PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061986

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061986

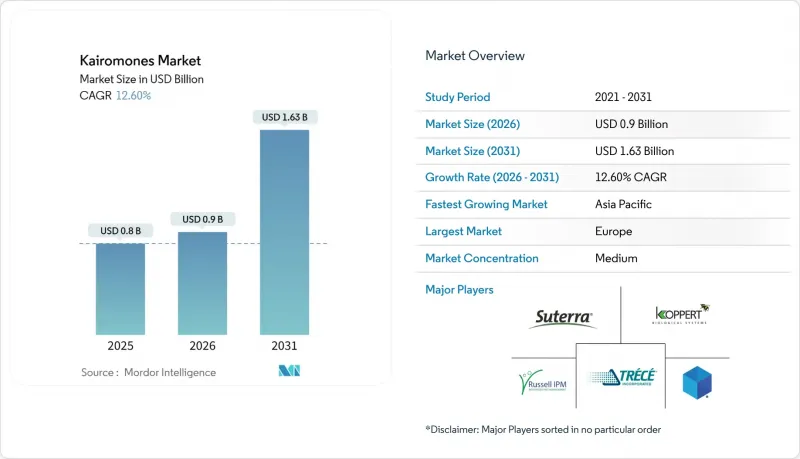

Kairomones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the kairomones market size is projected to grow from USD 0.80 billion in 2025 to USD 0.90 billion in 2026, reaching USD 1.63 billion by 2031, with a CAGR of 12.6% during the 2026-2031 period.

This report is Segmented by Function (Mass Trapping, Detection and Monitoring, Mating Disruption, and Other Functions), by Crop Type (Field Crops, Horticulture Crops, Plantation Crops, Floriculture, and Other Crop Types), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Kairomones Market Trends and Insights

Regulatory Push to Replace Broad-Spectrum Insecticides

Governments are increasingly implementing stricter residue limits, prompting growers to adopt low-risk alternatives. This shift is encouraging the use of kairomone lures within integrated pest management (IPM) frameworks. The Sustainable Use Regulation (SUR), proposed by the European Union in 2022, seeks to enhance the adoption of integrated pest management (IPM) by encouraging the use of non-chemical alternatives and reducing the risk by 50% by 2030. In Canada, Health Canada's pesticide re-evaluation programs continue to review semiochemical substances, demonstrating ongoing regulatory oversight. These regulatory developments promote reduced insecticide usage and assist growers in meeting certification standards such as GlobalG.A.P. and Rainforest Alliance.

Falling Unit-Cost of Bio-Fermented Semiochemicals

Declining unit costs of bio-fermented semiochemicals are driving increased adoption of kairomone-based solutions in crop protection. Improvements in metabolic engineering and fermentation processes have enhanced production efficiency, enabling scalable and cost-effective manufacturing of complex volatile compounds. For instance, a study published in Bioengineering and Biotechnology in 2021 indicates that engineered Yarrowia lipolytica serves as an effective microbial platform for producing insect pheromones and related semiochemicals. Advances in metabolic engineering have notably enhanced production efficiency compared to previous microbial systems.

High Multi-Jurisdictional Registration Fees

The preparation of identity, purity, efficacy, and environmental fate dossiers incurs high costs per active substance in the European Union, with approval processes taking several years. Comparable regulatory challenges in Japan and Australia provide a competitive edge to well-funded companies like Suterra LLC, while smaller innovators often opt to license formulations instead of pursuing independent registrations. According to the Organisation for Economic Co-operation and Development Biopesticide Steering Group, efforts are being made to establish mutual recognition frameworks, though progress remains slow.

Other drivers and restraints analyzed in the detailed report include:

- Precision-Ag Adoption of Smart Kairomone Lures

- Climate-Smart Repellent Portfolios for Heat-Stressed Regions

- Field Instability in Hot and Humid Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The detection and monitoring segment remains the largest in the kairomones market, accounting for 41% of the market share in 2025. However, this segment is maturing in regions such as Europe and North America, where lure-based scouting methods are already widely adopted. The mating disruption market size is projected to grow at the fastest rate, with a CAGR of 18% from 2026 to 2031, surpassing the overall market growth rate of 12.6%. This growth is driven by declining production costs and increasing adoption in large-scale crop protection strategies. Meanwhile, mass trapping continues to gain steady traction in regions like Kenya and Brazil, supported by advancements in formulation technologies that improve field performance under challenging environmental conditions.

In 2022, Suterra LLC, a global provider of sustainable pheromone pest control solutions, announced that four of its established products are now listed with the Organic Materials Review Institute (OMRI) for use in organic agricultural production. Further, Russell IPM Ltd's artificial intelligence (AI)-enabled trapping systems in Kenya's floriculture sector, facilitating data-driven pest control decisions in alignment with mating disruption programs. These developments reflect a broader industry trend observed in recent years, transitioning from detection-focused solutions to disruption strategies. This shift is influenced by the integration of digital agriculture tools.

Geography Analysis

Europe remained the largest regional segment in the kairomones market, holding a 29% market share in 2025. This dominance is attributed to robust regulatory frameworks and the widespread adoption of integrated pest management practices in countries such as France, Germany, and the Netherlands. The region benefits from policy-driven transitions toward sustainable agriculture, increased local production of bio-based semiochemicals, and active participation in regional innovation programs. Additionally, Eastern European markets are gradually adopting kairomone-based solutions, supported by sustainability-focused agricultural initiatives.

The Asia-Pacific market size is projected to grow at the fastest rate, with a projected CAGR of 15.8% from 2026 to 2031. Growth in this region is driven by increasing biopesticide adoption, favorable government policies, and rising domestic production capabilities in countries like China and India. The integration of digital agriculture tools with semiochemical applications, particularly in high-value crop systems, is also gaining traction. However, infrastructure and adoption challenges in rural areas create a varied pace of market expansion across the region.

North America continues to play a pivotal role as a regulatory and innovation hub for the kairomones market. Evolving policies are encouraging broader adoption of semiochemical-based solutions among growers. South America is enhancing its market presence through cooperative-led distribution models and the increasing use of sustainable pest management practices in commercial agriculture. The Middle East and Africa are witnessing a gradual uptake of kairomone-based solutions, particularly in plantation and export-oriented crops. This growth is supported by advancements in monitoring technologies and a growing awareness of residue-free agricultural practices.

- Suterra LLC

- Russell IPM Ltd

- Synergy Semiochemicals Corp.

- Koppert Biological Systems B.V.

- Trece, Inc.

- Bioglobal Holdings Limited

- Chemtica Internacional, S.A.

- Rincon-Vitova Insectaries, Inc.

- Harmony Ecotech Private Limited

- SANIDAD AGRICOLA ECONEX, S.L.

- SOSPALM

- Colkim S.r.l.

- Novagrica Hellas S.A.

- Provivi, Inc.

- ISCA Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push to replace broad-spectrum insecticides

- 4.2.2 Falling unit-cost of bio-fermented semiochemicals

- 4.2.3 Precision-ag adoption of smart kairomone lures

- 4.2.4 Climate-smart repellent portfolios for heat-stressed regions

- 4.2.5 Clustered Regularly Interspaced Short Palindromic (CRISPR)-engineered microbial chassis for volatile synthesis

- 4.2.6 Digital-twin modeling that optimizes kairomone release

- 4.3 Market Restraints

- 4.3.1 High multi-jurisdictional registration fees

- 4.3.2 Field instability in hot and humid climates

- 4.3.3 Patchy last-mile distribution in developing agri-economies

- 4.3.4 Brand cannibalization from low-priced synthetic pheromones

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Mass Trapping

- 5.1.2 Detection and Monitoring

- 5.1.3 Mating Disruption

- 5.1.4 Other Functions

- 5.2 By Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticulture Crops

- 5.2.3 Plantation Crops

- 5.2.4 Floriculture

- 5.2.5 Other Crop Types

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Russia

- 5.3.3.4 United Kingdom

- 5.3.3.5 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Kenya

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Suterra LLC

- 6.4.2 Russell IPM Ltd

- 6.4.3 Synergy Semiochemicals Corp.

- 6.4.4 Koppert Biological Systems B.V.

- 6.4.5 Trece, Inc.

- 6.4.6 Bioglobal Holdings Limited

- 6.4.7 Chemtica Internacional, S.A.

- 6.4.8 Rincon-Vitova Insectaries, Inc.

- 6.4.9 Harmony Ecotech Private Limited

- 6.4.10 SANIDAD AGRICOLA ECONEX, S.L.

- 6.4.11 SOSPALM

- 6.4.12 Colkim S.r.l.

- 6.4.13 Novagrica Hellas S.A.

- 6.4.14 Provivi, Inc.

- 6.4.15 ISCA Technologies, Inc.

7 Market Opportunities and Future Outlook