PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061971

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061971

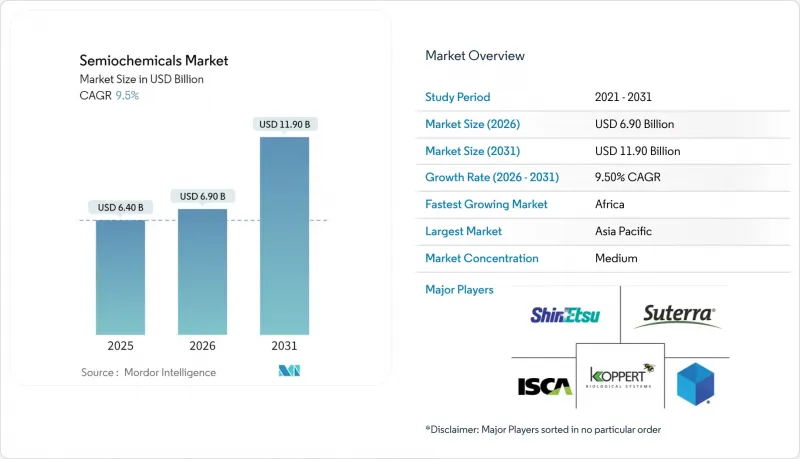

Semiochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the semiochemicals market was valued at USD 6.40 billion in 2025 and is projected to grow from USD 6.90 billion in 2026 to USD 11.90 billion by 2031, registering a CAGR of 9.50% during the forecast period 2026-2031.

This report is Segmented by Product Type (Pheromones, Kairomones, Allomones, and More), by Source (Plant-Derived, Synthetic, and More), by Application (Pest Monitoring, Mating Disruption, Mass Trapping, and More), by Livestock Species (Poultry, Swine, Aquaculture, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Semiochemicals Market Trends and Insights

Adoption of Pheromone-Based Mating-Disruption in High-Value Fruit Crops

Mating disruption has become a widely adopted semiochemical strategy in almond, pistachio, and walnut orchards due to its effectiveness in suppressing target pest populations without promoting resistance. Suterra's aerosol Puffer devices, deployed at a rate of one unit per acre, now cover over 400,000 acres in California. This method has reduced navel orangeworm damage by more than 50% when combined with monitoring traps . The technique minimizes the need for repeated insecticide applications, reduces residue levels that could jeopardize export certification, and helps preserve beneficial arthropods essential for integrated pest management programs. Additionally, growers report operational cost savings due to the once-per-season refill schedule and fewer sprayer passes. The adoption of this approach is expanding into grape and citrus orchards as generic insecticides become less effective and consumer demand for residue-free produce continues to grow.

Regulatory Bans on Broad-Spectrum Pesticides Favoring Bio-Rational Solutions

England's decision to phase out clothianidin, imidacloprid, and thiamethoxam by December 2024 highlights a global trend toward stricter pesticide regulations . In the European Union, straight-chain lepidopteran pheromones benefit from a streamlined approval process, reducing dossier costs and fostering portfolio expansion. This regulatory advantage accelerates commercialization for established players with existing data packages, while new kairomones are required to undergo full toxicology assessments. This disparity increases the attractiveness of semiochemicals for growers aiming to meet regulatory requirements without compromising yields, driving the semiochemicals market toward double-digit growth rates.

High Formulation and Micro-Encapsulation Costs

Manufacturers incur an added cost of USD 50-150 per kilogram when using polymer coatings or mesoporous silica in controlled-release systems. While almond and wine grape growers benefit from savings due to reduced re-sprays, those cultivating maize or rice, operating on tighter margins, are more cautious. There's promise in industrial-scale fermentation, yet the pursuit of enantiomeric purity and stable yields demands significant capital. As reported by Unife, public-private initiatives in the European Union are backing process-optimization trials to cut costs by 50% in just two seasons. However, until such advancements materialize, the pricing remains a barrier for widespread adoption in staple broadacre crops.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Organic Acreage in Asia-Pacific

- Feed Conversion-Efficiency Gains in Poultry Through Kairomone Blends

- Limited Field-Efficacy Data Under Tropical Humidity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pheromones accounted for the largest share of the semiochemicals market, representing 44% in 2025. Meanwhile, blends are anticipated to be the fastest-growing segment, with a projected CAGR of 15.8% from 2026 to 2031. This growth reflects a shift among growers toward multi-molecule solutions to address rising resistance and overlapping pest cycles. Field studies suggest that blends combining sex pheromones with host-plant kairomones can reduce infestation by up to 70% across multiple target species per hectare. Furthermore, research pipelines tracking over 60 candidate blends, including allomones for repellency and synomones for natural enemy attraction, underscore ongoing innovation in the market.

The market's growth is driven by increasing consumer intolerance for pesticide residues and heightened audit requirements from produce retailers. Manufacturers are utilizing artificial intelligence-guided formulation techniques to synchronize the release curves of each component, ensuring balanced ratios throughout the growing season. Licensing agreements enable specialty-crop growers to refill dispensers with custom canisters tailored to their specific pest complexes, fostering recurring revenue streams. Additionally, the semiochemicals market is gaining resilience as blends replace insect growth regulators that are being phased out due to regulatory changes, reducing the likelihood of single-mode resistance outbreaks.

Synthetic pheromones held the largest market share in the semiochemicals market at 38% in 2025, while plant-derived volatiles are projected to be the fastest-growing segment at a CAGR of 14.6% from 2026 to 2031, driven by increasing demand for organic certification and consumer trust. Steam-distilled essential oils such as thymol, eugenol, and geraniol offer dual functionality as repellents and microbial inhibitors, enabling hybrid formulations that combine behavioral and bioactive control.

Supply chains face challenges due to the low essential oil yields of 0.3-2.0% from fresh biomass, prompting companies to secure dedicated acreage for production. Advances in metabolic engineering of rosemary and basil are targeting a three-fold increase in volatile compound output, while green extraction technologies aim to minimize solvent waste. Synthetic biology companies are utilizing yeast fermentation of terpene pathways to address seasonal supply gaps. Integrated solutions combining synthetic backbone pheromones with plant-derived boosters leverage the advantages of both approaches, addressing regulatory, cost, and efficacy requirements within a single formulation.

Geography Analysis

Asia-Pacific held the largest market share of the semiochemicals market at 33% in 2025. This dominance is supported by the combined organic acreage of China and India. Government initiatives, including funding for demonstration farms that utilize pheromone traps and micro-sprinkler mating-disruption systems, have played a crucial role in improving agricultural practices. These measures have significantly reduced vegetable rejection rates by addressing pest-related challenges, thereby enhancing grower confidence and encouraging the adoption of semiochemicals across the region.

Africa is projected to be the fastest-growing region in the semiochemicals market, with a CAGR of 14.9% from 2026 to 2031. Growth is fueled by donor-supported integrated pest management programs that focus on residue-free export crops such as mangoes, avocados, and cut flowers. Advances in climate-resilient formulations, which now endure high humidity in East Africa, have extended lure life from three to six months. Additionally, policy harmonization under the African Continental Free Trade Area is reducing registration barriers, facilitating regional approvals, and supporting broader market expansion.

In North America, the semiochemicals market shows a high installed base in tree nuts and pome fruit orchards. However, growth is plateauing as market penetration nears saturation. Expansion persists in maize-growing regions, where Provivi, Inc.'s cost-effective pheromone sachets effectively reduce fall armyworm pressure without triggering secondary pest outbreaks. In South America, market uptake is accelerating with the establishment of cold-chain hubs near Mato Grosso grain corridors. These hubs address product-integrity challenges that previously hindered demand, enabling stronger market growth.

- Suterra LLC

- Shin-Etsu Chemical Co., Ltd.

- Koppert Biological Systems B.V.

- ISCA Technologies, Inc.

- Russell IPM Ltd

- Provivi, Inc.

- Bedoukian Research, Inc.

- Trece, Inc.

- Biobest Group NV

- BASF SE

- Mitsui Chemicals Agro, Inc.

- Sumitomo Chemical Co., Ltd.

- FMC Corporation

- SemiosBio Technologies Inc.

- Exosect Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of pheromone-based mating-disruption in high-value fruit crops

- 4.2.2 Regulatory bans on broad-spectrum pesticides favoring bio-rational solutions

- 4.2.3 Rapid expansion of organic acreage in Asia-Pacific

- 4.2.4 Feed conversion-efficiency gains in poultry through kairomone blends

- 4.2.5 Precision-ag platforms integrating semiochemical dispensers

- 4.2.6 Emergence of climate-resilient semiochemical formulations

- 4.3 Market Restraints

- 4.3.1 High formulation and micro-encapsulation costs

- 4.3.2 Limited field-efficacy data under tropical humidity

- 4.3.3 Fragmented distribution in South America smallholder channels

- 4.3.4 Regulatory uncertainty over synthetic-analog approvals in Europe

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Pheromones

- 5.1.2 Kairomones

- 5.1.3 Allomones

- 5.1.4 Synomones

- 5.1.5 Semiochemical Blends

- 5.2 By Source

- 5.2.1 Plant-derived

- 5.2.2 Insect-derived

- 5.2.3 Synthetic

- 5.3 By Application

- 5.3.1 Pest Monitoring

- 5.3.2 Mating Disruption

- 5.3.3 Mass Trapping

- 5.3.4 Livestock Feed-Intake Modulation

- 5.3.5 Stress Reduction and Welfare

- 5.4 By Livestock Species

- 5.4.1 Poultry

- 5.4.2 Swine

- 5.4.3 Ruminants (Cattle, Sheep, Goat)

- 5.4.4 Aquaculture

- 5.4.5 Other Livestock Species

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Turkey

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Suterra LLC

- 6.4.2 Shin-Etsu Chemical Co., Ltd.

- 6.4.3 Koppert Biological Systems B.V.

- 6.4.4 ISCA Technologies, Inc.

- 6.4.5 Russell IPM Ltd

- 6.4.6 Provivi, Inc.

- 6.4.7 Bedoukian Research, Inc.

- 6.4.8 Trece, Inc.

- 6.4.9 Biobest Group NV

- 6.4.10 BASF SE

- 6.4.11 Mitsui Chemicals Agro, Inc.

- 6.4.12 Sumitomo Chemical Co., Ltd.

- 6.4.13 FMC Corporation

- 6.4.14 SemiosBio Technologies Inc.

- 6.4.15 Exosect Ltd.

7 Market Opportunities and Future Outlook