PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061864

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061864

Jellies And Gummies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

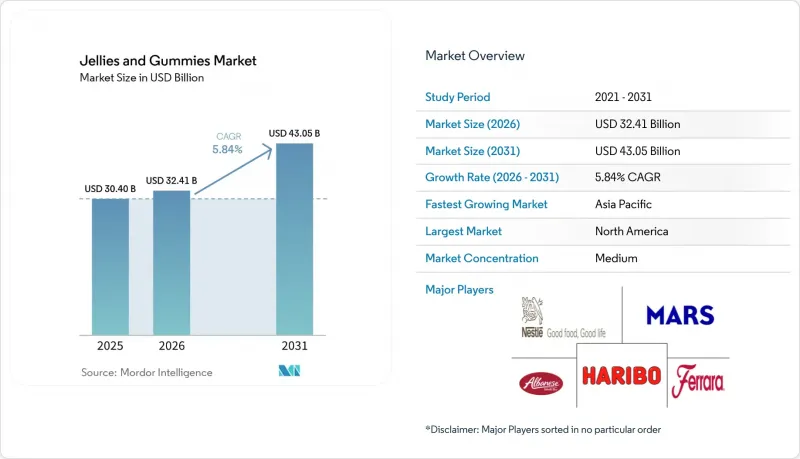

According to Mordor Intelligence, the jellies and gummies market size is expected to grow from USD 30.40 billion in 2025 to USD 32.41 billion in 2026 and is forecast to reach USD 43.05 billion by 2031 at a 5.84% CAGR over 2026-2031.

This report is Segmented by Product Type (Traditional, Functional, Sugar-Free/Low Sugar, Other), Ingredient Source (Gelatin-Based, Pectin/Plant-Based, Other Hydrocolloids), End User (Children/Kids, Adults), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Pharmacy/Drug Stores, Online Retail Stores, Other), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Jellies And Gummies Market Trends and Insights

Rising demand for functional confectionery

The increasing demand for functional confectionery is a significant driver of the global jellies and gummies market, as consumers seek products that combine indulgence with health benefits. Gummies have become a preferred format for delivering functional ingredients such as vitamins, minerals, probiotics, omega-3 fatty acids, and botanical extracts. They offer a more appealing and convenient alternative to traditional tablets and capsules. This trend is particularly prominent among younger consumers and working professionals who value ease of consumption and taste while maintaining a focus on wellness. In response, manufacturers are diversifying their product portfolios to include offerings targeted at immunity support, digestive health, beauty enhancement, and stress management. These products are often marketed with clean-label claims and reduced sugar content. The convergence of confectionery and nutraceuticals has further driven innovation in ingredient sourcing and formulation technologies. This enables brands to position gummies as both enjoyable treats and functional health supplements, thereby contributing significantly to market growth.

Innovation in flavors, shapes, and textures

Innovation in flavors, shapes, and textures is a key factor driving the global jellies and gummies market, enhancing consumer engagement and enabling product differentiation in a competitive environment. Manufacturers are expanding flavor offerings, ranging from traditional fruit options to exotic, sour, spicy, and hybrid combinations, to meet the changing taste preferences of various age groups and regions. Additionally, advancements in molding techniques have led to the creation of diverse shapes, including themed characters, filled centers, layered formats, and 3D designs, which are particularly appealing to children and impulse buyers. Texture innovations, such as dual-texture gummies, chewy-soft combinations, and aerated or foam-infused variants, further enhance the sensory experience and promote repeat purchases. These developments not only help brands differentiate themselves on retail shelves but also support premium positioning and seasonal or limited-edition product launches, contributing to increased consumption and sustained market growth.

Stringent regulations on sugar content and labeling

Stringent regulations on sugar content and labeling present a significant restraint on the global jellies and gummies market by increasing compliance costs and limiting manufacturers' flexibility in product formulation. Regulatory authorities in key markets require transparent disclosure of nutritional information, particularly sugar levels, subjecting confectionery products to heightened scrutiny. For example, the European Commission's Regulation (EU) No 1169/2011 mandates that all pre-packaged foods display detailed nutrition declarations, including sugar content per 100g or 100ml. This requirement limits the ability of brands to market high-sugar gummies as casual indulgences without clear disclosure. Similarly, the U.S. Food and Drug Administration requires labeling of "added sugars" with a recommended daily value of 50 grams based on a 2,000-calorie diet, increasing consumer awareness of sugar consumption. Additionally, the UK Department of Health & Social Care has introduced restrictions on the promotion and placement of high fat, sugar, and salt (HFSS) products, including bans on multibuy offers and prominent in-store placements, which directly affect impulse purchases of confectionery items like gummies. These regulatory measures compel manufacturers to invest in reformulation and labeling compliance while also limiting marketing strategies, thereby constraining market growth and profitability.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of plant-based and vegan product offerings

- Increasing demand for sugar-free and low-sugar alternatives

- High competition from alternative supplement formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional jellies and gummies accounted for a 41.53% market share in 2025, driven by their strong association with indulgence, nostalgia, and broad market appeal, solidifying their role in the global confectionery market. Their vibrant colors, playful shapes, and diverse flavors attract children and young consumers, while also appealing to adults seeking affordable treats and occasional indulgence. Ongoing innovation in taste profiles, spanning classic fruit flavors to sour, tangy, and exotic options, keeps the category dynamic and promotes repeat purchases. Seasonal launches, themed packaging, and collaborations with popular entertainment franchises further enhance visibility and encourage impulse buying. The widespread availability of these products across supermarkets, convenience stores, and online platforms, along with competitive pricing and bulk packaging formats, supports high-volume consumption and strengthens their position as a key segment within the jellies and gummies market.

Functional jellies and gummies are projected to grow at a CAGR of 6.27% through 2031, driven by the increasing integration of confectionery and wellness as consumers seek convenient and enjoyable ways to support their health. These products are emerging as alternatives to traditional supplement formats, offering benefits such as vitamins, minerals, probiotics, collagen, and herbal extracts in an easy-to-consume form. Growing awareness of preventive healthcare and demand for targeted solutions, including immunity support, digestive health, beauty enhancement, and stress relief, are boosting adoption across various age groups. Additionally, advancements in formulation technologies are enabling manufacturers to enhance ingredient stability, reduce sugar content, and incorporate plant-based or clean-label ingredients, improving product credibility. The combination of taste and functionality, supported by strong marketing emphasizing health benefits and lifestyle alignment, is driving the growth of functional jellies and gummies within the broader market.

Gelatin-based formulations accounted for 43.86% of the market in 2025, driven by their superior texture, elasticity, and sensory appeal. Gelatin provides the distinctive chewy and bouncy consistency that consumers often associate with traditional gummies, making it a preferred choice for both confectionery and certain functional applications. Its ability to deliver a clear, glossy appearance and maintain a stable structure across various formulations ensures consistent product quality at scale. Furthermore, gelatin is cost-effective and widely available, enabling manufacturers to produce gummies at competitive prices while maintaining desirable mouthfeel and flavor release. The ingredient also offers formulation flexibility, allowing for the seamless incorporation of colors, flavors, and active ingredients, which supports product innovation and addresses mass-market demand.

Pectin/plant-based alternatives are growing at a 6.36% CAGR through 2031, driven by the increasing shift toward vegan, vegetarian, and clean-label consumption patterns as consumers avoid animal-derived ingredients. Pectin, typically sourced from fruits, aligns with natural and plant-based positioning, making it appealing to health-conscious and ethically driven consumers. These gummies also cater to religious dietary requirements and allergen-sensitive groups, broadening their global consumer base. Additionally, brands are utilizing pectin-based formulations to introduce organic, non-GMO, and low-sugar variants, often paired with fruit-based flavors that enhance the perception of naturalness. While the texture of pectin-based gummies differs slightly from gelatin, advancements in formulation technologies are improving chewiness and stability, enabling plant-based gummies to compete more effectively while supporting premiumization and differentiation in the market.

Geography Analysis

North America accounted for a 41.11% market share in 2025, driven by strong demand for functional and fortified confectionery, supported by high consumer awareness of health and wellness. Gummies have gained popularity as a delivery format for supplements such as vitamins, collagen, and probiotics, offering a more enjoyable alternative to traditional pills. The region benefits from a well-established retail infrastructure and high e-commerce penetration, enhancing product accessibility and visibility. Continuous innovation in low-sugar, organic, and clean-label formulations aligns with growing concerns about sugar consumption. Additionally, premiumization trends and artisanal positioning appeal to adult consumers. Aggressive marketing, brand collaborations, and seasonal product launches further stimulate consumption across diverse age groups.

The Asia-Pacific market is expanding at a 6.61% CAGR through 2031, driven by rapid urbanization, rising disposable incomes, and evolving dietary habits. A large and youthful population base, particularly in countries like China and India, supports high demand for colorful, fun, and affordable confectionery products. Increasing health awareness is also encouraging the adoption of functional gummies, especially in urban centers where consumers are more receptive to nutraceutical innovations. The expansion of modern retail formats and the rapid growth of online shopping platforms have significantly improved product availability in both metropolitan and tier-2 cities. Additionally, local flavor adaptations and region-specific product innovations enable brands to cater to diverse taste preferences, further accelerating market growth.

In Europe, demand is driven by a strong preference for premium, organic, and plant-based gummies, alongside increasing regulatory focus on sugar reduction, which is encouraging reformulation and innovation. South America benefits from growing urban populations and expanding retail networks, where affordable confectionery products remain popular among price-sensitive consumers. In the Middle East and Africa, rising youth demographics, increasing westernization of diets, and expanding supermarket and convenience store channels are fueling demand. Across these regions, product diversification, including halal-certified and gelatin-free variants, along with improved distribution and marketing strategies, plays a crucial role in sustaining market expansion.

- Mars Inc

- Ferrara Candy Company

- Haribo GmbH & Co. KG

- Albanese Confectionery Group, Inc.

- Nestle S.A.

- Perfetti Van Melle

- Cloetta AB

- Albanese Confectionery Group

- Jelly Belly Candy Company

- Trolli GmbH

- Lotte Confectionery

- Meiji Holdings Co., Ltd.

- Yupi Indo Jelly Gum

- Amos Food Group (4D)

- Lamy Lutti

- SmartSweets Inc.

- First Choice Candy

- Valeo Foods Group ( Barratt)

- Van Vliet The Candy Company BV (DE bron)

- The Fini Company

- SmartyPants Vitamins

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for functional confectionery

- 4.2.2 Innovation in flavors, shapes, and textures

- 4.2.3 Expansion of plant-based and vegan product offerings

- 4.2.4 Increasing demand for sugar-free and low-sugar alternatives

- 4.2.5 Growing popularity of personalized nutrition

- 4.2.6 Strong influence of social media and digital marketing

- 4.3 Market Restraints

- 4.3.1 Stringent regulations on sugar content and labeling

- 4.3.2 High competition from alternative supplement formats

- 4.3.3 Product recalls and safety concerns

- 4.3.4 Texture and taste limitations in sugar-free variants

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Traditional Jellies and Gummies

- 5.1.2 Functional Jellies and Gummies

- 5.1.3 Sugar-Free/Low Sugar Jellies and Gummies

- 5.1.4 Other Product Types

- 5.2 By Ingredient Source

- 5.2.1 Gelatin-Based

- 5.2.2 Pectin/Plant-Based (Vegan)

- 5.2.3 Other Hydrocolloids

- 5.3 By End User

- 5.3.1 Children/Kids

- 5.3.2 Adults

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Pharmacy/Drug Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Netherlands

- 5.5.2.8 Sweden

- 5.5.2.9 Belgium

- 5.5.2.10 Poland

- 5.5.2.11 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Indonesia

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 New Zealand

- 5.5.3.10 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Egypt

- 5.5.5.5 Morocco

- 5.5.5.6 Turkey

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Share, Products, Recent Developments)

- 6.4.1 Mars Inc

- 6.4.2 Ferrara Candy Company

- 6.4.3 Haribo GmbH & Co. KG

- 6.4.4 Albanese Confectionery Group, Inc.

- 6.4.5 Nestle S.A.

- 6.4.6 Perfetti Van Melle

- 6.4.7 Cloetta AB

- 6.4.8 Albanese Confectionery Group

- 6.4.9 Jelly Belly Candy Company

- 6.4.10 Trolli GmbH

- 6.4.11 Lotte Confectionery

- 6.4.12 Meiji Holdings Co., Ltd.

- 6.4.13 Yupi Indo Jelly Gum

- 6.4.14 Amos Food Group (4D)

- 6.4.15 Lamy Lutti

- 6.4.16 SmartSweets Inc.

- 6.4.17 First Choice Candy

- 6.4.18 Valeo Foods Group ( Barratt)

- 6.4.19 Van Vliet The Candy Company BV (DE bron)

- 6.4.20 The Fini Company

- 6.4.21 SmartyPants Vitamins

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK