PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061893

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061893

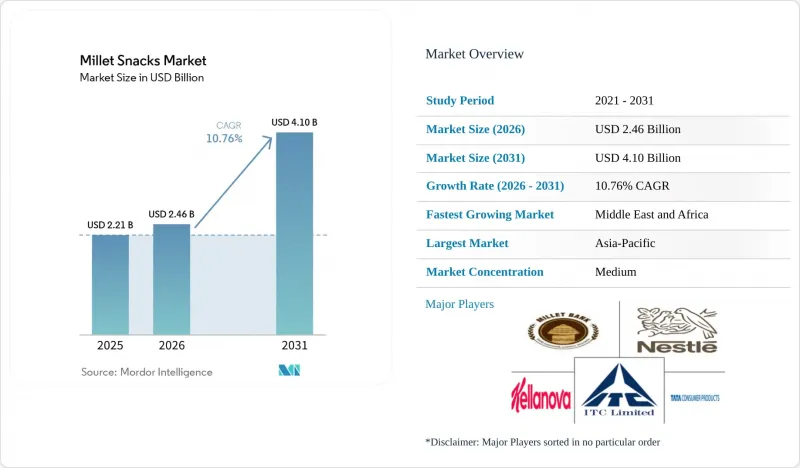

Millet Snacks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the millet snacks market size is projected to expand from USD 2.21 billion in 2025 and USD 2.46 billion in 2026 to USD 4.10 billion by 2031, registering a CAGR of 10.76% between 2026 and 2031.

This report is Segmented by Product Type (Chips and Crisps, Puffs, Bars and Granola, and More), Form (Fried and Baked), Millet Type (Finger Millet, Pearl Millet, and More), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Millet Snacks Market Trends and Insights

Gluten-Free and Allergen-Free Snacking Boom

Globally, celiac disease prevalence has stabilized at around 1%. However, non-celiac gluten sensitivity impacts an estimated 6-10% of populations in developed markets. This creates a consistent demand for gluten-free ancient grain snacks, as highlighted by the National Institutes of Health. Millets, being inherently gluten-free and hypoallergenic, are increasingly favored in formulations catering to diverse dietary restrictions. This is especially pertinent given the rising co-occurrence of gluten sensitivity and other food allergies. The Whole Grains Council found that 84% of US consumers trust products with the Whole Grain Stamp. Furthermore, 81% show a heightened intent to purchase items bearing the stamp, indicating a direct correlation between awareness and sales. Regulatory changes bolster this trend. The FDA's 2022 revision of the "healthy" nutrient content claim and 2023 sodium-reduction guidance encourage a shift towards whole grains. In contrast, the Pan American Health Organization's octagon warning-label mandate, affecting over 30 countries, penalizes snacks made from refined flour. Manufacturers are capitalizing on these insights, marketing millet snacks as both gluten-free and whole-grain to appeal to a broader audience. A case in point is Tata Soulfull's May 2026 debut of Corn Flakes+, which integrates finger millet for enhanced fiber content while proudly flaunting its gluten-free certification.

Government Initiatives and Support Programs

Since its inception in 2018-19, India's National Food Security Mission - Nutri Cereals has allocated a substantial INR 793.27 crore (USD 95.2 million) under the PLI scheme to 29 companies by 2024-25. This funding, as reported by the Ministry of Food Processing Industries, Government of India, has been directed towards millet procurement, bolstering processing infrastructure, and advancing research and development. Additionally, through the PMFME scheme, this subsidy has reached 4,366 millet entrepreneurs, disbursing loans amounting to INR 226.40 crore (USD 27.2 million) and establishing 17 incubation centers. The impact of these policies is evident in the production metrics: India's millet output hit 180.15 lakh tonnes in 2024-25. Furthermore, sales of millet-based packaged foods skyrocketed from INR 35 crore (USD 4.2 million) in 2020-21 to an impressive INR 814 crore (USD 97.7 million) in 2024-25, marking a staggering 23.3-fold increase, as highlighted by the Ministry of Agriculture & Farmers Welfare, Government of India. To bolster these efforts, over 10 Indian states have initiated state-level millet missions. Coupled with a hike in the Minimum Support Price (MSP) - notably, ragi's MSP saw an increase of INR 596 per quintal in 2025-26 - these measures aim to de-risk farmer adoption and ensure a steady availability of raw materials. On a broader scale, African nations, with the backing of FAO's technical assistance, are championing millet cultivation as a climate-resilient crop. Notably, both Nigeria and Ethiopia have been ramping up their millet acreage by an impressive 12-15% annually since 2024. Highlighting the global momentum, the UN's proclamation of 2023 as the International Year of Millets spurred a flurry of activity, leading to the launch of over 500 new millet-based SKUs within just a year.

Sensory Acceptance for Taste and Texture

Millet, with its nutty and slightly bitter flavor profile, presents challenges in markets accustomed to lighter and sweeter snack textures. The EAT-GlobeScan 2024 survey highlighted flavor and taste as the second-most significant barrier to plant-based food adoption, cited by 35% of respondents, just behind price concerns. While extrusion processing offers a solution, it's not without limitations. Twin-screw extruders, set at 140-160°C and maintaining 18-20% moisture content, can achieve expansion ratios between 1.24 and 3.95. This produces a puffed texture reminiscent of traditional corn-based snacks. Yet, these ratios fall short of corn's potential 4.5-5.0 expansion, leading to a denser product that some consumers find less appealing. To counteract millet's inherent bitterness, flavor-masking techniques are employed. Co-extrusion with a 20-30% blend of chickpea flour not only neutralizes the bitterness but also boosts protein content. Additionally, post-extrusion seasoning with robust flavors like barbecue, cheese, or chili-lime effectively masks millet's base notes. PepsiCo's Kurkure Jowar Puffs, introduced in September 2025, exemplified this strategy. By combining sorghum, a grain closely related to millet, with a bold masala seasoning, they achieved a remarkable 38% trial rate in urban Indian markets within just three months. Furthermore, to minimize launch failures, sensory testing now involves trained panels and consumer acceptance metrics, typically aiming for a score of 6.5 or higher on a 9-point hedonic scale. While this approach has proven effective, it does extend development timelines by an additional 4 to 6 months.

Other drivers and restraints analyzed in the detailed report include:

- Health-Conscious Consumers Seeking High-Fiber Ancient Grains and Superfoods

- Rise of Plant-Based and Whole-Grain Diets

- Competition from Established Snack Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Puffs are set to grow at a CAGR of 11.08% through 2031, outpacing the overall market's 10.76% growth. This is driven by manufacturers using hot-air puffing machines (HAPM) at 300°C for oil-free expansion while preserving micronutrients. In 2025, chips and crisps held a 39.59% market share due to consumer familiarity and versatile flavors but faced margin pressures from fluctuating potato and corn prices. Bars and granola, positioned as premium products, leveraged convenience and clean-label appeal to price 50-70% higher than chips. However, their growth is limited by a 6-9 month shelf-life and crumbly textures. Cookies and biscuits, popular for tea-time and breakfast, saw ITC's Sunfeast Farmlite Super Millets Cookies distributed in over 85,000 outlets by May 2025. Yet, the segment's 8.9% CAGR is hindered by sugar content concerns. Breakfast cereals and muesli are gaining traction among health-conscious consumers. Tata Soulfull's Corn Flakes+, launched in May 2026, doubled fiber content to 4.3 g per serving, meeting FDA "healthy" claim standards. The "Others" category, including millet-based pasta, noodles, and savory mixes, remains nascent but attracts innovation.

Extrusion technology drives puff growth: twin-screw extruders achieve expansion ratios of 1.24 to 3.95 for multi-millet blends (finger, pearl, foxtail). Key parameters include die configuration, barrel temperature (140-160°C), and moisture content (18-20%). Barnyard millet snacks reached a 3.949 expansion ratio, nearing corn's 4.5-5.0 benchmark. PepsiCo's Kurkure Jowar Puffs, launched in September 2025, combined sorghum with masala seasoning, achieving a 38% trial rate in urban Indian markets within three months. Chips and crisps face innovation challenges; vacuum-frying reduces oil by 30-40% but raises costs by 15-20%, limiting adoption to premium SKUs. Bars and granola struggle with millet's low gluten content, requiring alternative binders like dates or chicory root fiber, complicating formulations. Breakfast cereals use millet's low glycemic index (54-68 vs. wheat's 70-85) to target diabetic and prediabetic consumers, a group projected to exceed 700 million globally by 2045, per the International Diabetes Federation.

Fried variants are set to grow at a CAGR of 11.97% through 2031, surpassing baked formats' growth despite baked's 65.69% market share in 2025. Innovations like vacuum-frying and air-puffing are enhancing fried snacks' health appeal. Vacuum-frying, operating at 90-120°C under reduced pressure (5-10 kPa), reduces oil absorption by 30-40% and preserves heat-sensitive vitamins like thiamine and riboflavin. This positions fried snacks as "better-for-you" options, appealing to consumers seeking indulgent textures without guilt. Baked formats, dominant through 2025 due to clean-label trends, face sensory drawbacks, such as 18-22% lower crispness scores and shorter shelf-life (8-9 months vs. 12 months for fried).

Air-puffing, using hot-air puffing machines (HAPM) at 300°C, eliminates oil while achieving expansion ratios of 2.8-3.2 for finger millet. Bonvie Snacks' Millet Chips - Mint, launched in May 2025, used air-puffing to deliver 4.1 g fiber per 30 g serving with zero trans fat, earning USDA Organic and Non-GMO Project Verified certifications. Regulatory changes, like the FDA's 2023 sodium-reduction guidance and the Pan American Health Organization's octagon warning-label mandate, penalize high-sodium baked snacks, leveling competition. Fried formats also cater to ethnic flavors like chili-lime and masala, appealing to growing diaspora segments in North America and Europe. While baked formats dominate institutional channels due to low-fat policies, fried snacks are regaining ground in retail through improved processing and targeted marketing.

Geography Analysis

Asia-Pacific, holding a 48.40% market share in 2025, is expected to maintain its lead through 2031. India's production of 180.15 lakh tonnes in 2024-25, representing 38.4% of global millet output, and government policies allocating INR 793.27 crore (USD 95.2 million) under the PLI scheme to 29 millet-processing companies, drive this growth. Millet-based packaged food sales in India rose from INR 35 crore (USD 4.2 million) in 2020-21 to INR 814 crore (USD 97.7 million) in 2024-25, a 23.3-fold increase, driven by over 500 new SKU launches following the UN's 2023 International Year of Millets declaration. In China, millet consumption is concentrated in northern provinces like Shanxi and Hebei, while urbanization and Western dietary trends are boosting snack-format adoption in tier-1 cities, with modern retail channels growing 14-16% annually. Japan's USD 30 billion health-food market increasingly incorporates millets into functional snacks targeting elderly consumers (28.4% of the population aged 65+), focusing on bone health and glycemic control. Thailand, Indonesia, and South Korea are seeing gluten-free product launches rise 18-22% annually since 2024, driven by expatriate communities and health-conscious millennials. Australia's organic snack market, growing at 12% CAGR, positions millets as a native alternative to imported quinoa, with retailers like Woolworths and Coles increasing millet SKU counts by 30% in 2025.

The Middle East and Africa, growing at 11.92% CAGR through 2031, lead regional growth. Yemen's per-capita consumption of 47,000 tonnes (35% of the regional total) and the UAE's 22,000 tonnes consumption drive demand. Nigeria and Ethiopia, Africa's largest millet producers, are expanding acreage by 12-15% annually with FAO support to promote climate-resilient crops. The UAE's retail sector, led by Carrefour and Lulu, stocks millet snacks in "free-from" sections catering to expatriate demand. Saudi Arabia's Vision 2030 allocates SAR 500 million (USD 133 million) to millet-processing clusters in Al-Qassim and Hail. South Africa's urban centers see rising millet-snack penetration in Woolworths and Pick'n Pay, driven by health-conscious consumers and government nutrition campaigns. Egypt and Morocco leverage Mediterranean diets to position millets as alternatives to imported wheat, with brands like Mansour Group launching millet-based biscuits in 2025.

North America, with a 25% market share in 2025, is led by the U.S., where gluten-free and ancient-grain segments exceed USD 8 billion in annual sales. Health snack shelf space grew 22% in 2024, with retailers like Whole Foods and Walmart dedicating 12-15% of snack aisles to millet-based products. Canada's millet snack market benefits from multicultural demographics, with South Asian, African, and Middle Eastern communities (22% of the population) easing adoption. Tata Consumer's Joyfull Millets muesli launched in Canada in June 2024, securing listings in 450+ cafeterias within 6 months. Mexico's snack market, dominated by corn-based products, is seeing millet chips gain traction in premium supermarkets in urban centers. Europe, with a 30% market share in 2025, is led by the UK, Germany, and France. UK retailers like Tesco expanded millet SKU counts by 25% in 2025, positioning them in "Free From" aisles. Germany's Bio-Siegel and EU Organic certifications enable millet snacks to access premium channels like Alnatura. France's Nutri-Score labeling, favoring high-fiber, low-sodium products, boosts millet snacks' visibility. South America, the smallest market, sees Brazil, Argentina, and Colombia growing at 9-11% CAGRs, driven by urbanization and health-awareness campaigns.

- Tata Consumer Products Limited

- Minkan Agro Industries Private Limited

- ITC Limited

- Nestle S.A.

- Kellanova

- Haldiram Snacks Food Pvt Ltd.

- Britannia Industries Limited

- Mformillet Foods Private Limited (TrooGood)

- Brahhm Arpan Organic Private Limited

- Wholsum Foods

- Yummy Valley

- Kiru Millet Snacks

- Nutty Yogi

- Urban Millets Private Limited

- Southern Health Foods Private Limited (Manna Foods)

- Mrida Group (Earthspired)

- Nutraahaar Foods Private Limited

- Aggarwal Group

- Supreem Super Foods

- Millet Maagic Meal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Gluten-free and allergen-free snacking boom

- 4.2.2 Government initiatives and support programs

- 4.2.3 Health-conscious consumers seeking high-fiber "ancient grains" and superfoods

- 4.2.4 Rise of plant-based and whole-grain diets

- 4.2.5 Appeal to convenience and on-the-go snacking

- 4.2.6 Demand for clean-label and natural food products

- 4.3 Market Restraints

- 4.3.1 Sensory acceptance for taste and texture

- 4.3.2 Competition from established snack alternatives

- 4.3.3 Low consumer awareness and familiarity

- 4.3.4 High retail prices compared to alternatives

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Chips and Crisps

- 5.1.2 Puffs

- 5.1.3 Bars and Granola

- 5.1.4 Cookies and Biscuits

- 5.1.5 Breakfast Cereal and Muesli

- 5.1.6 Others

- 5.2 Form

- 5.2.1 Fried

- 5.2.2 Baked

- 5.3 Millet Type

- 5.3.1 Finger Millet

- 5.3.2 Pearl Millet

- 5.3.3 Foxtail Millet

- 5.3.4 Little Millet

- 5.3.5 Others

- 5.4 Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Specialty Health Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Others

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Sweden

- 5.5.2.7 Belgium

- 5.5.2.8 Poland

- 5.5.2.9 Netherlands

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Thailand

- 5.5.3.5 Singapore

- 5.5.3.6 Indonesia

- 5.5.3.7 South Korea

- 5.5.3.8 Australia

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Peru

- 5.5.4.5 Chile

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Tata Consumer Products Limited

- 6.4.2 Minkan Agro Industries Private Limited

- 6.4.3 ITC Limited

- 6.4.4 Nestle S.A.

- 6.4.5 Kellanova

- 6.4.6 Haldiram Snacks Food Pvt Ltd.

- 6.4.7 Britannia Industries Limited

- 6.4.8 Mformillet Foods Private Limited (TrooGood)

- 6.4.9 Brahhm Arpan Organic Private Limited

- 6.4.10 Wholsum Foods

- 6.4.11 Yummy Valley

- 6.4.12 Kiru Millet Snacks

- 6.4.13 Nutty Yogi

- 6.4.14 Urban Millets Private Limited

- 6.4.15 Southern Health Foods Private Limited (Manna Foods)

- 6.4.16 Mrida Group (Earthspired)

- 6.4.17 Nutraahaar Foods Private Limited

- 6.4.18 Aggarwal Group

- 6.4.19 Supreem Super Foods

- 6.4.20 Millet Maagic Meal

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK