervention models that reward proactive screening and treatment. Microalbuminuria (Stage 1) and macroalbuminuria (Stage 2) together represent about 35% of the market, with growth supported by guidelines promoting earlier screenings. End-stage renal disease (Stage 5) holds a smaller share as patients transition to dialysis or transplantation, though diagnostic services for ESRD patients remain a significant revenue driver.

Geography Analysis

In 2025, North America accounted for 39.67% of the market share, driven by CMS policies that reimburse SGLT-2 inhibitors and GLP-1 agonists for diabetic kidney disease under Medicare Part B. These policies, combined with Comprehensive Kidney Care Contracting models, support early-stage interventions. The U.S., with 34.8 million diabetics, faces a significant gap in care as only 48% of eligible patients receive annual UACR screenings, despite 37% showing kidney impairment. Health systems are addressing this gap through electronic health record alerts and pharmacist-led outreach. In Canada, while SGLT-2 inhibitors are covered under provincial formularies, reimbursement for advanced biomarkers like Cystatin-C remains inconsistent. This creates a two-tier diagnostic system, with provinces like Ontario and British Columbia offering advanced testing, while rural areas rely on serum creatinine methods.

Asia-Pacific is the fastest-growing region, with an 8.50% CAGR projected through 2031. Growth is fueled by China's 140 million diabetics, 20% of whom exhibit microalbuminuria. National policies mandating the inclusion of SGLT-2 inhibitors in provincial essential medicine lists ensure hospital access and drive price reductions of 50-70% through volume-based procurement. In India, the landscape is fragmented. Private hospitals in major cities like Delhi, Mumbai, and Bangalore provide comprehensive diabetic nephropathy care, including advanced biomarkers. However, government primary health centers in smaller cities lack basic UACR testing, pushing patients to private laboratories for self-funded diagnostics.

- Abbott Laboratories

- Abbvie

- AstraZeneca

- Bayer

- Beckton Dickinson

- Boehringer Ingelheim

- Chinook Therapeutics

- Eli Lilly and Company

- Roche

- GlaxoSmithKline

- Johnson & Johnson (Janssen / Invokana)

- Kyowa Kirin

- Merck

- Novo Nordisk

- Ortho Clinical Diagnostics

- Pfizer

- Quest Diagnostics

- Randox Laboratories

- Reata Pharmaceuticals

- Sanofi

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Diabetes Prevalence

- 4.2.2 Ageing Population Accelerating CKD Burden

- 4.2.3 Guideline-Mandated Annual Microalbumin Testing

- 4.2.4 Rise of Urinary Multi-Omics Biomarker Panels

- 4.2.5 Pay-for-Performance Nephrology Care Models

- 4.3 Market Restraints

- 4.3.1 Low Physician Awareness in Primary Care

- 4.3.2 Adverse-Event Concerns with Endothelin Antagonists

- 4.3.3 Limited Reimbursement for Novel Biomarker Tests

- 4.3.4 AI Diagnostic Algorithms Facing Regulatory Delay

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Therapeutics

- 5.1.1.1 ACE Inhibitors

- 5.1.1.2 Angiotensin II Receptor Blockers (ARBs)

- 5.1.1.3 SGLT-2 Inhibitors

- 5.1.1.4 Endothelin Receptor Antagonists

- 5.1.1.5 GLP-1 Receptor Agonists

- 5.1.1.6 Calcium-Channel Blockers

- 5.1.1.7 Others

- 5.1.2 Diagnostics

- 5.1.2.1 Urine Albumin-to-Creatinine Ratio (UACR)

- 5.1.2.2 24-h Urine Albumin

- 5.1.2.3 Serum Creatinine

- 5.1.2.4 Estimated GFR (eGFR) Algorithms

- 5.1.2.5 Imaging (Ultrasound, MRI)

- 5.1.2.6 Novel Biomarkers (Cystatin-C, NGAL, KIM-1, etc.)

- 5.1.2.7 Others

- 5.1.1 Therapeutics

- 5.2 By Stage of Disease

- 5.2.1 Hyperfiltration (Pre-clinical)

- 5.2.2 Micro-albuminuria (Stage 1)

- 5.2.3 Macro-albuminuria (Stage 2)

- 5.2.4 Chronic Kidney Disease (Stage 3-4)

- 5.2.5 End-Stage Renal Disease (Stage 5)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics

- 5.3.3 Dialysis Centres

- 5.3.4 Diagnostic Laboratories

- 5.3.5 Academic & Research Institutes

- 5.4 By Route of Administration (Therapeutics)

- 5.4.1 Oral

- 5.4.2 Injectable

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of MEA

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 AbbVie Inc.

- 6.3.3 AstraZeneca plc

- 6.3.4 Bayer AG

- 6.3.5 Beckman Coulter

- 6.3.6 Boehringer Ingelheim GmbH

- 6.3.7 Chinook Therapeutics

- 6.3.8 Eli Lilly and Company

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 GSK plc

- 6.3.11 Johnson & Johnson (Janssen / Invokana)

- 6.3.12 Kyowa Kirin

- 6.3.13 Merck KGaA

- 6.3.14 Novo Nordisk A/S

- 6.3.15 Ortho Clinical Diagnostics

- 6.3.16 Pfizer Inc.

- 6.3.17 Quest Diagnostics

- 6.3.18 Randox Laboratories

- 6.3.19 Reata Pharmaceuticals

- 6.3.20 Sanofi S.A.

- 6.3.21 Siemens Healthineers AG

- 6.3.22 Sysmex Corporation

- 6.3.23 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment