PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061965

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061965

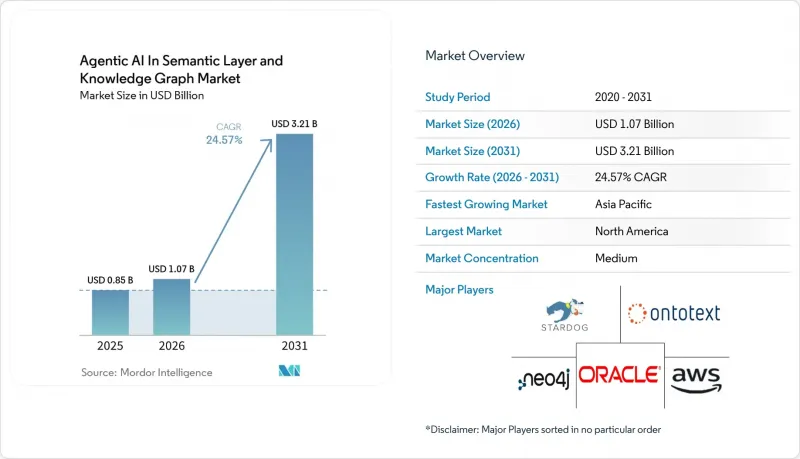

Agentic AI In Semantic Layer And Knowledge Graph - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the agentic AI market in the semantic layer and knowledge graph market size is expected to grow from USD 0.85 billion in 2025 to USD 1.07 billion in 2026, and is forecast to reach USD 3.21 billion by 2031 at a 24.57% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Knowledge-Graph Type (Enterprise Knowledge Graph, and More), Application (Customer and 360-View Analytics, and More ), Deployment Mode (Cloud, and On-Premises), End-User Industry (BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In Semantic Layer And Knowledge Graph Market Trends and Insights

Rising Enterprise Adoption of Agentic AI for Autonomous Workflows

Enterprise adoption of autonomous agents has moved beyond experimentation, and that shift is increasing demand for governed semantic structures that can serve as reliable memory across enterprise systems. In the agentic AI market for the semantic layer and knowledge graph, this change matters because agents need persistent context, clear relationships, and traceable logic before they can operate across finance, operations, and customer workflows. Neo4j moved this trend closer to production in February 2026 when it launched Aura Agent in general availability with automated ontology-driven agent construction and hosted MCP deployment for AuraDB customers. Microsoft also extended enterprise agent workflows in May 2026 by introducing Dataverse Business Skills into public preview, enabling organizations to encode processes and operational logic as instructions discoverable by AI agents via the Dataverse MCP server. These launches show why the agentic AI in the semantic layer and knowledge graph market is being shaped by production needs rather than pilot activity, especially where enterprises want auditable agent actions across many systems.

Accelerating Shift from Data Lakes to Semantic Data Fabrics

Enterprises are moving away from passive data lakes because raw and disconnected data structures do not provide the policy-aware context that agent systems need for dependable reasoning. The agentic AI in the semantic layer and knowledge graph market is benefiting from that shift because semantic layers can present enterprise data in a governed, interpretable form, rather than exposing agents to schema complexity. Microsoft Research reported that GraphRAG achieved 86% multi-hop enterprise query accuracy, compared with 32% for the baseline vector RAG, which helps explain why richer semantic context is gaining priority in enterprise AI architecture. Europe is also reinforcing this direction because AI governance rules are increasing the need for data lineage, technical documentation, and explainable system behavior in high-risk deployments. A related scientific study argued for open knowledge graph-based mapping between AI Act requirements and standards, which further supports the role of semantic structures in governed enterprise AI environments.

High Total Cost of Ownership for Large-Scale Knowledge Graph Projects

Large-scale knowledge graph programs still carry a high ownership burden because infrastructure, schema design, entity resolution, curation, and ongoing governance costs extend far beyond software purchase decisions. In the agentic AI market for the semantic layer and knowledge graph, this cost pressure is especially relevant for mid-sized organizations that may want graph-grounded agents but cannot justify large specialist teams or multi-stage implementation programs. Vendor product design shows that the market is trying to reduce this burden, with Neo4j launching Fleet Manager in December 2025 as a unified control plane for cloud, hybrid, and on-premises graph deployments. Hyperscaler-managed services are also reducing some operational overhead, as AWS continues to expand Neptune Analytics and add features that would otherwise require more direct engineering effort from customers. Even with these improvements, the agentic AI in the semantic layer and knowledge graph market still faces slower adoption, where buyers see ontology engineering and graph freshness as long-running cost centers rather than one-time project tasks.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Availability of Vector-Enabled Graph Databases

- Surging Demand for Real-Time 360-View Customer Analytics In BFSI

- Shortage of Qualified Knowledge Graph Engineers and Ontologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 62.87% of revenue in 2025, maintaining its leading position across the component mix. That weighting reflected the cost of platform licensing, query engines, ontology management tools, and embedded vector search capabilities that must be in place before an enterprise graph becomes operationally useful. In the agentic AI market for the semantic layer and knowledge graph, software also benefited from heavy customization requirements, as many deployments still begin with tailored schema design and integration work. The early revenue mix, therefore, favored platform vendors that could supply core graph infrastructure before broader service ecosystems matured.

Services are projected to grow at a 24.97% CAGR from 2026 to 2031, indicating that buyers are increasingly paying for implementation support after platform purchase. In the agentic AI in the semantic layer and knowledge graph industry, this shift is tied to the practical reality that schema design, entity resolution, governance setup, and operational monitoring take longer than database installation alone. Neo4j's December 2025 launch of Fleet Manager reflected this need for easier lifecycle management across cloud, hybrid, and on-premises estates. Databricks also widened the service opportunity in April 2026 when it pushed Unity Catalog Business Semantics into general availability and joined the Open Semantic Interchange initiative, which will still require integration work inside customer environments. As a result, the agentic AI in the continue to seethe semantic layer and knowledge graph market is likely to continue to see services grow quickly as enterprises seek outside help to turn graph platforms into governed production systems.

Enterprise knowledge graphs accounted for 46.21% of the market value in 2025, making them the largest knowledge graph type. This position came from large organizations that needed to unify proprietary records, such as ERP data, customer profiles, product catalogs, and transaction histories, into a single, relationship-aware structure. In the agentic AI space, in the semantic layer and knowledge graph market, enterprise knowledge graphs are valuable because they support reasoning over internal assets that cannot be handled with open web data alone. Their lead also reflects the fact that large enterprises have stronger incentives to connect fragmented systems before they deploy autonomous agents widely.

Web-scale knowledge graphs are projected to grow at a 25.17% CAGR through 2031, which makes them the fastest-growing type. The growth path is tied to internet-facing use cases where entity resolution, deduplication, and relationship inference must operate across very large pools of public and semi-public information. Neo4j's Infinigraph launch in September 2025 showed how vendors are preparing for this scale by supporting 100TB+ deployments and billions of embedded vectors in a graph-native environment. Cloud platform support also matters here, because AWS and Microsoft continued to expand managed graph capabilities through 2025 and 2026, which lowers some of the infrastructure burden for very large graph workloads. That combination keeps enterprise graphs in the lead today, while web-scale graphs gain momentum as customer-facing search, recommendation, and reasoning workloads expand.

Geography Analysis

North America held 41.63% of the agentic AI market share in the semantic layer and knowledge graph market in 2025, maintaining its lead due to concentrated enterprise AI investment, a mature vendor base, and early adoption across BFSI and technology use cases. The United States led with investments in graph-grounded AI tools and managed graph platforms, while Canada contributed through financial services and healthcare adoption. Mexico remained in an earlier deployment phase. Key product launches, including Microsoft's Graph in Fabric, Databricks' expansion of its semantic layer, and Neo4j's platform releases in 2025 and 2026, further supported the market.

Europe, the second-largest region, saw demand growth in automotive, financial services, and public-sector AI governance programs. Germany, the United Kingdom, and France led due to stronger incentives for operational data linkage and explainability in regulated environments. The European Union AI Act heightened the importance of semantic layers and knowledge graphs for data governance and compliance.Italy and Spain contributed through financial services automation and public digital transformation, though on a smaller scale than leading Western European markets.

Asia-Pacific is projected to grow at a 25.52% CAGR from 2026 to 2031, driven by digital transformation programs and increased use of semantic reasoning in enterprise and public AI systems in China, India, South Korea, and Japan. AWS expanded regional access by extending Neptune Analytics to Mumbai in 2025 and additional locations in 2026, addressing infrastructure gaps for managed graph deployment. The Middle East is gaining prominence in AI, with the UAE and Saudi Arabia focusing on citizen data integration and public service AI initiatives. South America and Africa remain smaller markets, but Brazil, South Africa, and Egypt are building activity in financial services and telecommunications, despite talent and cost constraints. Service-led implementation models are likely to remain critical in these regions.

- Amazon.com, Inc. (AWS)

- Neo4j, Inc.

- Oracle Corporation

- Stardog Union, Inc.

- Ontotext AD

- TigerGraph, Inc.

- IBM Corporation

- Google LLC

- Microsoft Corporation

- SAP SE

- Databricks, Inc.

- DataStax, Inc.

- GraphAware Limited

- TerminusDB

- ArangoDB GmbH

- Franz Inc.

- PoolParty (Semantic Web Company GmbH)

- Expert.ai S.p.A.

- RelationalAI, Inc.

- Cambridge Semantics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Shift from Data Lakes to Semantic Data Fabrics

- 4.2.2 Rising Enterprise Adoption of Agentic AI For Autonomous Workflows

- 4.2.3 Regulatory Push for Explainable AI In Critical Industries

- 4.2.4 Mainstream Availability of Vector-Enabled Graph Databases

- 4.2.5 Surging Demand for Real-Time 360-View Customer Analytics In BFSI

- 4.2.6 Emergence of AI-Native Knowledge Agents in Developer Toolchains

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Large-Scale Knowledge Graph Projects

- 4.3.2 Shortage of Qualified Knowledge Graph Engineers and Ontologists

- 4.3.3 Data Sovereignty Concerns in Cross-Border Knowledge Integration

- 4.3.4 Interoperability Gaps Among Heterogeneous Graph Standards

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Knowledge-Graph Type

- 5.2.1 Enterprise Knowledge Graph

- 5.2.2 Domain-Specific Knowledge Graph

- 5.2.3 Web-Scale Knowledge Graph

- 5.3 By Application

- 5.3.1 Customer and 360-View Analytics

- 5.3.2 Fraud Detection and Risk Management

- 5.3.3 Recommendation and Personalization Engines

- 5.3.4 Conversational / Agentic AI Assistants

- 5.3.5 Knowledge Discovery and Research

- 5.4 By Deployment Mode

- 5.4.1 Cloud

- 5.4.2 On-Premises

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Retail and E-Commerce

- 5.5.4 Manufacturing and Supply-Chain

- 5.5.5 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon.com, Inc. (AWS)

- 6.4.2 Neo4j, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 Stardog Union, Inc.

- 6.4.5 Ontotext AD

- 6.4.6 TigerGraph, Inc.

- 6.4.7 IBM Corporation

- 6.4.8 Google LLC

- 6.4.9 Microsoft Corporation

- 6.4.10 SAP SE

- 6.4.11 Databricks, Inc.

- 6.4.12 DataStax, Inc.

- 6.4.13 GraphAware Limited

- 6.4.14 TerminusDB

- 6.4.15 ArangoDB GmbH

- 6.4.16 Franz Inc.

- 6.4.17 PoolParty (Semantic Web Company GmbH)

- 6.4.18 Expert.ai S.p.A.

- 6.4.19 RelationalAI, Inc.

- 6.4.20 Cambridge Semantics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment