PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061942

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061942

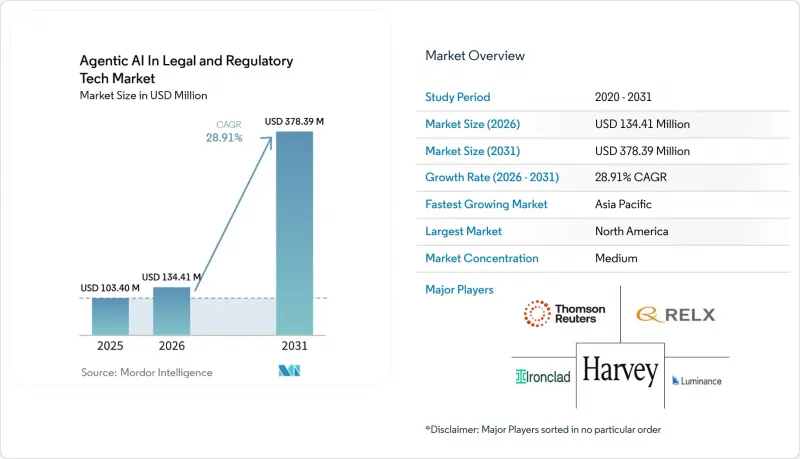

Agentic AI In Legal And Regulatory Tech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the agentic AI market in the legal and regulatory tech market is expected to grow from USD 103.4 million in 2025 to USD 134.41 million in 2026, and is forecast to reach USD 478.39 million by 2031 at a 28.91% CAGR over 2026-2031.

This report is Segmented by Application (Contract Lifecycle Management Agents, Ediscovery and Document Review Agents, and More), Deployment Model (Cloud-Based, and More), End-User Industry (Law Firms, Corporate Legal Departments, and More), Core Technology (Machine-Learning and Predictive Models, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In Legal And Regulatory Tech Market Trends and Insights

Accelerating Mainstream Adoption of GenAI Tools Within Legal Workflows

Corporate Legal Operations Consortium data show that 52% of corporate legal teams had production-grade generative AI systems in 2025, more than double the prior year, and 85% had an internal AI committee guiding policy. Widespread committees signal permanent budget lines rather than one-off pilots. Thomson Reuters noted that 40% of legal professionals now use generative AI and 53% expect to add fully autonomous agents within 12 months. The steep curve is unique because LLMs require minimal custom coding, giving mid-market firms immediate access to capabilities once reserved for the exclusive domain of large firms.

Cost-Reduction Imperatives Amid Rising Outside-Counsel Fees

Thomson Reuters reported an 8.3% blended-rate increase for outside counsel in 2024, prompting corporate legal heads to expand in-house teams and adopt AI-driven review tools that replace low-complexity external work. A 500-attorney firm documented a drop in intake time from 48 hours to 5 minutes after deploying AI-supported triage, cutting partner hours and improving responsiveness. Legal operations groups increasingly rank technology proficiency as a talent-retention factor, linking cost control to workforce strategy.

Data-Privacy And Privilege Concerns Over Cloud-Hosted LLM Inference

A February 2026 ruling in US v. Heppner declared that using consumer chatbots without contractual protections waived attorney-client privilege. The decision accelerated migration to enterprise-grade tiers that promise zero-retain data handling, regional residency controls, and SOC 2 Type II attestations. Forty-seven state bars now require written client consent before confidential data passes through AI tools. Risk-averse general counsel in healthcare and finance are delaying deployments until vendors deliver on-premises or hybrid options.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-First Digital-Transformation Initiatives Across Legal Operations

- Increasing Regulatory Scrutiny Demanding Audit-Ready Compliance Automation

- Hallucination Liability And Ethical-Competence Obligations For Attorneys

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, eDiscovery and document review agents secured 34.89% of the agentic AI (artificial intelligence) market share in the legal and regulatory tech market, a dominance driven by their ability to cut discovery budgets that often exceed USD 1 million per matter. Relativity's aiR for Review reached 90% accuracy in privilege classification, halving human review hours. Litigation outcome prediction agents, though smaller today, are forecast to expand at a 30.11% CAGR, adding significant volume to the agentic artificial intelligence market in legal and regulatory tech by 2031.

Rapid adoption of predictive analytics stems from firms seeking data-backed settlement ranges and venue strategies. Lex Machina's judge analytics module is now standard among 60% of AmLaw 200 practices. At the same time, contract-lifecycle agents attract corporate legal departments eager to shorten negotiation cycles, as evidenced by Ironclad's USD 150 million Series F funding. Compliance-intelligence and IP-management agents round out demand, especially in sectors with intensive regulatory duties or large patent estates.

Cloud platforms accounted for 61.89% of revenue in 2025, confirming that most buyers prefer subscription economics and continuous model upgrades. The agentic artificial intelligence in legal and regulatory tech market therefore remains closely tied to hyperscaler GPU availability. However, edge and embedded deployments are growing at a 29.71% CAGR because sensitive data, such as cross-border M&A, must remain within firm firewalls. This shift is expanding the agentic artificial intelligence in the legal and regulatory tech market size for hardware-optimized inference appliances.

Hybrid architectures allow routine work to stay in the cloud while confidential data is processed on-premises, but they also introduce API duplication costs. Large AmLaw firms with legacy document systems often choose on-premises clusters to integrate with existing records. Meanwhile, practice-management vendors embed lightweight LLMs so that small firms can gain agentic features without juggling multiple logins.

Geography Analysis

North America accounted for 41.89% of 2025 revenue for agentic AI in the legal and regulatory tech market. AmLaw 100 firms and Fortune 500 legal operations drive volume through cross-practice rollout of contract lifecycle and compliance agents. Enterprise adoption surged after the US District Court for the Southern District of New York clarified privilege obligations in February 2026. Canada's growth is steadier; Toronto firms favor eDiscovery agents to stay competitive with U.S. counterparts, while Mexico sees uptake mainly among multinational subsidiaries complying with the United States-Mexico-Canada Agreement.

Asia-Pacific is projected to record a 29.91% CAGR through 2031, the fastest worldwide. China's Smart Courts handle more than 30 million cases annually using AI case-routing and sentencing support. Japan's ministry pilots AI-enabled contract review to modernize corporate transactions, while India's digital court projects raise demand for budget-friendly research agents. Singapore's Smart Nation strategy and South Korea's regulatory complexity in semiconductors and finance add further momentum.

Europe trails slightly but benefits from GDPR enforcement and active cross-border M&A, expanding the agentic AI market within the bloc's legal and regulatory tech. Magic Circle firms in London buy orchestration platforms to manage multi-jurisdictional due diligence, while German practices focus on EU AI Act compliance audits. France's start-up scene cultivates contract negotiation agents tuned to civil-law systems. The Middle East, led by the United Arab Emirates and Saudi Arabia, is adopting sovereign-AI mandates to implement compliance and dispute-resolution tools. In Africa, adoption is concentrated in South Africa and Egypt due to infrastructure gaps elsewhere.

- Thomson Reuters Corporation

- RELX PLC

- LexisNexis Legal & Professional

- Harvey AI Inc.

- Ironclad Inc.

- Luminance Technologies Ltd.

- Casetext Inc.

- Everlaw Inc.

- DISCO Inc.

- Relativity ODA LLC

- Icertis Inc.

- ContractPod Technologies Ltd.

- Kira Systems Inc.

- Exterro Inc.

- Reveal-Brainspace Inc.

- Evisort Inc.

- SirionLabs Pte. Ltd.

- LinkSquares Inc.

- SpotDraft Inc.

- Onit Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Mainstream Adoption of GenAI Tools Within Legal Workflows

- 4.2.2 Cost-Reduction Imperatives Amid Rising Outside-Counsel Fees

- 4.2.3 Cloud-First Digital-Transformation Initiatives Across Legal Operations

- 4.2.4 Increasing Regulatory Scrutiny Demanding Audit-Ready Compliance Automation

- 4.2.5 Under-Served Demand for Multi-Agent Orchestration in Cross-Border Matters

- 4.2.6 Emerging VC-Backed Point Solutions Targeting Niche Litigation Tasks

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Privilege Concerns Over Cloud-Hosted LLM Inference

- 4.3.2 Hallucination Liability and Ethical-Competence Obligations for Attorneys

- 4.3.3 Fragmented Legacy Systems Limiting Seamless AI Integration

- 4.3.4 Under-Reported Shortage of Legal-Domain AI Talent for Model Fine-Tuning

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Contract Lifecycle Management Agents

- 5.1.2 eDiscovery and Document Review Agents

- 5.1.3 Legal Research and Analytics Agents

- 5.1.4 Compliance and Regulatory Intelligence Agents

- 5.1.5 Litigation Outcome Prediction Agents

- 5.1.6 IP-Management Agents

- 5.2 By Deployment Model

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.2.4 Edge / Embedded

- 5.3 By End-User Industry

- 5.3.1 Law Firms

- 5.3.2 Corporate Legal Departments

- 5.3.3 Financial-Services Compliance Units

- 5.3.4 Government and Regulatory Bodies

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Insurance

- 5.3.7 Technology and Telecom

- 5.4 By Core Technology

- 5.4.1 Machine-Learning and Predictive Models

- 5.4.2 Rule-based Expert Systems

- 5.4.3 Large-Language-Model (GenAI) Agents

- 5.4.4 Multi-agent Orchestration Platforms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Thomson Reuters Corporation

- 6.4.2 RELX PLC

- 6.4.3 LexisNexis Legal & Professional

- 6.4.4 Harvey AI Inc.

- 6.4.5 Ironclad Inc.

- 6.4.6 Luminance Technologies Ltd.

- 6.4.7 Casetext Inc.

- 6.4.8 Everlaw Inc.

- 6.4.9 DISCO Inc.

- 6.4.10 Relativity ODA LLC

- 6.4.11 Icertis Inc.

- 6.4.12 ContractPod Technologies Ltd.

- 6.4.13 Kira Systems Inc.

- 6.4.14 Exterro Inc.

- 6.4.15 Reveal-Brainspace Inc.

- 6.4.16 Evisort Inc.

- 6.4.17 SirionLabs Pte. Ltd.

- 6.4.18 LinkSquares Inc.

- 6.4.19 SpotDraft Inc.

- 6.4.20 Onit Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment